As a seasoned analyst, I’ve seen my share of “bad quarters.” But the FY2025 annual report for Spray Engineering Devices Limited (SEDL) isn’t just a bad quarter; it’s a story of a severe operational breakdown.

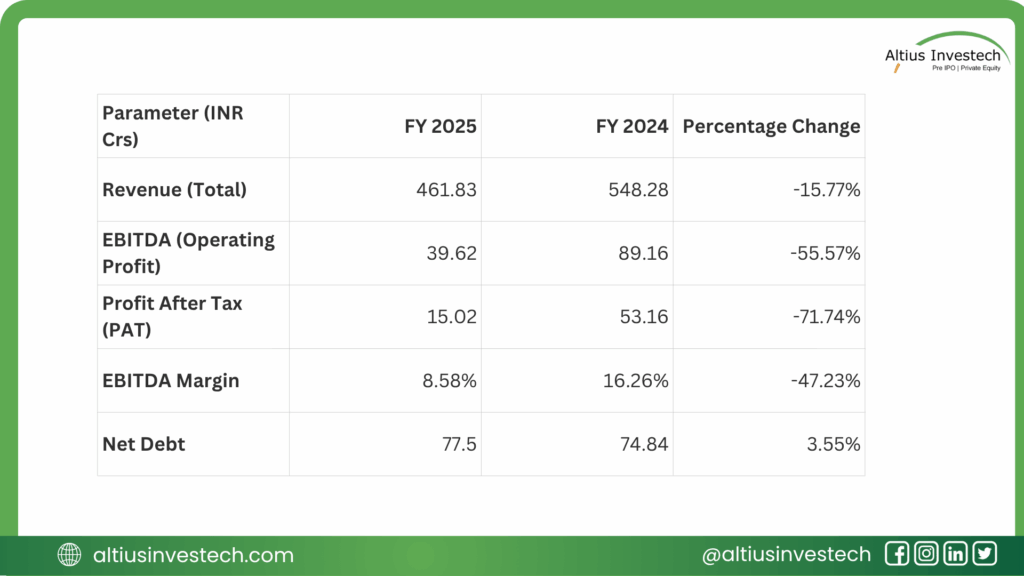

Revenue is down 16%, EBITDA collapsed by 56%, and Net Profit has evaporated by 72%.

But here’s the paradox: if you only looked at the balance sheet, you might think things are fine. The company’s debt-to-equity ratio actually improved.

How is this possible? Because while the business was hemorrhaging cash, it was simultaneously saved by a ₹67 Crore equity “lifeline” from investors. This is a classic case of a capital raise masking a deep operational failure. Let’s break down the two conflicting stories.

Massive Profit Collapse: Net Profit was virtually wiped out, falling 72% from ₹53.16 Cr to just ₹15.02 Cr.

The Cash Flow Crisis: The business is no longer funding itself. Operating Cash Flow swung from a ₹19.1 Cr inflow to a ₹28.8 Cr outflow. This is a massive -₹48 Cr reversal.

The “Equity Bailout”: The only reason the balance sheet looks stable is a ₹67 Crore fundraise. This new cash improved the debt-to-equity ratio, but it doesn’t fix the broken core business.

The Debt Risk: The company’s ability to service its debt from its earnings has collapsed. The Debt Service Coverage Ratio (DSCR) plummeted from a healthy 13x to a risky 3.4x.

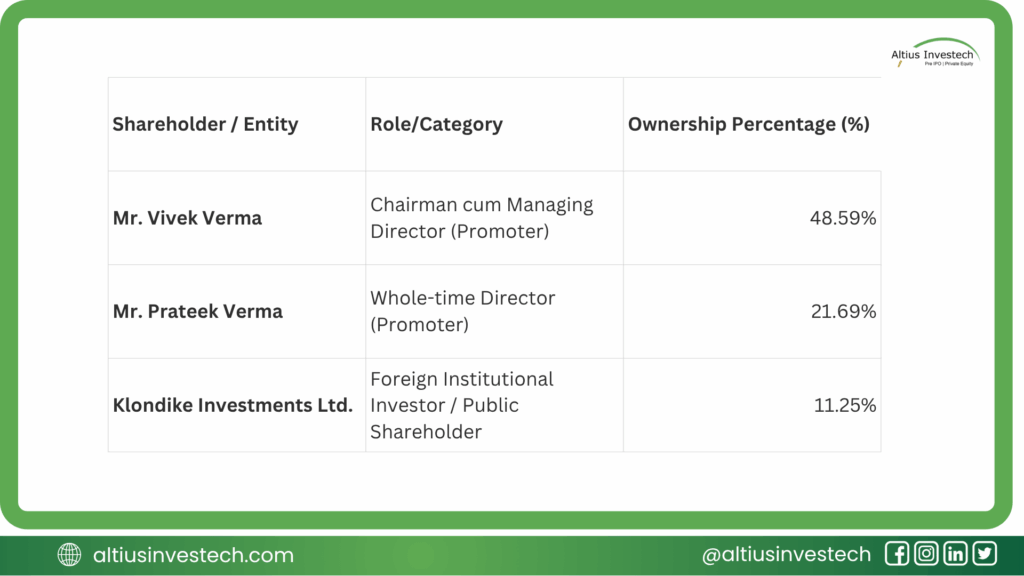

Who Owns SEDL?

The company is very tightly controlled by its promoters, who own over 70% of the company. This means high alignment, but also high concentration risk.

Financial Analysis

📈 The Financial Deep Dive: A Tale of Two Reports

The FY25 financials tell two completely different stories. The P&L and Cash Flow statements show a company in deep trouble, while the Balance Sheet shows a successful (and timely) repair.

The P&L and Cash Flow: A Story of Operational Failure

The company’s core business, which supplies tech to sugar and wastewater industries, hit a wall. Sales fell 16%, but costs rose, crushing profitability.

The real emergency is in the cash flow. A negative ₹28.8 Cr in operating cash flow means the day-to-day business is no longer paying for itself. This was driven by a disastrous blow-up in working capital:

- Inventories swelled by ₹38 Cr.

- Receivables (money owed by customers) jumped by ₹27 Cr.

This is the worst-case scenario: sales are falling, but you are failing to collect cash and are left holding more unsold inventory.s suggests the company’s “operations” are heavily intertwined with its treasury and investment activities. While the balance sheet is still loaded with ₹278 Crores in net cash, you cannot ignore that the core business consumed cash this year.

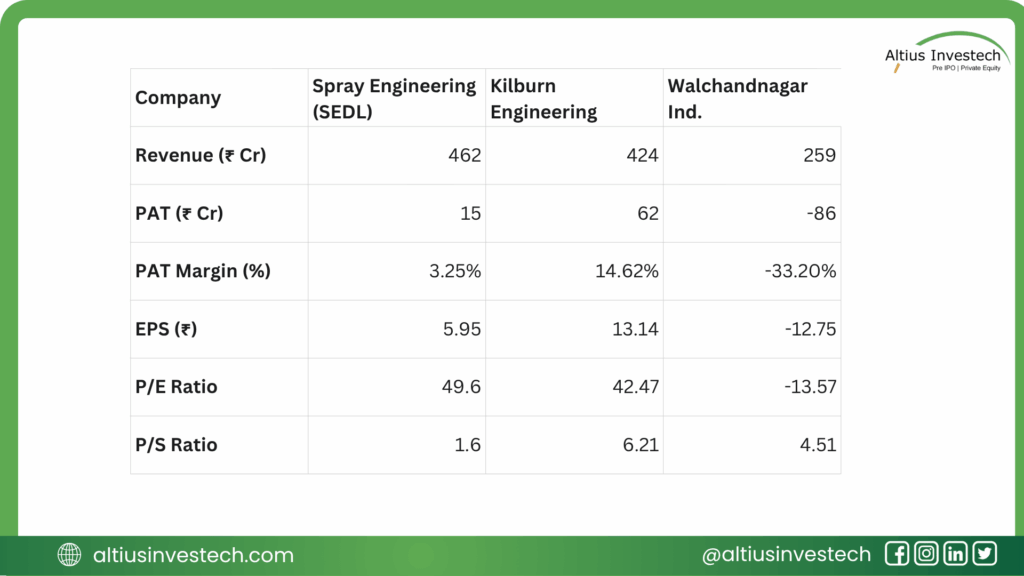

Peer Analysis: A Troubling Valuation Story

This is where the story gets truly concerning for SEDL. When we compare it to peers in the same revenue ballpark, its valuation appears entirely disconnected from its performance. The market seems to be pricing it based on hope, not financial reality.

We will compare SEDL to Kilburn Engineering, a high-quality peer, and Walchandnagar Industries, a loss-making peer.

This comparison reveals a deeply flawed valuation for Spray Engineering.

P/S Disconnect: The Price-to-Sales (P/S) ratio tells the real story. The market values SEDL’s sales at a paltry 1.6x. This is far lower than Kilburn (6.2x) and, shockingly, even lower than the loss-making Walchandnagar (4.5x).

The “Best-in-Class” Peer (Kilburn): Kilburn Engineering is the star of this group. It has similar revenue to SEDL but is vastly more profitable, with a robust 14.6% PAT margin compared to SEDL’s meager 3.3%. The market rightfully rewards Kilburn’s high-quality sales, giving it a strong P/S ratio of 6.2x.

The “Laggard” Peer (Walchandnagar): This company is a financial disaster, posting a massive ₹86 Crore loss on just ₹259 Crore in sales.

The SEDL Anomaly: This is where it gets irrational.

P/E Disconnect: SEDL is trading at a P/E of 49.6x, which is higher than its far more profitable peer, Kilburn (42.5x). The market is paying a premium for every rupee of SEDL’s low-quality profit.

Conclusion: Refining the Investment View

Profitability Collapse: The company suffered a catastrophic operational setback in FY 2025. A 72% drop in net profit and a 47% collapse in EBITDA margins signal a severe loss of cost control.

Working Capital and Cash Crisis: The operational failure is compounded by a massive working capital drain. The business is burning cash, with a disastrous EBITDA-to-CFO conversion rate of -74%.

The Equity Lifeline: The only reason the balance sheet looks stable (Debt/Equity 0.39x) is the ₹67 Crore equity infusion. This new cash did not come from operations; it came from new investors, and it is masking the severe cash burn from the core business.

Heightened Debt Risk: The Debt Service Coverage Ratio (DSCR) plummeted from a safe 13x to a risky 3.4x. This shows the company’s ability to pay its debts from its earnings has been severely weakened.

Concluding Perspective: To use an analogy, the SEDL ship is taking on heavy water from massive operational leaks. The ₹67 Cr fundraise was a timely patch that keeps it afloat for now. But the internal cash pumps are failing, and the engine is sputtering. The market’s high valuation (49.6x P/E) seems entirely disconnected from this reality, pricing in a heroic recovery that the data does not yet support.

Looking to invest in more high-potential companies like Spray Engineering Devices Limited (SEDL) ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)