Versuni, the new name behind the iconic Philips and Preethi home appliances, just dropped its annual report for FY2025. On the surface, it tells a story of steady growth. But beneath the numbers lies a bold, high-stakes strategy. The company is betting big on the upcoming festive season, deliberately stocking its warehouses to the brim. Is this a masterstroke of foresight or a risky gamble that could backfire? Let’s unplug the appliance and look at the wiring inside.

Growth with a Catch: Versuni’s revenue grew a healthy 7.8%, driven by strong performance in its Airfryer and Mixer Grinder categories.

A Big Festive Bet: Inventories surged 59%, a deliberate move management confirmed at the AGM is to stock up for a massive upcoming festive season, anticipating a surge in consumer demand.

Profit Margins Under Pressure: Despite selling more, the company’s profitability shrank. Higher costs for materials and operations ate into the profits, causing margins to decline.

Cash Has Left the Building: The company’s cash and cash equivalents dropped by a staggering 43%, largely due to a significant dividend payment to its Dutch parent company.

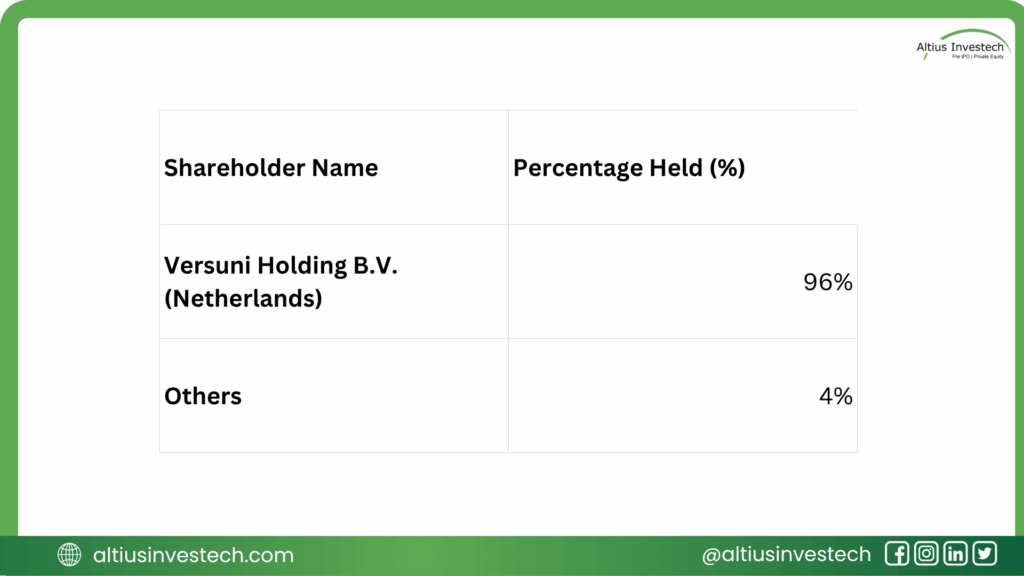

Ownership Structure:

🚀 The Versuni Engine: A Legacy Rebranded

At its heart, Versuni is a powerhouse in the Indian consumer durables market. It leverages the global innovation of the Philips brand and the deep-rooted market dominance of Preethi, especially in the South Indian mixer grinder segment. Its business model is built on turning houses into homes through a steady stream of innovative and sustainable appliances, from the kitchen to the living room.

🛡️ What is Versuni’s Competitive Moat?

Versuni’s market position is defended by several key strengths that make it a formidable player.

Distribution Dominance: Versuni boasts an unparalleled distribution network across India, ensuring its products are available from large retail chains in metros to small family-owned shops in Tier-3 towns.

Brand Royalty: The Philips name is synonymous with quality and trust globally. In India, the Preethi brand is a household name with an iron grip on the kitchen appliances market, giving Versuni incredible pricing power and brand recall.

Innovation Pipeline: From pioneering the Airfryer to launching new, eco-friendly mixer grinders, the company consistently invests in R&D to stay ahead of consumer trends and create new market categories.

