While the market chases established renewable names, a quiet storm has been brewing in the unlisted space. Onix Renewable Limited just dropped its FY 2024-25 numbers, and they are nothing short of explosive.

The company has officially crossed the ₹1,000 Crore revenue milestone, delivering triple-digit growth that outpaces almost every major listed peer. But with a 91% promoter holding and missing cash flow data, is this a perfect growth story or a “watch from the sidelines” play?

Let’s dive into the numbers.

🚀 Quick Take: The 165% Growth Explosion

The headline number is the sheer velocity of growth. Onix hasn’t just grown; it has multiplied.

The Driver: This wasn’t luck. It was a strategic execution of government mandates like PM-KUSUM and Solar-Wind Hybrid projects, proving the company can execute at scale.

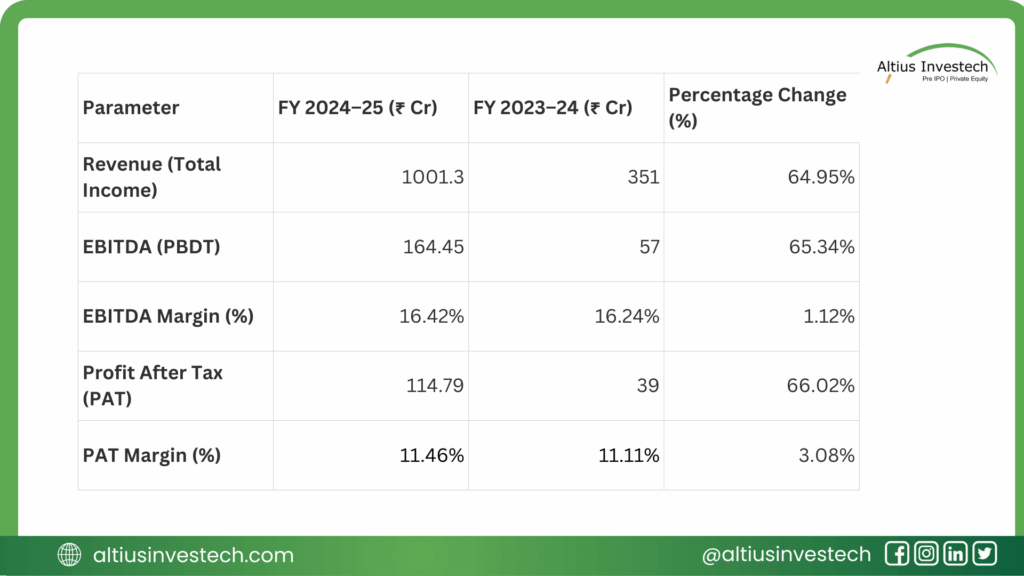

Revenue Rocket: Top-line revenue surged 165%, jumping from ~₹351 Cr to ₹1,001.3 Cr in a single year.

Profit Power: Net Profit (PAT) grew even faster at 166%, landing at ₹114.8 Cr.

