The National Stock Exchange’s (NSE) latest results for Q2 FY26 are complex, and the headline numbers can be misleading. At first glance, the reported figures show a significant drop.

Reported profit showed a 33% year-over-year decline, and reported operating margins were 40%, down from 74%. However, this was almost entirely due to a single, strategic accounting decision.

Reported Profits Mask the Core Story: This provision obscured the quarter’s underlying performance…

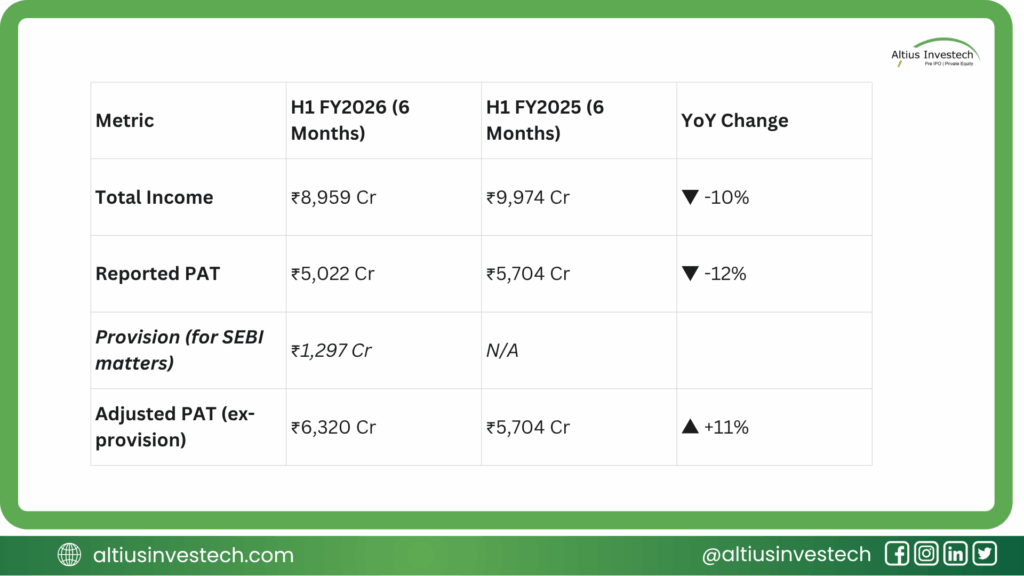

The entire narrative of Q2 FY26 is defined by one number: ₹1,297 crore.

For investors, this is a classic “clean slate” move. Management is taking a decisive, one-time charge to provision for these legacy regulatory matters, signaling a desire to put the past to bed.

Financial Analysis

📈 The Financial Deep Dive: A Slowdown in the Core

The real story for analysts is what’s happening underneath the provision. The core business is facing a cyclical slowdown. The post-pandemic trading boom is cooling off, and this is the first clean look we’ve had at the new “normal.”

For the first half of the year (H1 FY26), reported revenue and profit are down. But as investors, we must look at the adjusted numbers to see the true health of the business.

The real emergency is in the cash flow. A negative ₹28.8 Cr in operating cash flow means the day-to-day business is no longer

Analysis: The key takeaway is that despite a 10% drop in total income, the company’s underlying (adjusted) profit grew by 11%.

How is this possible?

Aggressive Cost-Cutting: NSE management proved they can protect the bottom line. Total expenses (ex-provision) fell by a massive 26% in H1. This includes a 36% drop in regulatory fees and a 30% drop in “other expenses” (ex-provision). This demonstrates incredible operating leverage.

Trading Slowdown: The revenue drop is real. Transaction charges, the main engine, fell 18% in H1. Average daily volumes in Q2 were down sharply across the board: Cash Market (-26%), Equity Futures (-30%), and Equity Options (-29%) compared to the prior year.

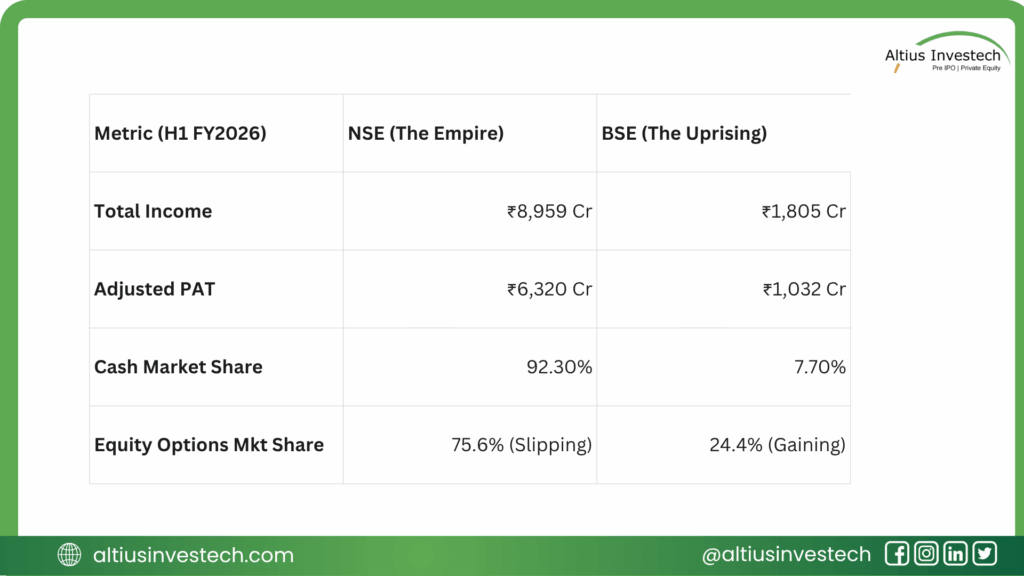

🛡️ Peer Analysis: The Empire vs. The Uprising (NSE vs. BSE)

For the first time in years, we have a real competitive story. The battle is no longer a monopoly; it’s a duopoly, and the fight is for the lucrative derivatives market.

The First Blood: NSE’s own data shows its equity options market share slipped from 78.6% in Q1 to 75.6% in Q2. This 3% shift in a single quarter is the most significant competitive dynamic in the Indian market today. While NSE is still the world’s largest derivatives exchange, it is no longer the only choice.

The Scale: Let’s be clear: NSE is a fortress. It is nearly 5 times the size of BSE by revenue and 6 times larger by adjusted profit. Its 92.3% share of the cash market is a virtual monopoly and a massive cash cow.

The Real Battleground: The cash market is a settled war. The real war is in Equity Options, the main profit driver for both exchanges. Here, BSE has successfully carved out a significant ~24% market share. This is not a small feat; it’s a direct, effective assault.

Concluding Perspective: The Analyst’s Take

This was a messy, painful, but ultimately necessary quarter for NSE.

- The Core Business: The fortress is intact, but the post-COVID high-growth party is over. The 18% drop in core revenue is a real headwind, and investors must now model for a more mature, cyclical growth rate.

- The “Governance Discount”: The ₹1,300 crore provision is a backward-looking event. The bull case is that this “kitchen sink” quarter finally cleans the slate from old governance issues, potentially reducing the “governance discount” that has weighed on its valuation.

- The New War: The investment thesis for NSE has shifted. It’s no longer just a hyper-growth monopoly. It’s a high-margin, high-moat, operational-excellence story that must now actively fight a re-energized competitor (BSE) in its most profitable segment.

Final Take: This was a “rip the band-aid off” moment. The headline numbers are ugly, but they mask an operationally brilliant quarter in terms of cost control. The real concern isn’t the one-time provision; it’s the revenue slowdown combined with the first real taste of competition. Watch NSE’s derivative market share in the coming quarters—that is the new battleground.

Looking to invest in more high-potential companies like The National Stock Exchange’s (NSE) ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)