Billionbrains Garage Ventures, the parent company of India’s largest stockbroker Groww, is heading for an IPO. The numbers are staggering: market leadership in active clients, explosive revenue growth, and a dramatic swing back to profitability. But a deep dive into its draft prospectus reveals a fascinating paradox. This is a story of a high-octane growth engine that, despite reporting massive profits, is burning through cash at an alarming rate. For investors, the key question is: Is this a visionary investment in future dominance or a high-risk gamble on a cash-hungry business model?

Market Dominance & Explosive Growth: Groww is the undisputed leader in NSE active clients. Its revenue surged nearly 50% in FY25 to ₹3,902 Crores.

The Profitability Illusion: The company swung from a massive loss in FY24 to a record profit of ₹1,824 Crores in FY25. However, this was mainly because FY24 was hit by a huge one-time tax charge and a massive management bonus.

The Cash Burn Problem: This is the central risk. Despite record profits, Groww had a negative operating cash flow of over ₹962 Crores in FY25. The profit is on paper; the cash is being aggressively reinvested into its new lending businesses.

Emerging Risks: The rapid expansion into lending is showing early signs of stress, with Non-Performing Assets (NPAs) rising sharply. The business is also highly vulnerable to regulatory changes.

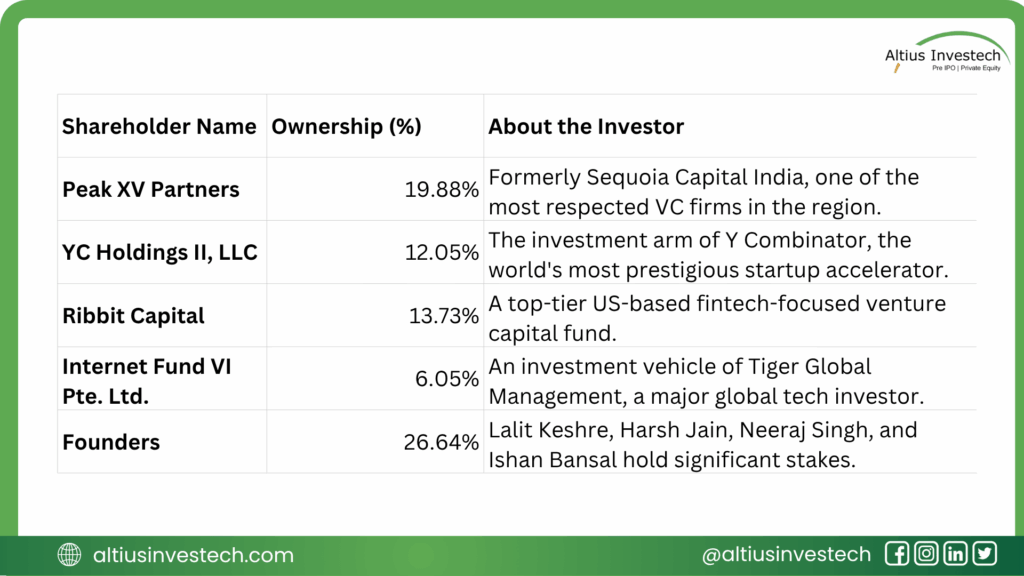

Ownership Structure:

Groww is backed by a who’s who of global venture capital, a strong vote of confidence from some of the smartest money in the world.

🚀 What’s Driving the Groww Engine?

At its core, Groww is a digital-first, direct-to-customer investment platform. Its simple, user-friendly app has been instrumental in bringing millions of new retail investors to the market. The business model is straightforward:

Lending & Interest Income: Earns interest from its rapidly growing Margin Trading Facility (MTF) and consumer credit (NBFC) businesses.

Brokerage: Earns fees and commissions from the millions of trades executed on its platform.

🛡️ What is Groww’s Competitive Moat?

Groww’s meteoric rise isn’t a fluke. It’s built on a powerful and defensible competitive advantage.

