Physicswallah is one of India’s fastest-growing edtech companies, known for its hybrid model that combines digital content with physical learning centers. Founded by Alakh Pandey, the company has rapidly scaled its operations, serving millions of students across competitive exam categories such as JEE, NEET, and UPSC.

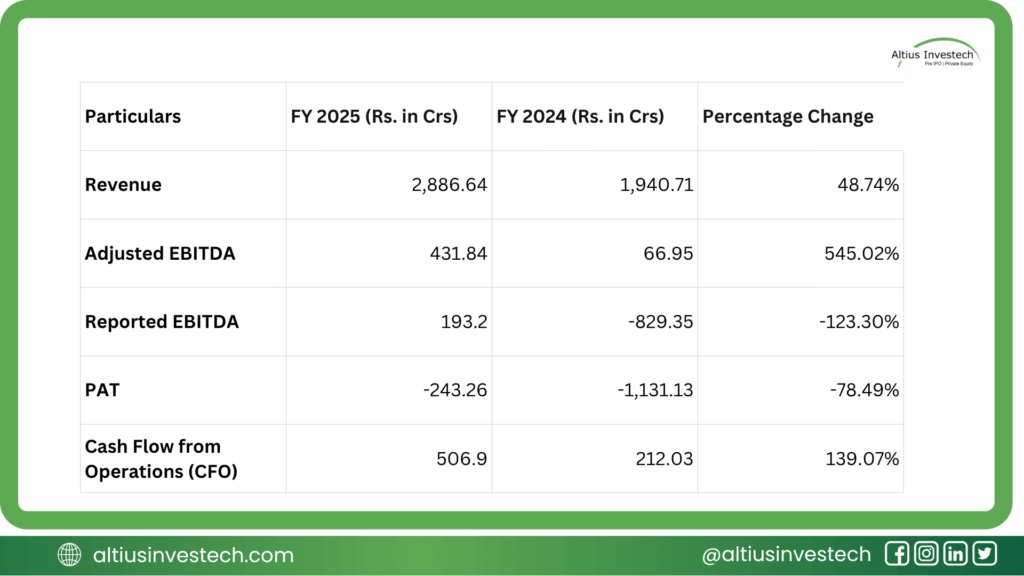

It reported a revenue of ₹2,886.64 crore in FY25, making it one of the largest players in the sector by topline.

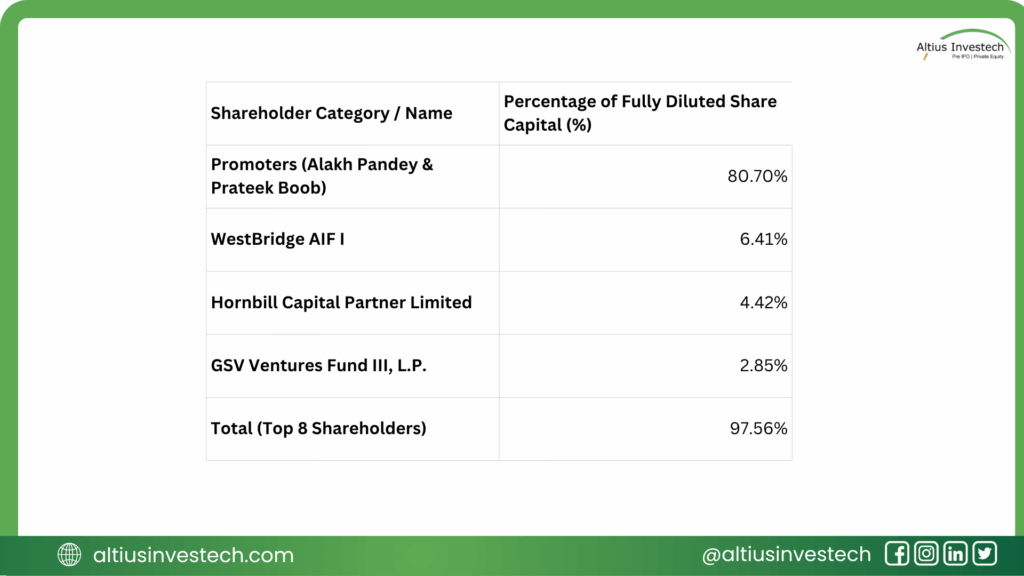

Backed by marquee investors like WestBridge and GSV Ventures, Physicswallah is now preparing for its public market debut through an IPO.

The offering marks a key milestone in the company’s journey from YouTube channel to unicorn, and invites close scrutiny of its financial strength, governance standards, and valuation.

Ownership Structure:

Core Assets & Operational Foundation: The Engine of Scale ⚙️

Physicswallah’s operational engine is built on three pillars designed for massive scale:

- Content Library: An extensive digital repository, including a question bank with over 8.20 million items, forms the backbone of its educational offerings.

- Faculty & Delivery: A large and growing team of 5,096 faculty members as of March 31, 2025, delivers this content through a proprietary Learning Management System (LMS) and a rapidly expanding physical network.

- Omni-channel Infrastructure: The company operates 198 total offline centers (PW Vidyapeeth and PW Pathshala), creating a hybrid ecosystem that blends the reach of online with the effectiveness of offline learning.

