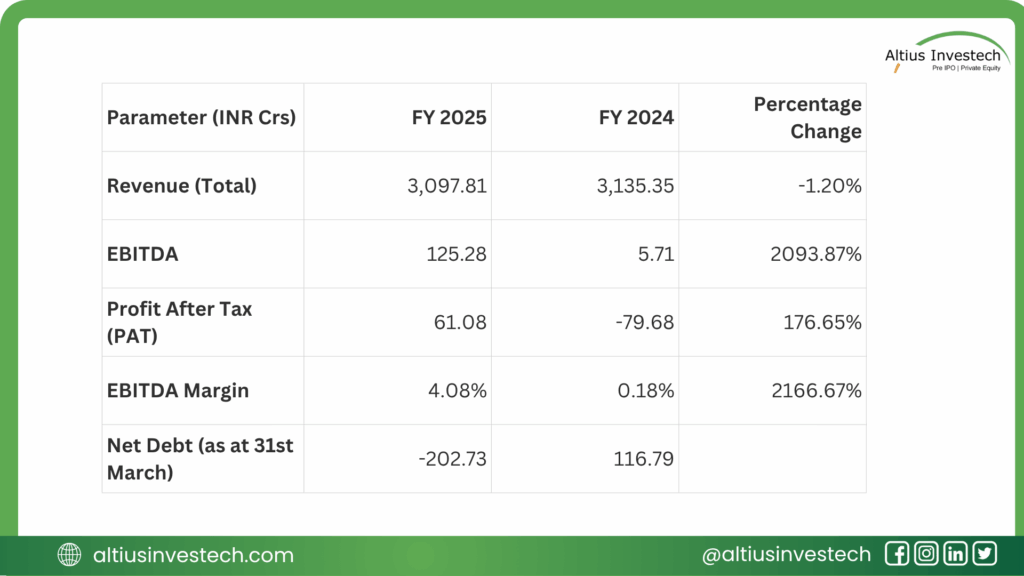

Imagine Marketing, the parent company of boAt, just dropped its annual report for FY2025. For a company speeding towards an IPO, it’s a story that demands a double-take. It just pulled off a stunning financial turnaround, swinging from an ₹80 Crore loss last year to a ₹61 Crore profit.

But as a seasoned analyst, I’ve learned that the headline number is never the full story. This impressive profit surge happened while revenue actually fell by 1.2%. This wasn’t a growth story; it was a cost-cutting story. And as the P&L was being polished, some serious risks have piled up on the balance sheet.

The Big Profit Swing: boAt is now profitable, reporting a ₹61 Cr PAT after a disastrous ₹80 Cr loss in FY24.

Stagnant Sales: This profit wasn’t fueled by growth. Revenue actually shrank by 1.2%.

The Ticking Liquidity Bomb: A massive ₹505 Crore liability (from preference shares) just became a “current” (due within 12 months) problem, crushing the company’s short-term liquidity ratio.

Massive Legal Risk: A new, uncertain ₹241 Crore contingent liability related to a customs dispute has appeared on the books.

Extreme Concentration: The company is dangerously reliant on just two customers for 65% of its entire revenue.