In-House Technology Stack: The company owns and operates its entire technology infrastructure. This allows for rapid innovation, better security, and superior operating leverage as it scales. The proof is in the numbers: its Adjusted Cost to Operate has fallen from 26% of revenue in FY23 to just under 14% in FY25.

Viral Organic Growth: Unlike peers who spend heavily on advertising, over 80% of Groww’s customers are acquired organically. This word-of-mouth growth model creates a massive cost advantage and a loyal user base.

Financial Analysis

Financial Insights:

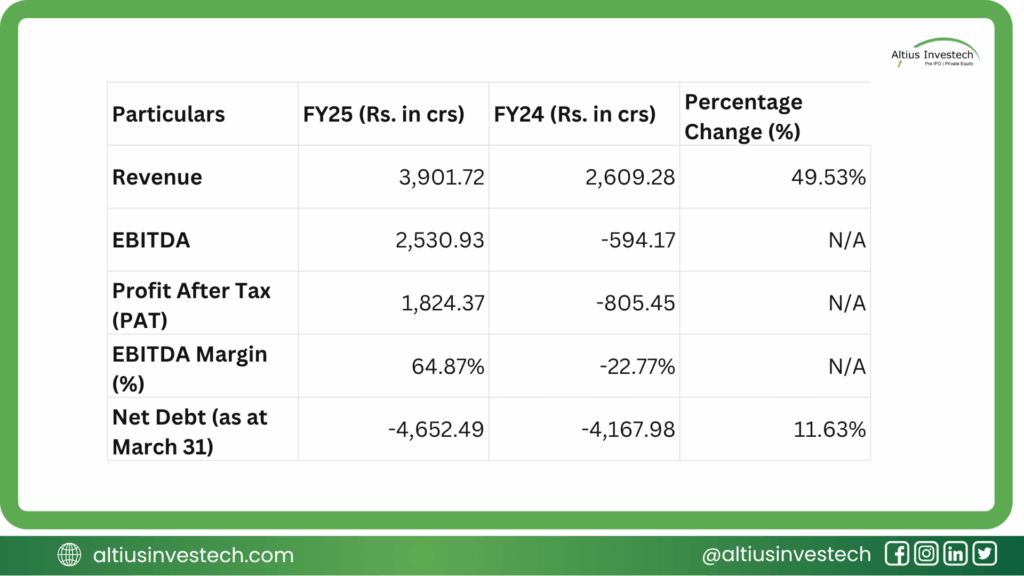

The enormous loss in FY24 wasn’t due to poor operational performance. It was caused by two extraordinary, non-recurring events: a one-time tax liability of ~₹1,340 Crores related to a US merger and a one-time management performance incentive of ~₹779 Crores.

The return to a staggering 65% EBITDA margin in FY25 shows the true, underlying profitability of the core business. However, this is where the paradox begins. Despite these impressive profits, the company’s operating cash flow was negative ₹962 Crores. This cash is being used to fund the loan books of its NBFC and MTF businesses, making the company’s growth extremely capital-intensive.

⚠️ Red Flags: The Risks Under the Hood

Beyond the cash flow paradox, investors need to be aware of several material risks.

- Deteriorating Loan Quality: The push into lending is showing signs of stress. The Gross NPA percentage on its NBFC loan book has jumped from a healthy 0.29% to 1.68% in just one year, a significant deterioration in asset quality.

- The Regulatory Tightrope: Groww’s revenue is highly sensitive to regulatory changes. Recent SEBI circulars in late 2024 immediately led to a drop in broking fees and trading volumes, demonstrating how quickly the regulatory environment can impact the bottom line.

- The Governance Question: The payment of a massive, one-time bonus to management in FY24, which significantly impacted the year’s financials, raises questions about corporate governance practices that will be under scrutiny in the public markets.