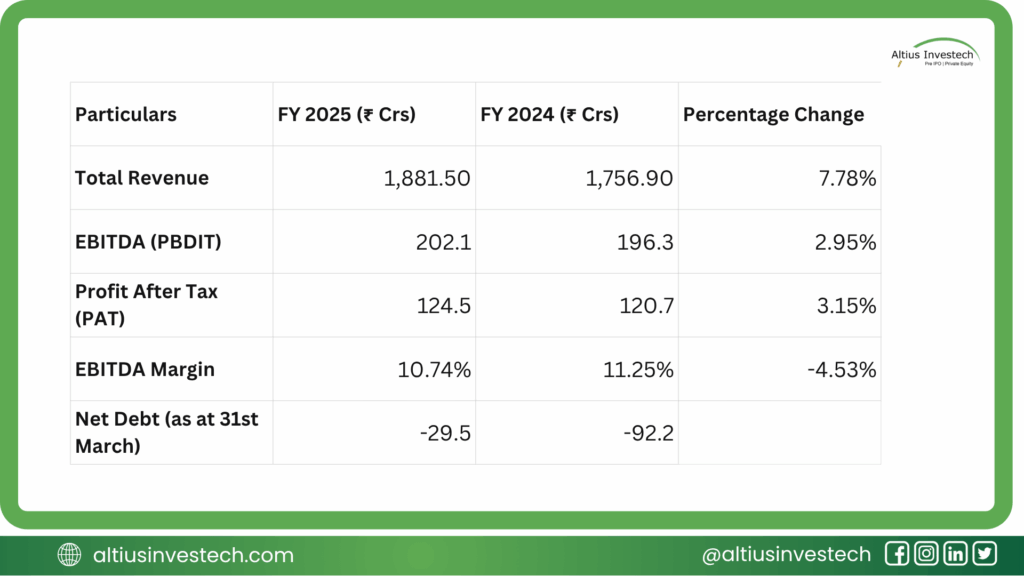

Financial Analysis

The FY25 numbers tell a fascinating story. While the company successfully grew its top line, the bottom line didn’t keep pace. The pressure on profitability is evident.

Financial Insights:

While absolute EBITDA and PAT saw modest growth, the EBITDA margin contracted. This happened because total expenses grew faster (8.4%) than revenue (7.8%). The main culprits were a sharp 23% increase in the cost of goods purchased and an 18% jump in other operational expenses.

⚠️ Red Flags: The Warning Lights and The Big Bet

Beneath the surface of the financial statements, several points demand attention.

- The High-Stakes Inventory Bet: A 59% surge in inventory is a massive gamble. As explained by management, this is a deliberate and strategic buildup for the upcoming festive season to meet anticipated high demand. While proactive, this ties up significant cash and creates a huge risk. If the expected festive sales don’t materialize, the company could be left with a mountain of unsold stock and face heavy discounting to clear it.

- The Great Cash Exodus: A 43% drop in cash reserves in a single year is alarming. While the company generated positive free cash flow, a massive dividend payout of ₹88 Crores to its parent company, Versuni Holding B.V., drained the domestic entity’s liquidity.

- The Profitability Squeeze: The declining margins show that Versuni is struggling with cost control or facing intense pricing pressure, a trend that needs reversing.