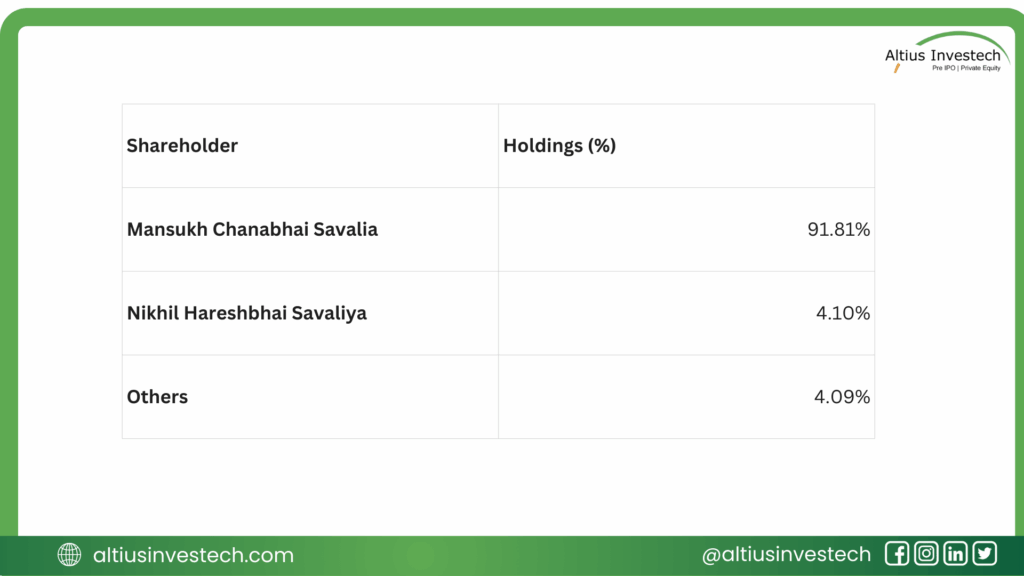

👑 Ownership: A One-Man Show?

Unlike the diverse boards of its Peers, Onix Renewable is tightly controlled by a single individual. The promoter holding is exceptionally high, which tells a unique story of conviction but also concentration.

Skin in the Game: With ~92% ownership, the promoter Mansukh Chanabhai Savalia effectively is the company. This level of “skin in the game” ensures rapid decision-making and total alignment with the business’s success.

The Double-Edged Sword: While this structure allows for agility, it also raises questions about key-man risk and the lack of a diverse board or institutional checks and balances a key factor to watch if the company moves towards an IPO.

Financial Analysis

📊 The Financial Scorecard: Anatomy of a Hyper-Growth Sprint

The financial statements for FY25 reveal more than just big numbers; they show a company undergoing a fundamental change in scale. Onix Renewable didn’t just grow; it vaulted into a new league.

Crossing the ₹1,000 Crore revenue mark is a critical milestone for infrastructure companies it’s the threshold where execution capability is proven, and economies of scale usually kick in.

Financial Insights:

1. The “Triple-Digit Lockstep” (Quality of Growth) In the infrastructure and EPC (Engineering, Procurement, and Construction) sector, it is common to see companies “buy revenue” by taking on low-margin projects just to bloat the top line.

- The Insight: Onix avoided this trap. Its Revenue (165%), EBITDA (165%), and PAT (166%) grew in perfect lockstep. This indicates “Quality Growth.” The company didn’t sacrifice profitability to gain market share; it scaled its operations efficiently without diluting the quality of its earnings.

2. Margin Resilience in a Hyper-Growth Phase Usually, when a company triples its size in 12 months, operational chaos ensues, and margins shrink due to inefficiencies or aggressive pricing.

- The Insight: Onix actually expanded its margins. The EBITDA margin ticked up to 16.42%, and the Net Profit margin improved to 11.46%. This suggests strong cost controls and economies of scale—as they bought more solar panels and wind turbines, they likely negotiated better prices, squeezing out more profit from every rupee of revenue.

3. The “Missing Link”: Cash Flow Transparency While the P&L (Profit & Loss) statement is stellar, an astute investor must look for the holes in the story.

The Caution: The report lacks detailed Cash Flow data. In the renewable sector, “Revenue” is often recognized based on project completion milestones, not necessarily when the cash hits the bank. With such massive growth, working capital needs (money tied up in inventory and receivables) usually skyrocket. Without seeing the Cash Flow from Operations (CFO), we cannot confirm if this ₹114 Cr profit has successfully been converted into cash or is stuck as unpaid invoices from government clients.

