In the bustling world of Indian NBFCs, Hinduja Leyland Finance Ltd (HLF) has long been the quiet giant. As a subsidiary of commercial vehicle titan Ashok Leyland, HLF has powered India’s logistics sector for years.

But the FY25 Annual Report reveals that this giant is no longer quiet. With a massive 35% surge in revenue, a fortress-like balance sheet, and an imminent reverse merger with NDL Ventures, HLF is shaping up to be one of the most exciting financial stories of the year.

Is this the perfect time to look at the “financing” engine behind the trucks? Let’s dive into the numbers.

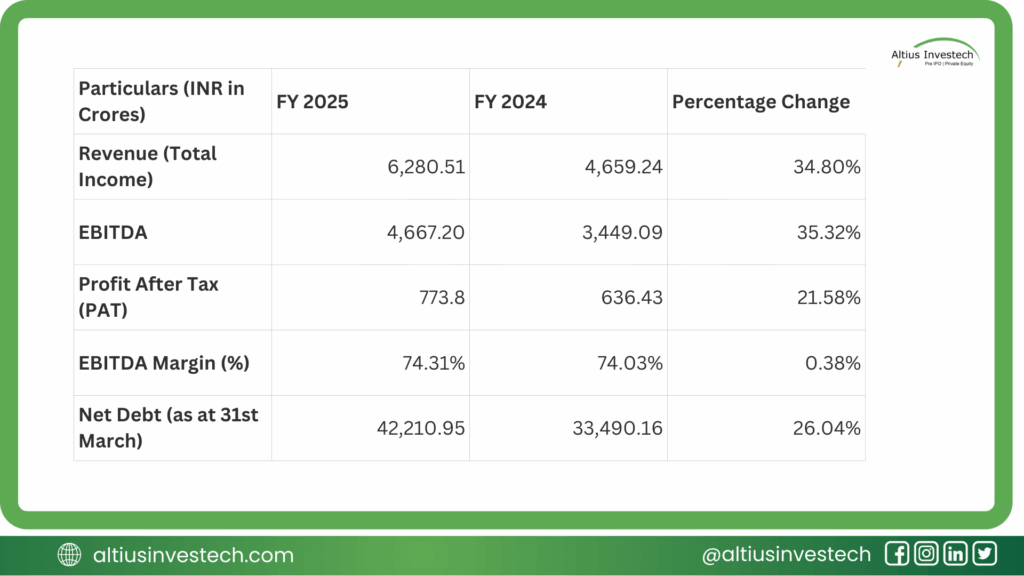

Explosive Growth: Revenue grew 34.8% to ₹6,280 Cr, and EBITDA jumped 35.3%, signaling massive demand for vehicle finance.

The Profit Squeeze: While profits grew 21.6%, rising interest rates (finance costs up 38%) slightly compressed net margins.

Liquidity King: The company is sitting on a massive liquidity buffer with a Liquidity Coverage Ratio (LCR) of 291%—nearly 3x the requirement.

The Big Event: HLF is not going for a traditional IPO. Instead, it is merging with NDL Ventures, offering a unique “backdoor” listing opportunity for savvy investors.

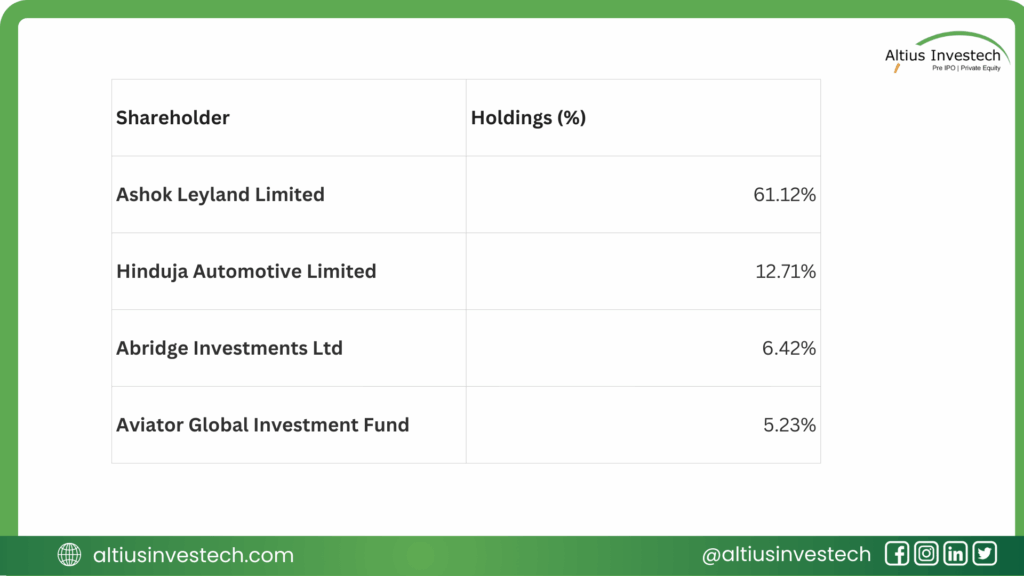

👑 Ownership

HLF isn’t just another lender; it is the captive financing arm of the Hinduja Group. This gives it proprietary access to Ashok Leyland’s ecosystem, a competitive moat that is hard to replicate.

