The Indian IPO market is heating up again — and this time, the spotlight is on Lenskart, India’s eyewear unicorn turned global retail disruptor. From humble beginnings as an online spectacle seller to becoming a full-fledged omnichannel retail powerhouse, Lenskart has redefined how India sees eyewear — quite literally.

As it prepares for its highly anticipated IPO, investors are asking a big question: Is Lenskart the next big thing — or just another overhyped consumer-tech play?

👓 The Lenskart Story: From Clicks to Bricks

Founded in 2010 by Peyush Bansal, Lenskart started as an e-commerce platform for eyewear when buying glasses online was unheard of in India. Over time, it evolved into a hybrid model combining online convenience with offline experience centers, a move that proved to be a game changer.

As of FY25, Lenskart operates over 2,500 stores across India and international markets (including Singapore, Dubai, and Riyadh) and serves over 20 million customers. It claims to add a new store every day, scaling with precision and consistency that few retail players can match.

The company’s secret sauce lies in its vertically integrated model — controlling everything from design and manufacturing to distribution and retail. Its state-of-the-art facility in Bhiwadi (Rajasthan) produces millions of lenses and frames annually, allowing for tighter margins and faster product turnaround.

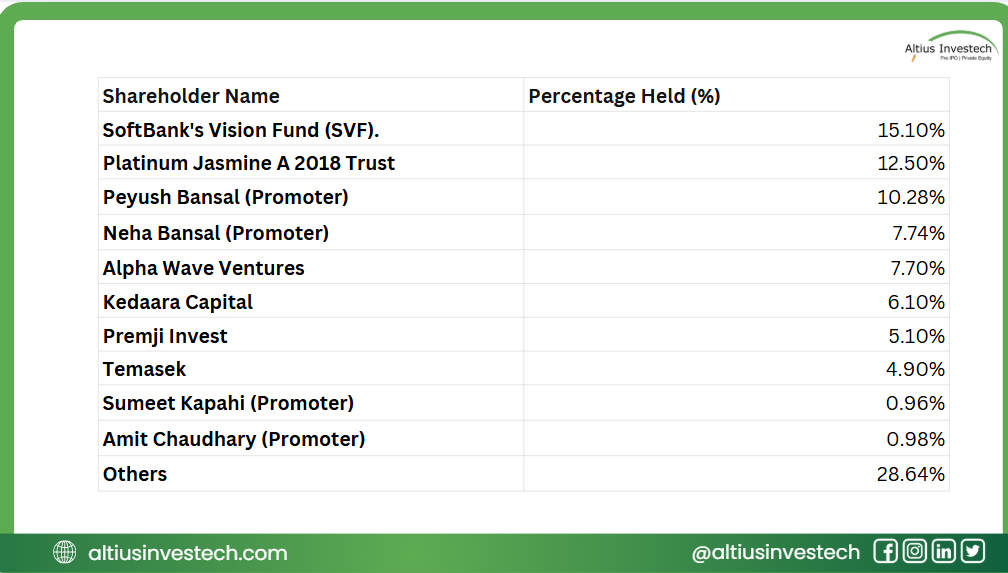

Ownership Structure:

Moat: Integration, Innovation, and Insight

Lenskart’s competitive edge lies in three interconnected strengths:

1. Vertical Integration

By manufacturing its own lenses and frames, Lenskart avoids middlemen margins, ensuring better pricing and quality control — a sharp contrast to traditional opticians relying on third-party suppliers.

2. Technology-Led Retail

AI-powered face scanning, 3D try-ons, and a data-driven inventory system make Lenskart a retail-tech hybrid. Its proprietary tech tracks user preferences and eye power patterns, allowing for customized recommendations.

3. Omnichannel Network

Over 70% of its customers interact with both online and offline touchpoints before purchase. This seamless blending of digital and physical retail gives it a defensible moat that neither Amazon nor traditional opticians can easily replicate.