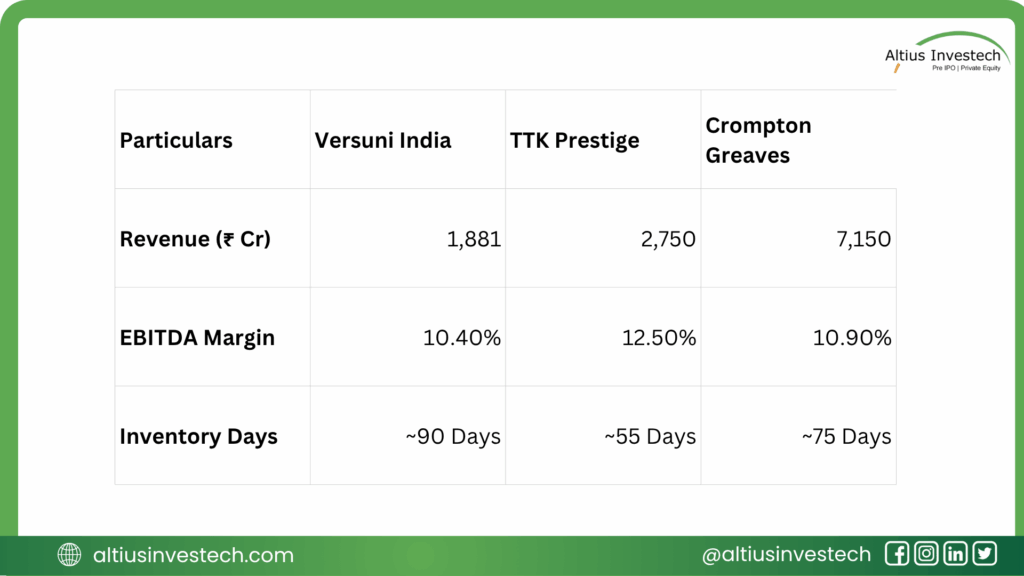

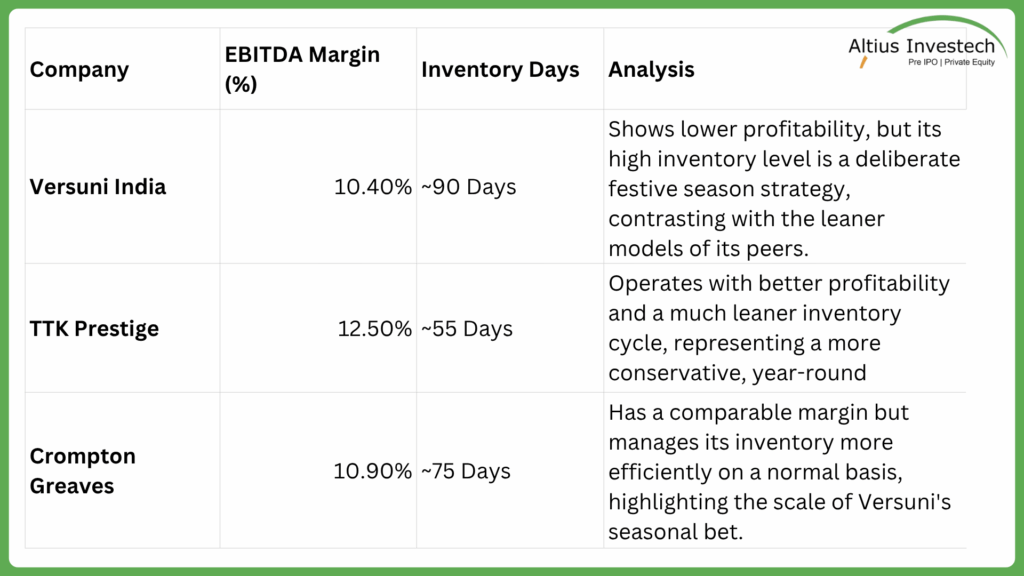

Peer Analysis (FY 2024-25)

This comparison puts Versuni’s recent performance into sharp focus and highlights two critical areas of concern.

- The Profitability Gap: Versuni’s EBITDA margin of 10.4% lags behind its direct competitor, TTK Prestige (12.5%), and is slightly below the larger, more diversified Crompton Greaves. This confirms the “margin squeeze” seen in its financials; its peers are simply more effective at converting sales into operating profit.

- The Efficiency Problem (Inventory Overload): This is the most glaring issue. Versuni takes approximately 90 days to sell its inventory, which is significantly higher than the much leaner TTK Prestige at 55 days and even the larger Crompton at 75 days. This points to a major inefficiency in its working capital management, tying up a huge amount of cash in warehouses and increasing the risk of stock obsolescence.

In essence, while Versuni holds its own on the sales front with its powerful brands, its listed peers are running a tighter ship, demonstrating superior profitability and far more efficient control over their inventory.

Conclusion: Refining the Investment View

Strong Brand Core: Versuni is not a business struggling for relevance. Its foundation is built on iconic, market-leading brands (Philips and Preethi) that command consumer trust and drive consistent top-line growth. This brand equity provides a significant competitive moat and pricing power.

Working Capital and Governance Risks are Material: The massive inventory buildup, even if strategic, combined with the sharp drop in cash reserves, highlights a significant working capital risk. If the anticipated festive demand falters, the financial strain could be substantial. Furthermore, the high volume of related-party transactions, while disclosed, warrants a “governance premium” in risk assessment until the company demonstrates that domestic liquidity and profitability are prioritized.

Valuation Hinges on Operational Execution: The company’s future value depends entirely on its ability to convert its strong market position into efficient, profitable growth. Investors need to be convinced that management can navigate its high-stakes inventory strategy successfully, reverse the trend of margin compression, and manage its cash with a focus on strengthening the Indian entity’s balance sheet.

Concluding Analysis: Versuni India represents an investment in a powerful consumer brand franchise. However, it’s a “show me” story fraught with operational challenges. The investment is suitable for investors who believe in the long-term structural growth of the Indian consumer durables market and are confident in management’s ability to execute its ambitious sales strategy without compromising financial stability. The key risk is not the brand, but the execution.

Looking to invest in more high-potential companies likeVersuni ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)