Financial Analysis

📊 The Financial Scorecard

The FY25 numbers tell a story of aggressive expansion supported by operational efficiency.

Financial Insights:

The Good: Operational efficiency is world-class. An EBITDA margin of 74.3% means HLF is incredibly lean in its operations.

The Squeeze: Notice that Finance Costs (+38%) grew faster than Revenue (+35%). This is why Net Profit growth (21%) lagged behind. HLF had to pay higher interest rates on its own borrowings, which slightly compressed the final net margin.

2. The Balance Sheet (The “Fortress”)

This is where HLF truly shines. It has built a massive asset base while keeping risk buffers well above regulatory requirements.

- Assets Under Management (AUM): ₹61,692 Crores (Up 25%). HLF is now a massive player, comparable in scale to many mid-sized banks.

- Net Worth: ₹7,299 Crores (Consolidated). A huge equity base that provides stability.

- Total Borrowings: ₹42,211 Crores. The fuel for its lending engine.

- Capital Adequacy Ratio (CRAR): 19.29% (vs. 15% requirement). This indicates HLF has plenty of room to leverage up and lend more without needing immediate capital infusion.

3. Asset Quality (The Risk Check)

For any lender, the biggest risk is bad loans. HLF’s trend is improving, signaling disciplined underwriting.

- Gross NPA (Stage 3 Assets): Improved to 3.63% (down from 4.27% in FY24).

- Net NPA: Improved to 2.10% (down from 2.70% in FY24).

Verdict: HLF is firing on all cylinders. It is capturing market share (Revenue up 35%), improving asset quality (NPA down), and maintaining high operational efficiency (74% EBITDA margins). The only headwind is the rising cost of funds, which is a sector-wide phenomenon, not an HLF-specific issue.

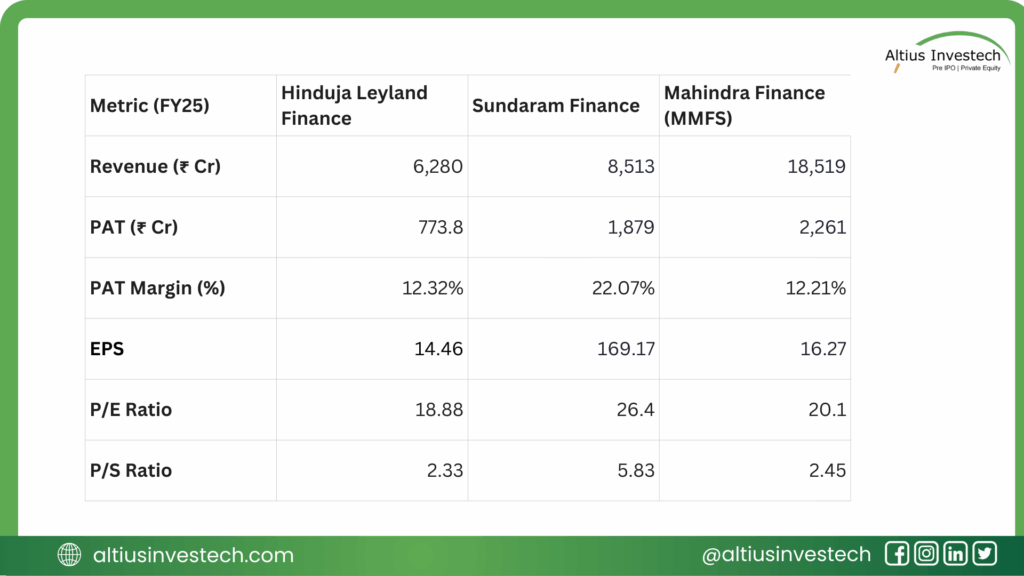

⚔️ Peer Analysis: The Valuation Showdown

To see where Hinduja Leyland Finance (HLF) stands in the market, we’ve stacked it against two listed giants in the vehicle finance space: the gold-standard Sundaram Finance and the massive Mahindra Finance (MMFS).

Why HLF Looks Attractive?

1. The Profitability Match-Up: While Sundaram Finance is in a league of its own with a 22% Net Profit Margin, HLF is holding its ground against Mahindra Finance.

- HLF’s Margin (12.32%) is actually slightly higher than Mahindra Finance’s (12.21%). This proves that despite being smaller, HLF is operating with competitive efficiency.