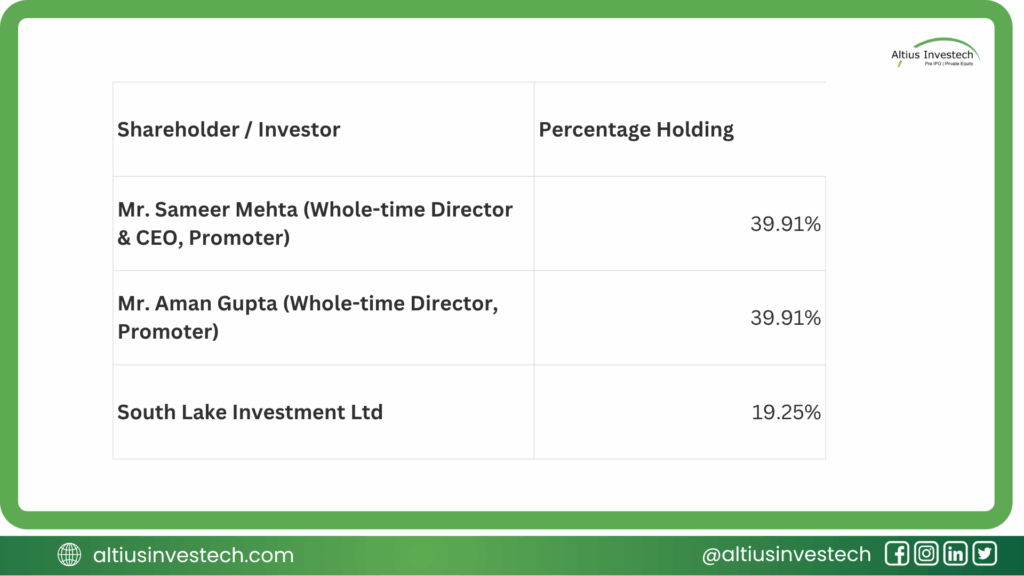

Ownership Structure:

The company is a classic founder-led story. The two co-founders, Mr. Sameer Mehta and Mr. Aman Gupta, are the dominant shareholders, ensuring their vision (and risk) is aligned with the company.

Before it was a ₹3,000 Crore giant, boAt was a bootstrapped startup founded in 2016 by Aman Gupta and Sameer Mehta. With a modest ₹30 lakh investment, their first product wasn’t a trendy earbud, but a humble Apple charging cable.

They identified a simple, universal problem: original cables were expensive and broke easily, while cheap knockoffs were unreliable. boAt launched a durable, stylish, and affordable cable, and it was an instant hit on e-commerce platforms.

This initial success gave them the insight and the capital to tackle their real target: the audio market. At the time, consumers had two choices: expensive, legacy international brands (like JBL, Sony) or cheap, unbranded, low-quality Chinese imports.

Aman Gupta, having previously worked at Harman (JBL’s parent company), knew the gap. He and Sameer Mehta created boAt to be the brand that filled that gap: aspirational yet affordable, stylish, and built for the Indian consumer. They focused on what mattered to the youth—heavy bass, durability, and celebrity-driven marketing. This brand-first, digital-native approach is the core of their “moat” and the reason they’ve become a cultural icon.

Financial Analysis

The FY25 story is one of aggressive, pre-IPO financial cleanup. The company successfully engineered a 2000%+ surge in its operating (EBITDA) margin from a razor-thin 0.18% to a healthier 4.08%.

Financial Insights:

How did profits surge while sales fell?

- Cost-Cutting, Not Growth: The turnaround was driven by operational efficiencies, primarily by cutting the massive losses in its Wearables segment.

- Lower Finance Costs: Finance costs were significantly reduced.

- Positive Cash Flow: The company generated an impressive ₹434 Crores in Free Cash Flow, allowing it to pay down debt and move to a Net Cash position of ₹203 Crores.

On paper, this looks like a masterclass in operational discipline. But this positive P&L narrative is hiding some serious balance sheet risks.

⚠️ Red Flags: Yellow Cards on the Field?

As an analyst, I’m less interested in the profit they just booked and more concerned about the risks they’re carrying forward.

- The ₹505 Crore Liquidity Crunch: This is the biggest red flag. A massive ₹504.6 Cr liability from Series C preference shares (CCPS) was suddenly reclassified from “non-current” to “current.” This means it’s due for repayment or conversion within 12 months. This single entry caused the Current Ratio to collapse from a healthy 1.71 to a precarious 1.05, indicating very little buffer to cover short-term obligations. The IPO is no longer just for growth; it’s a necessity to manage this liability.