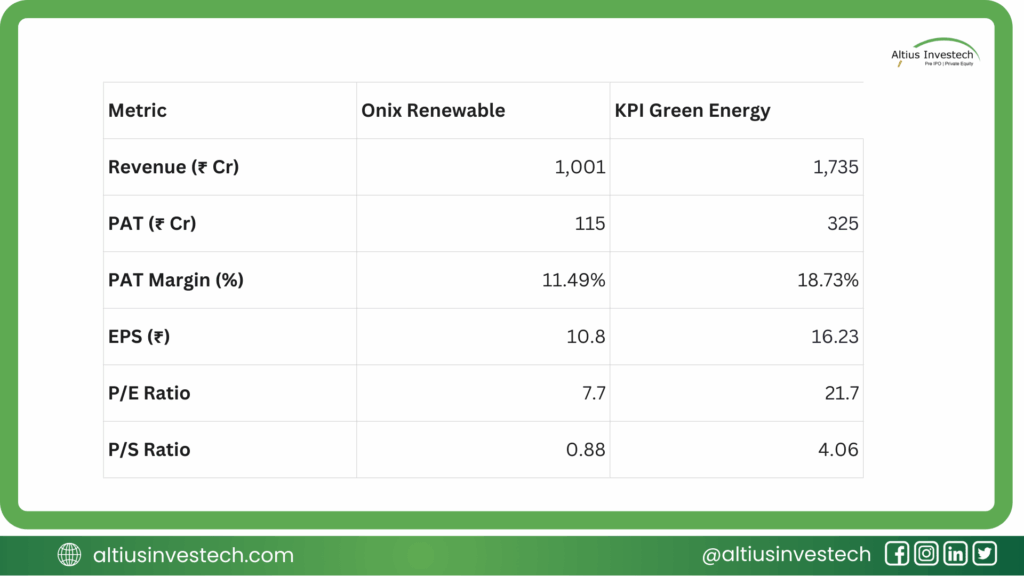

⚔️ Peer Analysis: The Undervalued Challenger vs. The Premium Leader

To understand the investment potential of Onix Renewable, we must stack it up against a listed benchmark. KPI Green Energy is the perfect peer—it operates in the same sector but commands a much higher valuation.

A side-by-side comparison reveals a massive valuation gap that defines the investment thesis.

The “Value” Arbitrage

1. The Valuation Chasm (7.7x vs. 21.7x) This is the most striking takeaway. Investors are paying 21.7 times earnings for KPI Green, but only 7.7 times earnings for Onix.

- The Opportunity: Onix is trading at a 65% discount to its listed peer on a P/E basis. If Onix were to trade at even half of KPI’s multiple (e.g., 11-12x P/E), the stock price would see significant upside. The Price-to-Sales ratio tells a similar story: you are buying Onix’s sales for less than 1x revenue (0.88x), while the market pays 4x revenue for KPI.

2. The “Quality” Premium (Why KPI is Expensive) Markets are rarely wrong without a reason. KPI Green commands a premium because it is significantly more efficient.

- The Margin Gap: KPI Green retains ₹18.73 as profit for every ₹100 of sales, whereas Onix retains only ₹11.49.

- The Insight: KPI’s superior margins suggest better cost control, higher pricing power, or a more favorable mix of IPP (Independent Power Producer) vs. EPC (Engineering) revenue. For Onix to command a higher valuation multiple, it needs to bridge this margin gap.

3. The Investment Thesis

Onix Renewable is a deep “Value” play. You are buying a ₹1,000 Cr revenue company at a rock-bottom valuation (0.88x Sales). The bet here is on re-rating: as Onix scales and potentially improves its margins toward the 15-18% range, the market will be forced to re-value it closer to its peers.

KPI Green is a “Quality” play—investors pay up for established scale and superior margins.

Conclusion: Refining the Investment View

Onix Renewable has emerged as a rare high-momentum find in India’s unlisted green energy space, vaulting into the big leagues by crossing the ₹1,000 Crore revenue mark with staggering triple-digit growth. Uniquely, this explosive scale hasn’t come at the cost of efficiency; the company actually expanded its profit margins, signaling robust operational control. This performance creates a compelling valuation arbitrage, as Onix trades at a massive discount to listed peers like KPI Green Energy (less than 1x sales vs. ~4x), offering a deep “value” play for investors betting on a future re-rating. However, this opportunity is balanced by significant “black box” risks: with a tight 92% promoter holding and no visible cash flow data to confirm the quality of its reported profits, Onix remains a high-stakes trade-off between undeniable raw growth and the opacity of its financial governance.

Looking to invest in more high-potential companies like Onix Renewable Limited?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)