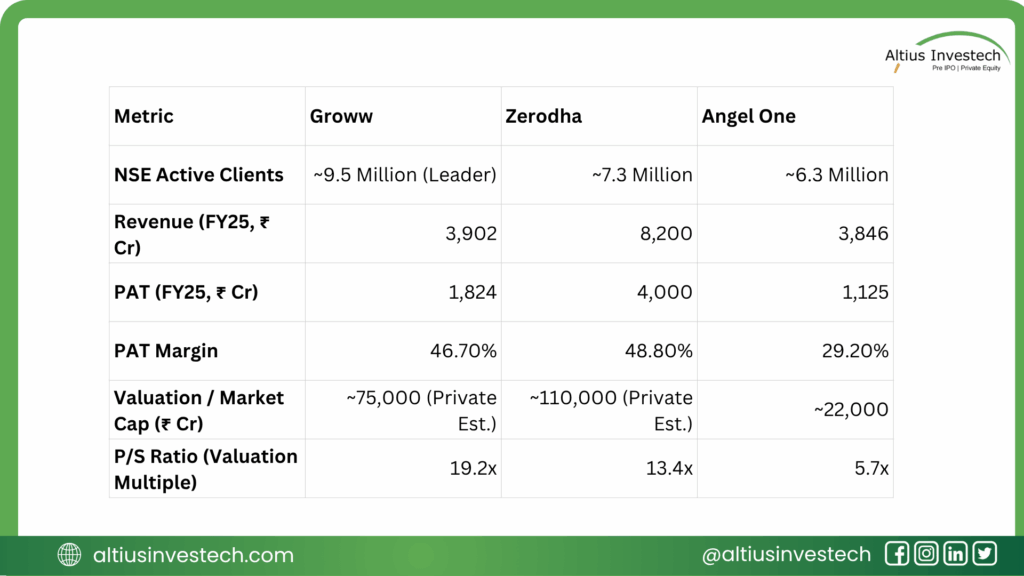

Peers Analysis(FY 2025)

This comparison reveals three distinct strategies in the Indian brokerage market.

- The Scale King (Groww): Groww’s primary focus has been on user acquisition, and it has succeeded spectacularly, becoming the undisputed leader in active clients. Its viral, organic growth model is its biggest asset.

- The Profitability Champion (Zerodha): Zerodha is in a league of its own when it comes to capital efficiency. As a bootstrapped company, it generates nearly ₹48 of profit for every ₹100 of revenue without any external funding, a testament to its lean operational model.

- The Valuation Story (Groww vs. Angel One): This is the most crucial insight for IPO investors. The market is willing to pay a Price-to-Sales (P/S) multiple of 19.2x for Groww, more than three times the multiple for its publicly listed peer, Angel One (5.7x). This massive premium indicates that investors are betting heavily on Groww’s superior market share and faster growth rate, believing it will eventually convert its millions of users into industry-leading profits, and are therefore willing to pay a premium for that future potential today.

Conclusion: Refining the Investment View

Financially Robust Core: This is not a typical loss-making startup. Excluding one-off charges, Groww’s core brokerage business is a highly profitable, cash-generative machine with powerful operating leverage. The statutory loss in FY24 is an accounting narrative, not an operational one.

A “Governance Discount” is Warranted: The massive, one-time management bonus and other related-party transactions are a concern. Investors must apply a “governance discount” to their valuation until the company demonstrates a mature and robust compliance framework expected of a public entity.

Valuation Hinges on the Growth Narrative: The IPO’s success will depend on convincing investors to look past the current cash burn and governance questions and pay a premium for a dominant position in a structurally growing market.

Concluding Perspective: The Groww IPO is an opportunity to invest in a market-defining, high-growth educational platform. However, it’s a high-risk, high-reward proposition. The investment is suitable for investors with a strong risk appetite who are making a long-term bet on management’s ability to successfully scale its lending business and, crucially, elevate its corporate governance to public market standards.

Looking to invest in more high-potential companies like Groww ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)