The FY2025 annual report for the IPO-bound Veritas Finance is a perfect case study in this “Growth vs. Risk” paradox.

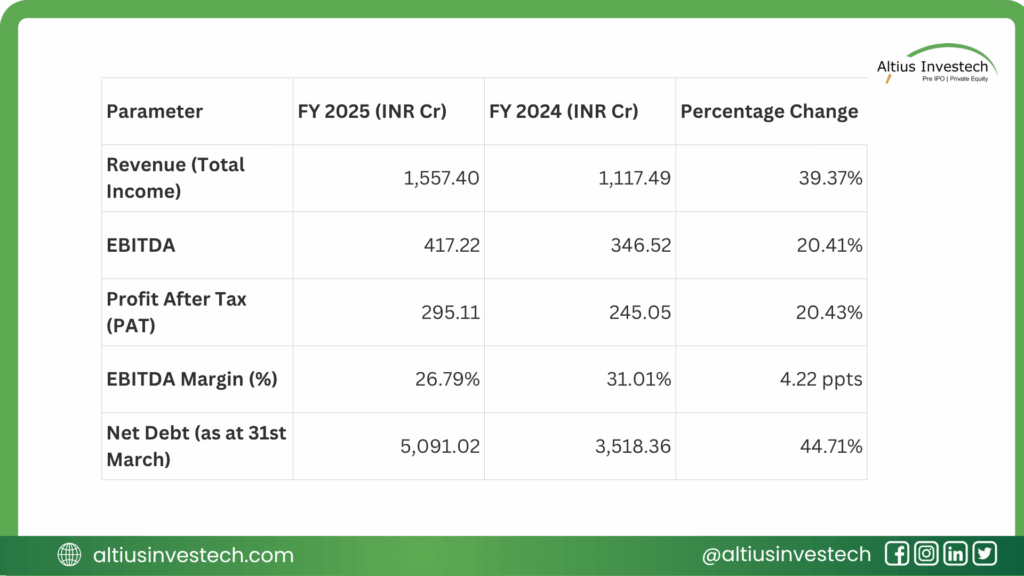

On one hand, the company is a growth juggernaut. Revenue surged 39%, and the loan book grew by over 28%. The balance sheet is a fortress, with a Capital Adequacy Ratio (CRAR) of 37.8%, more than double the regulatory need.

But this growth is coming at a steep price. Net Profit growth was only 20.4%, lagging revenue by half. Why? Because the cost of this growth is exploding. Finance costs are up 54%, and more alarmingly, impairments for bad loans skyrocketed by 90%.

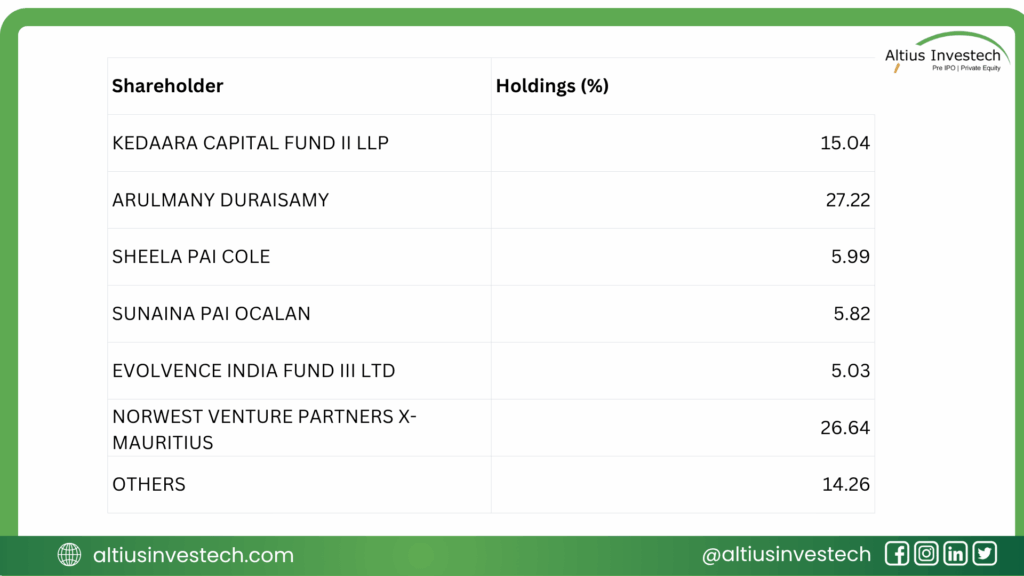

👑 Who Owns Urban Tots? A Tightly Controlled Ship

Veritas’s ownership structure is a blend of a strong founder-promoter and marquee private equity backers. This is a classic pre-IPO setup. The founder, Arulmany Duraisamy, holds the largest stake (27.2%), ensuring a founder’s vision. He is backed by a “who’s who” of smart-money investors, including Norwest Venture Partners (26.6%) and Kedaara Capital (15.0%). This PE backing brings high-level governance and a clear focus on an “exit” — i.e., the upcoming IPO.