Strategic Value Proposition: The Affordability Moat 🏰

Physicswallah’s primary competitive advantage—its “moat”—is its disruptive pricing strategy. This is not just a marketing tactic; it’s the core of its value proposition.

Market Capture Strategy: The aggressive expansion of its omni-channel network is a direct play to consolidate the fragmented test preparation market. By offering an affordable and accessible alternative, PW is positioned to capture market share from both premium legacy players and smaller, unorganized coaching centers.

Price Disruption: PW’s one-year online JEE course is priced at ₹ 4,500 (₹ 0.045 lakh). This is a fraction of the industry average of ₹ 7.5 lakh-₹ 8.0 lakh charged by the top five organized competitors. This creates an enormous value proposition for students in Tier 2 cities and beyond, effectively democratizing access to quality test prep.

Financial Analysis

Financial Insights:

Fortified Balance Sheet: The IPO follows a crucial balance sheet cleanup. The conversion of CCPS to equity has eliminated a major liability, resulting in a positive Net Worth of ₹ 1,945.37 crore and making the company virtually debt-free. This presents a much cleaner and more resilient entity to public markets.

Look Beyond Reported Profit: The FY24 loss was an anomaly, driven by a ₹ 756.47 crore non-cash charge for preference shares. The Adjusted EBITDA of ₹ 431.84 crore in FY25 (a 14.96% margin) is a far better indicator of the core business’s profitability.

Negative Working Capital Model: The company’s ability to generate ₹ 506.90 crore in CFO despite a net loss is the highlight. This is achieved by collecting fees in advance, reflected in the ₹ 863.66 crore of Contract Liabilities on its balance sheet. This model provides substantial, interest-free capital to fund growth.

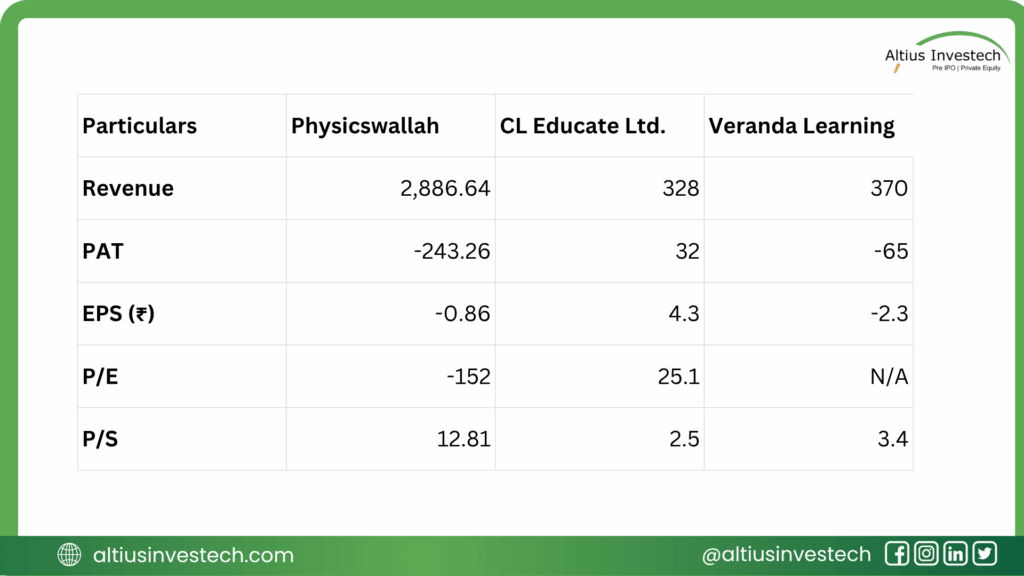

Peer Analysis (FY 2024-25)

Scale Dominance: Physicswallah’s revenue is nearly 8x larger than its listed peers, justifying its position as a market leader.

Valuation Premium: Investors will be asked to pay a significant premium for this scale and hyper-growth. An illustrative Price-to-Sales (P/S) ratio of ∼12.81x is substantially higher than peers, indicating that the market must believe in its future growth trajectory to justify the price.

Profitability vs. Growth: While peers like CL Educate are profitable (P/E of 25.1x), Physicswallah’s investment case is not about current earnings. The P/E ratio is not a meaningful metric due to its statutory loss. The entire bet is on future market share capture translating into future profits.

Conclusion: Refining the Investment View

Financially Robust Core: The company is not a typical loss-making startup. Its core operations are highly cash-generative, and its balance sheet is now fortified for public markets. The statutory loss is primarily an accounting narrative of its aggressive acquisition strategy.

Governance Discount is Warranted: The repeated red flags on internal financial controls from auditors are a serious concern. Investors must apply a “governance discount” to their valuation until the company demonstrates a mature and robust compliance framework.

Valuation Hinges on Growth Narrative: The IPO’s success will depend on convincing investors to look past the current losses and governance issues and pay a premium valuation for a dominant position in a structurally growing market. The high promoter ownership provides alignment, but the OFS component needs to be watched.

Final Verdict: The Physicswallah IPO is an opportunity to invest in a market-defining, high-growth educational platform. However, it’s a high-risk, high-reward proposition. The investment is suitable for investors with a strong risk appetite who are making a long-term bet on management’s ability to execute its ambitious expansion plan and, crucially, elevate its corporate governance to the standards expected of a public company.

Looking to invest in more high-potential companies like Physicswallah ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius