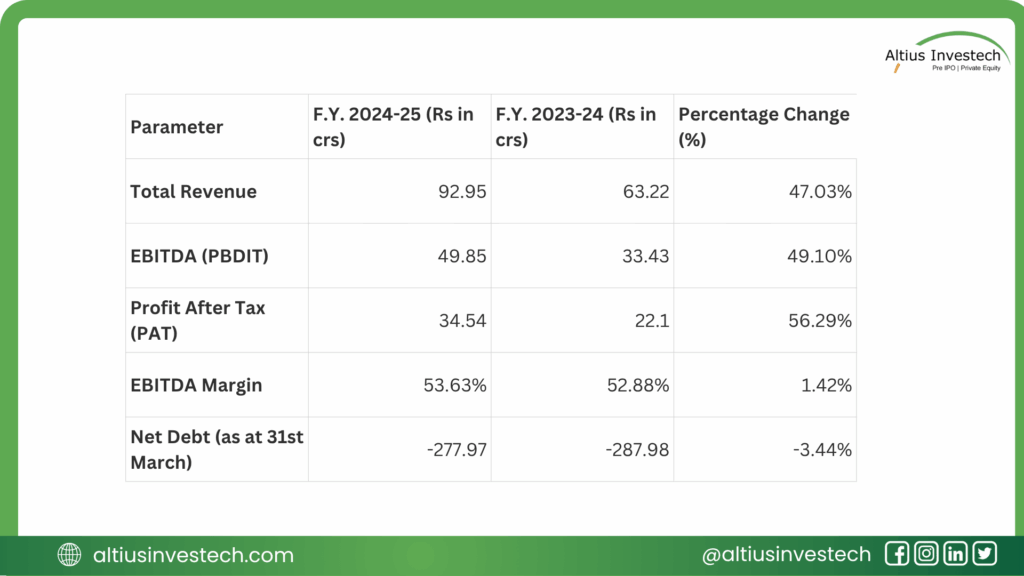

Power Exchange India Limited (PXIL) just released its annual report, and on the surface, it’s a masterpiece. Revenue is up 47%. Net Profit has skyrocketed 56%. The company boasts an incredible 53.6% operating margin and is sitting on a massive pile of net cash.

So why, as a seasoned analyst, am I so concerned?

Because when you flip from the profit statement to the cash flow statement, the story completely reverses. Last year, PXIL generated ₹165 Crores in cash from its operations. This year, it burned ₹16.5 Crores.

This is the central enigma of PXIL: it’s a tale of two companies. One is a high-growth, high-profit machine. The other is a business that’s suddenly stopped generating cash. Let’s dive in.

Stunning P&L Growth: The profit and loss statement is beautiful. Revenue surged 47% to ₹93 Cr, and Net Profit soared 56% to ₹34.5 Cr.

Elite Profit Margins: The company has a 53.6% EBITDA margin, making it an incredibly efficient, high-profitability business.

The Cash Flow Crisis: This is the #1 red flag. Operating Cash Flow (OCF) swung from a +₹165 Cr inflow in FY24 to a -₹16.5 Cr outflow in FY25. Free Cash Flow is also negative.

The Culprit: This isn’t a case of customers not paying. The cash drain is due to a massive, ₹44 Cr swing in “Payables for purchase of investments,” blurring the lines between operations and investing.

The Future: PXIL is at a crossroads, with a “market coupling” pilot underway (which could reshape the industry) and a strategic push into new areas like a Coal Exchange.

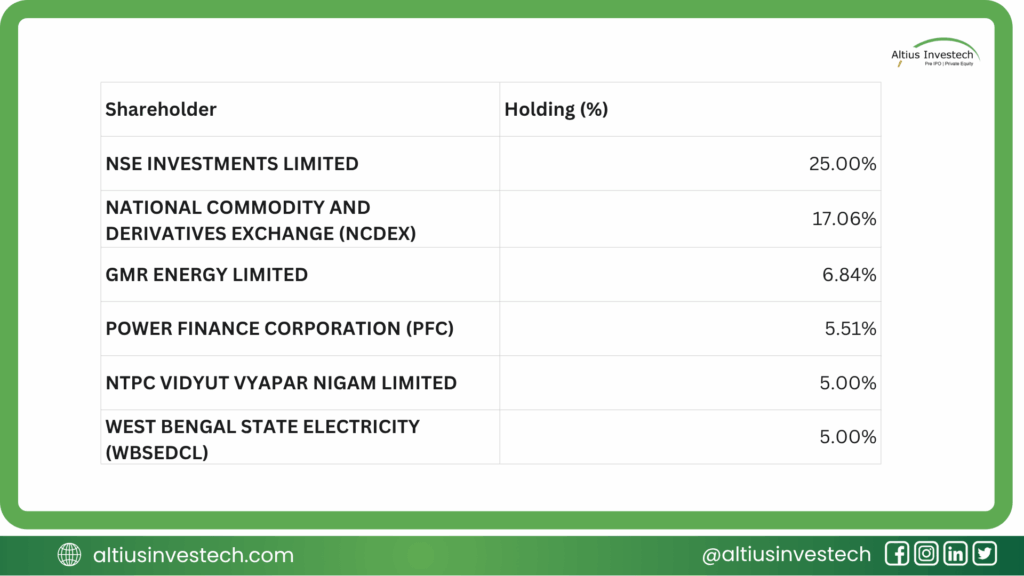

Who Owns PXIL? A Fortress of Institutions

This is not a founder-led startup. PXIL is owned by a “who’s who” of India’s financial and power infrastructure. This is a massive strategic strength.

This ownership provides immense regulatory and capital credibility. It’s a “too big to fail” consortium of backers, suggesting stability and deep market integration.

Financial Analysis

📈 The Financial Deep Dive: A Tale of Two Reports

The PXIL story is a perfect lesson in why you must read all three financial statements. The P&L tells you what they earned. The Cash Flow Statement (CFS) tells you what they kept.

The “Good News” (The Profit & Loss Statement)

The P&L is flawless. The company is in a high-growth phase and is scaling beautifully. It’s growing revenue at 47% while simultaneously expanding its already-high margins. This is the dream scenario for an investor.

The “Bad News” (The Cash Flow Statement)

This is where the record scratches. Despite reporting ₹50 Crores in EBITDA, the company’s cash flow from operations was negative ₹16.5 Crores.

- Free Cash Flow (FCF) FY24: +₹162.4 Crores

- Free Cash Flow (FCF) FY25: -₹17.7 Crores

How is this possible? The report shows that the company’s operating cash flow was wiped out by a massive ₹44 Crore outflow for “Payables for purchase of investments.” This suggests the company’s “operations” are heavily intertwined with its treasury and investment activities. While the balance sheet is still loaded with ₹278 Crores in net cash, you cannot ignore that the core business consumed cash this year.

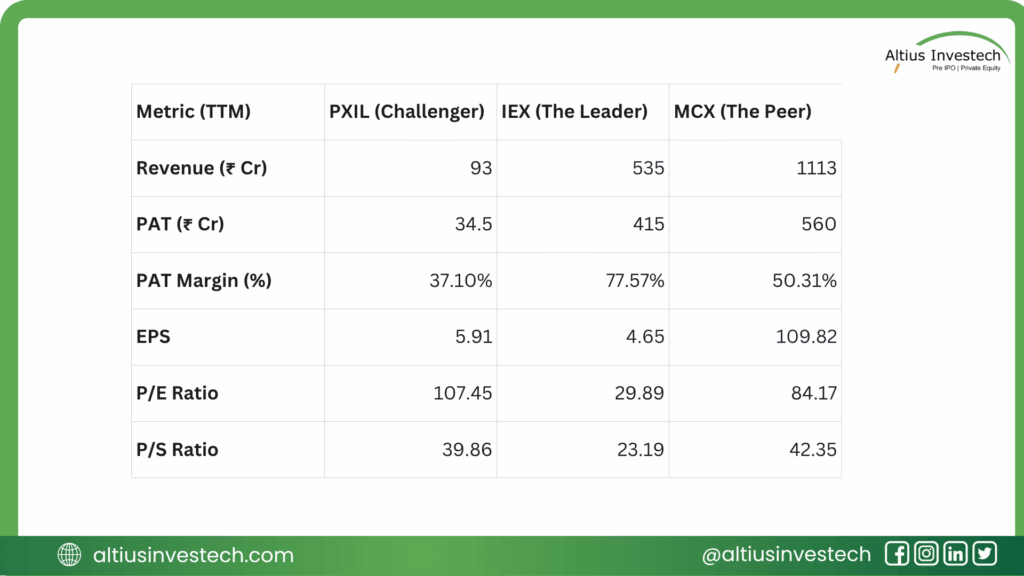

Peer Analysis: The Challenger vs. The Champions

PXIL is a challenger in a market dominated by giants. Its direct competitor is the Indian Energy Exchange (IEX), and a relevant peer is the Multi Commodity Exchange (MCX).

A David vs. Goliath Scenario: PXIL is a tiny fraction of the size of IEX, which is the undisputed 800-pound gorilla in the power exchange market.

Incredible Profitability: The exchange business model is a license to print money. IEX’s 77.57% net profit margin is staggering. PXIL’s 37.1% is also exceptionally strong, showing the duopolistic nature of the market.

The Growth Story: As the smaller player, PXIL’s 47% revenue growth is its key selling point. It is growing much faster than the incumbent IEX, signaling it is successfully capturing market share.

Conclusion: Refining the Investment View

Financially Robust Core: PXIL is not a struggling company. Its core business is fundamentally sound, highly profitable (53.6% EBITDA margin), and rapidly growing (47% revenue growth). The 56% PAT jump is real on an accrual basis.

A “Cash Flow Discount” is Warranted: The negative operating cash flow is a serious, non-negotiable red flag. Investors must apply a “risk discount” to their valuation until management can prove this was a one-time anomaly and not a structural flaw in its treasury management.

Valuation Hinges on the Growth Narrative: The entire investment thesis for PXIL is that it is the “growth” stock in a mature duopoly. Its value is tied to its ability to continue to outpace IEX and capture market share, especially as new markets (like the proposed Coal Exchange) open up.

The Bottom Line: This is an opportunity to invest in a high-margin, high-growth, institutionally-backed challenger. However, it’s a “profit vs. cash” paradox. The investment is suitable for investors with a strong risk appetite who believe the 56% profit growth is the real story and that the negative cash flow is just temporary noise.

Looking to invest in more high-potential companies like Power Exchange India Limited (PXIL) ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)