Financial Analysis

📈 The Financials: A Story of Margin Compression

The FY25 P&L tells a story of “profitless prosperity.” The company is getting bigger, but not richer, as the cost of growth is eating into its margins.

Financial Insights:

The disconnect is clear. Revenue grew by 39%, but PAT grew by only 20.4%. The “why” is the real story:

- Cost of Funds: Net Debt jumped by 45% to fuel the loan book. Unsurprisingly, Finance Costs surged by 54% to ₹483 Cr.

- The Credit Problem: This is the big red flag. Impairment on financial instruments (provisions for bad loans) exploded by 90% to ₹171 Cr.

Management even admitted to “stress in certain urban pockets of short-term working capital loans,” blaming customers falling “prey to the easy availability of digital loans at significantly higher rate of interest.” This is a clear sign that asset quality is deteriorating in their high-yield unsecured segment.

🚩 The Auditor’s “Audit Trail” Red Flag

For an IPO-bound company, this is a major issue. The auditors noted that the company’s accounting software “audit trail (edit log) feature was not enabled throughout the year.”

This is a critical internal control failure. An audit trail is a mandatory feature that records every change made to the financial data. Without it, data integrity cannot be fully guaranteed. This is a significant governance gap that public market investors will not take lightly.

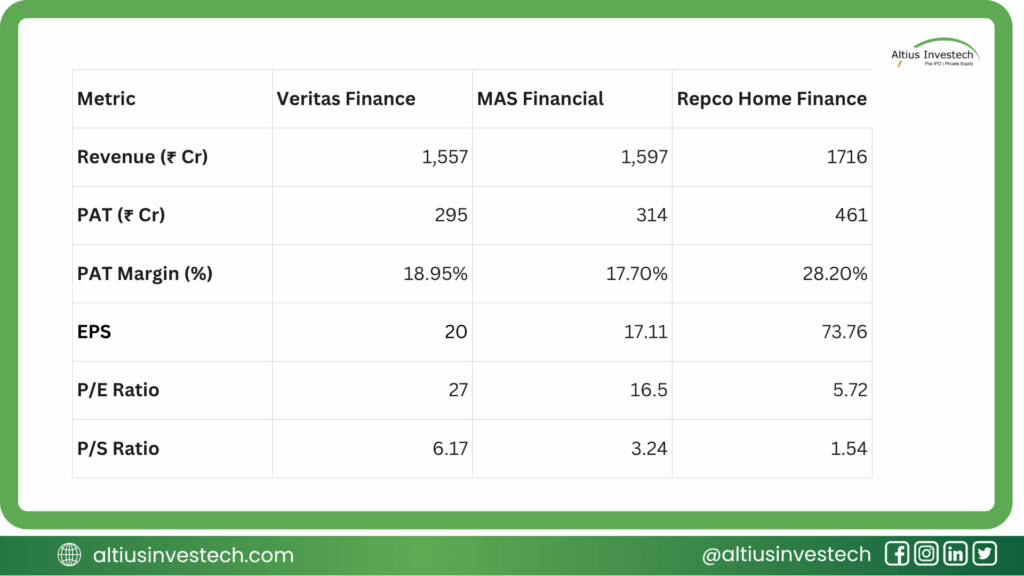

📊 Peer Analysis: A High-Growth, High-Risk Valuation

This comparison reveals three very different investment profiles, even though all three companies have a similar revenue scale.

The market is clearly telling a story about Value vs. Growth.

TThis table shows a clear disconnect between profitability and valuation, which is key to understanding the investment thesis.

Its P/S ratio of 6.17x is double that of MAS and four times that of Repco.

Repco Home Finance (The “Value” Play): Repco is the most profitable and efficient company in the group by a huge margin. It boasts a 28.20% PAT margin and generates the highest absolute profit (₹461 Cr). However, the market assigns it a rock-bottom P/E ratio of 5.72x and a P/S of 1.54x. This signals that investors see Repco as a mature, slow-growth “value” stock, likely a secure cash cow with limited upside.

MAS Financial (The “Growth at a Reasonable Price” Play): MAS Financial is the “middle-of-the-road” stock. Its profitability is solid (17.7% margin), and its valuation is reasonable (16.5x P/E). The market views it as a stable, reliable grower, balancing growth and value.

Veritas Finance (The “Hyper-Growth” Play): This is the most critical insight. Veritas has a PAT margin (18.95%) similar to MAS Financial but is far less profitable than Repco. Despite this, it commands the highest valuation of the entire group.

Its P/E ratio of 27.0x is significantly higher than its peers.

Conclusion: Refining the Investment View

The market is pricing Veritas as a premium, high-growth company. It is not valuing the company based on its current profits, which are lower than Repco’s. It is paying a premium based on its 39% revenue growth story.

Investors are betting that Veritas’s rapid expansion will allow its earnings to grow much faster than its peers, justifying the high price. An investment in Veritas is a clear bet on future growth, whereas an investment in Repco is a bet on current value. The upcoming IPO will be a test of whether public market investors agree with this premium “hyper-growth” valuation, especially given the rising credit costs.

Looking to invest in more high-potential companies like Veritas Finance?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)