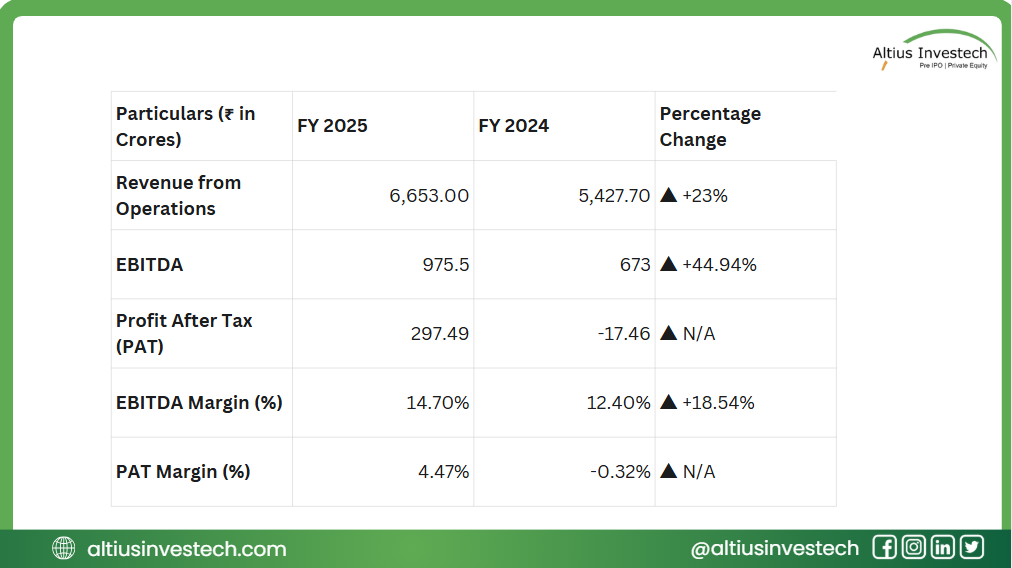

Financial Analysis

Insights:

1. Strong Growth and Operational Efficiency

- Revenue grew 23% YoY to ₹6,653 crore, driven by expansion across online and offline channels.

- EBITDA rose 45% to ₹975 crore, reflecting improved supply chain efficiency, cost control, and scale benefits.

2. Profitability and Scalability Gains

- Turned profitable with a PAT of ₹297 crore and margin expansion (EBITDA at 14.7%).

- Indicates maturing unit economics and the company’s ability to scale profitably after years of aggressive growth.

3. Strategic Expansion and Financial Strength

- Balanced omni-channel model (60% offline, 40% online) with growing presence in global markets.

- Backed by SoftBank, Temasek, and KKR, Lenskart remains cash-positive and focused on AI-driven automation and innovation to sustain growth.

⚠️ Red Flags: The Bear Case

1. Fragile Profitability

- Despite turning profitable, PAT margin is just 0.4%, leaving little cushion for cost increases or market disruptions.

- Sustaining profits amid expansion and marketing spend remains a major challenge.

2. Aggressive Growth & Valuation Pressure

- Continued reliance on rapid store expansion and global rollouts demands heavy capital and execution discipline.

- A high valuation (P/E ~384x) amplifies pressure to deliver consistent, strong growth.

3. Cash Flow & Operational Risks

- Profit growth not yet matched by strong cash flow conversion, with rising inventory and working capital needs.

- Increasing competition and international exposure could strain margins if efficiency weakens

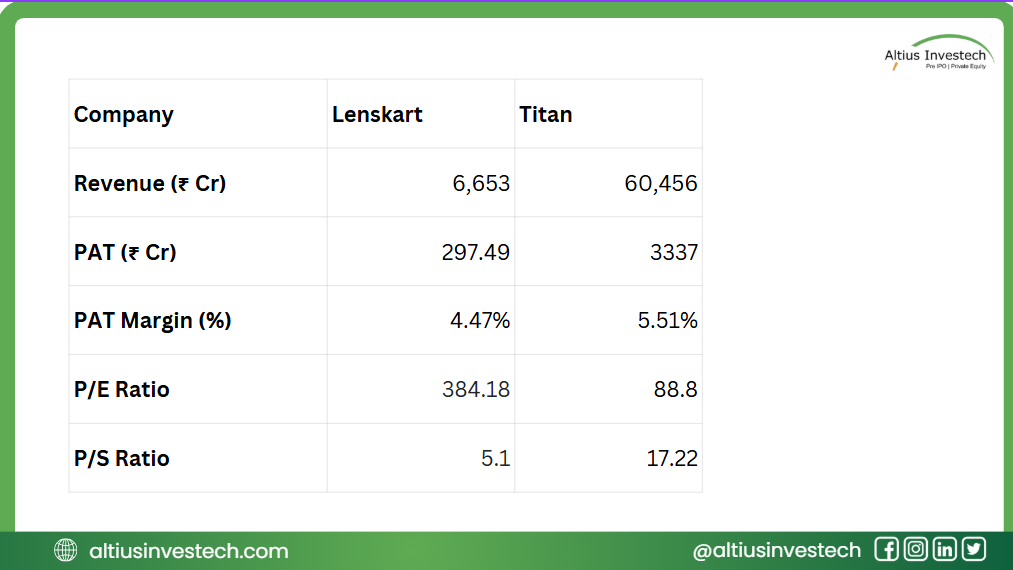

Peer Analysis

To get a relative idea, we can look at Titan another company operating in the retail eyewear space, though these are imperfect comparisons.

🏁 Final Take: Clear Vision, Blurred Valuation

The Lenskart IPO represents the next evolution of Indian consumer-tech — profitable, scalable, and built on solid fundamentals rather than vanity metrics. Its hybrid model, tech-enabled retail, and strong brand moat make it one of the few startups genuinely ready for public markets.

But for all its strengths, investors must remember: great businesses aren’t always great IPO buys.

With its rich valuation and concentration risks, this listing might suit long-term believers in India’s consumer upgrade story more than short-term traders chasing the next “Eyewear Unicorn” rally.

Bottom line:

Lenskart has perfect vision — but the market’s price tag might still need a little correction

Looking to invest in more high-potential companies like Lenskart ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of October 24th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)