2. The Valuation Discount: Here is the kicker. Despite having better margins than Mahindra Finance, the market is pricing HLF at a discount.

- Price-to-Earnings (P/E): HLF trades at 18.88x earnings, making it cheaper than both Mahindra (20.1x) and the premium-valued Sundaram (26.4x).

- Price-to-Sales (P/S): At 2.33x sales, HLF is the most affordable entry point in this peer group.

Investors are currently paying a premium for Sundaram’s efficiency and Mahindra’s scale. HLF is the “Value Pick” of the trio. It offers margins comparable to Mahindra but at a cheaper valuation. If HLF can continue its growth trajectory and close the gap with Sundaram’s efficiency, the stock has significant room to re-rate upwards post-listing.

Fair Value Analysis: The “Merger Math” You Can’t Ignore:

The HLF-NDL merger creates a unique arbitrage window. Here is the valuation logic in a nutshell:

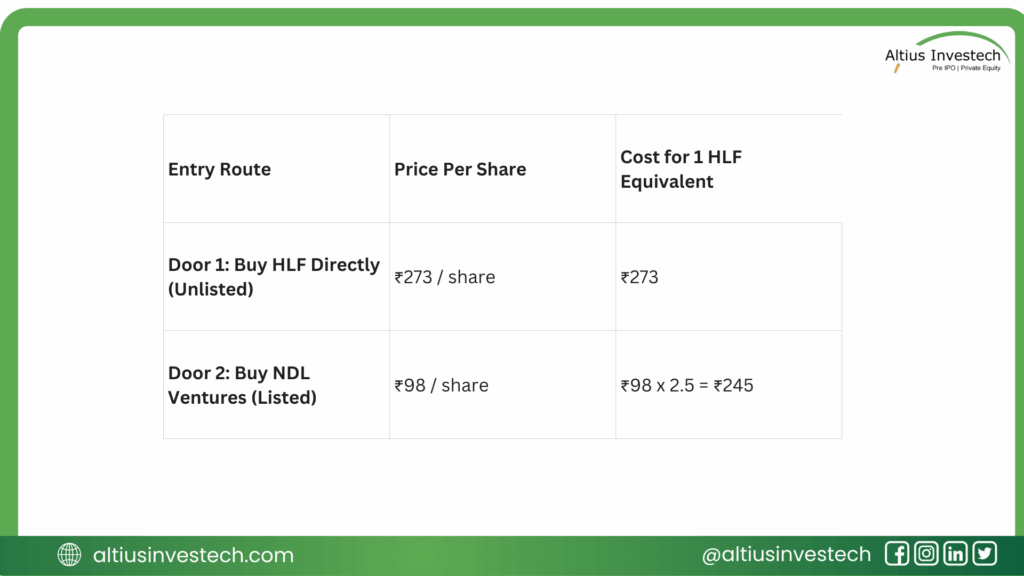

1. The Core Equation: The share swap ratio is fixed at 25:10 (25 NDL shares for every 10 HLF shares).

- Effective Ratio: 1 Share of HLF = 2.5 Shares of NDL.

2. The Arbitrage Opportunity (The Disconnect):

- Implied Fair Value: With NDL trading at ₹98, the implied value of one HLF share is ₹245 (2.5 × ₹98).

- Market Reality: In the unlisted market, HLF shares are trading at a premium of ₹273.

- The Trade: Buying NDL Ventures today effectively gets you HLF shares at a 7-8% discount compared to the grey market price.

3. Why the Discount? This 8% gap is essentially the “waiting fee” for the 18-month timeline (Appointed Date: April 1, 2026) and the regulatory risks (NCLT/SEBI approvals) involved.

4. The Reality Check: The market pegs value to HLF because it is the powerhouse. Compared to NDL’s standalone operations, HLF has ~9x higher Book Value, superior profitability (ROE ~9% vs <1%), and a massive ₹14,500 Cr market cap (vs NDL’s ~₹330 Cr). NDL is simply the vessel.

🎯 Conclusion: The Bull Case

Hinduja Leyland Finance is a “Growth with Safety” play.

- The Engine: It is riding the cyclical upswing in the Indian auto sector.

- The Shield: It has an LCR of 291% and strong parcentage, ensuring it never runs out of fuel (cash).

- The Kicker: The merger with NDL Ventures provides a clear path to listing, offering liquidity and potentially unlocking value for early entrants.

Risk to Watch: The auditor noted a minor deficiency in the “Audit Trail” feature in one of its JV’s software. While not a financial material issue, governance in tech systems is a key area for public market investors.

Final Take: HLF is no longer just a lending arm; it is a full-fledged financial powerhouse. For investors looking for exposure to the commercial vehicle cycle without buying auto stocks directly, HLF (via NDL Ventures) might just be the smartest ride in town.

Looking to invest in more high-potential companies like Hinduja Leyland Finance Ltd (HLF)?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)