- The ₹241 Crore Legal Battle: A new contingent liability of ₹241 Crores has emerged related to a Show Cause Notice from Customs authorities. This is a massive, uncertain cost hanging over the company, stemming from a dispute over the classification of its core products.

- The “Two-Client” Business: A staggering 64.55% of all revenue comes from just two customers. If either of these major distributors faces issues or negotiates harder terms, boAt’s entire business model is at risk.

- “Messy Books” & Auditor Remarks: The annual report is littered with “material prior period errors” and “restatements” from FY24. The auditor also had unfavorable remarks on the holding company’s maintenance of books. For a company about to ask for thousands of crores from the public, this indicates a significant weakness in its internal financial controls.

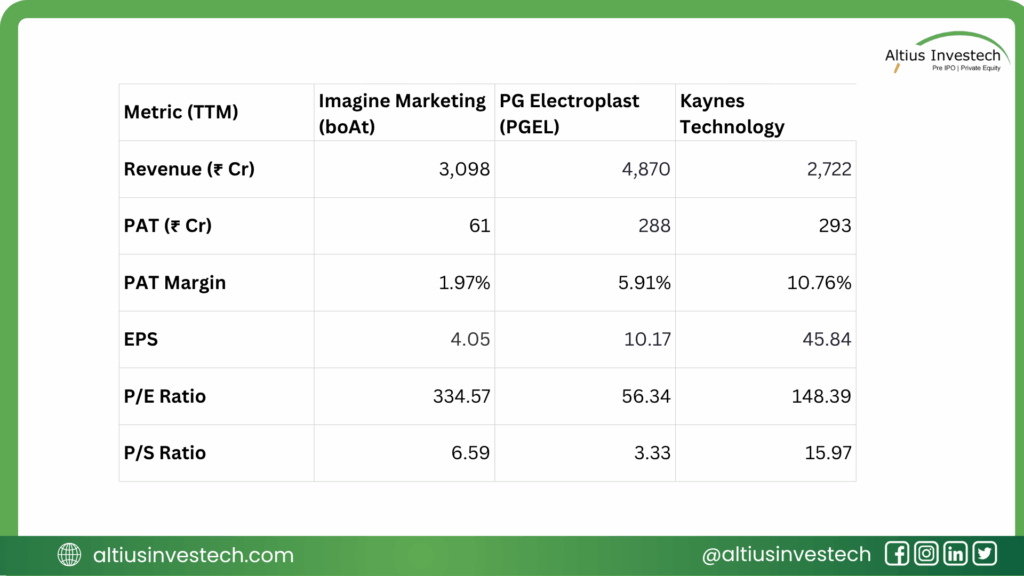

Peer Analysis: The Brand vs. The Manufacturers

This comparison is brutal. It shows that the companies making the electronics are significantly more profitable than the brand selling them.

- Kaynes Technology, with a similar revenue of ₹2,722 Cr, delivered ₹293 Cr in profit, while boAt delivered only ₹61 Cr.

- The market is paying a massive premium for these high-growth EMS players (P/E of 148x for Kaynes!), betting on the “Make in India” story.

- This places boAt in a tough position: its 2.0% net margin is razor-thin, suggesting it has very little pricing power against its suppliers (the EMS companies) and its customers (the two big distributors).

Conclusion: Refining the Investment View

boAt’s IPO-bound story is a classic tale of two books. The P&L has been beautifully cleaned up to show a dramatic swing to profitability—a “must-have” for any public offering. The company is now net-cash positive and generating strong free cash flow.

However, the Balance Sheet and the business risks tell a much scarier story. The company is walking a tightrope with a massive short-term liability (₹505 Cr), a huge potential legal bill (₹241 Cr), and a business model that is almost entirely dependent on just two clients.

This is a high-risk, high-reward bet on a powerful brand. Investors are being asked to buy into the brand’s strength—a brand that grew from a simple charging cable—while underwriting a long list of very real, very large financial and operational risks.

Looking to invest in more high-potential companies like boAt ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)