If you’ve recently inherited a house or plot of land and are thinking of selling it, a crucial ruling by the Income Tax Appellate Tribunal (ITAT) could significantly reduce your tax bill — and it’s one that many heirs unknowingly miss out on.

The ITAT has reaffirmed a principle that is as favourable as it is often overlooked: when computing Long-Term Capital Gains (LTCG) on the sale of an inherited property, the benefit of indexation must be calculated starting from the year in which the original (previous) owner first purchased or held the property — not the year in which you, the heir, inherited it.

THE CORE RULING

Adil Noshirvan Shethna vs. ITO (I.T.A. No. 898/SRT/2024, January 23, 2026): The ITAT bench held that the appellant had correctly applied the Cost Inflation Index (CII) starting from FY 1985–86 — the year the original owner first held the property — rather than the year the heir received it through a will. The Assessing Officer’s addition was struck down.

First, Let’s Understand the Basics

When you sell a property that you’ve held for more than 24 months, the profit is classified as a Long-Term Capital Gain (LTCG). To make the tax calculation fair, the Income Tax Act allows you to “index” your cost of acquisition — that is, adjust the original purchase price upward to account for inflation over the years. The higher your indexed cost, the lower your taxable gain.

The indexation is done using the Cost Inflation Index (CII), a number notified annually by the government. The key question for inherited property has always been: which year’s CII do you use at the denominator? The year the original owner bought it, or the year you inherited it?

THE FORMULA

Indexed Cost of Acquisition = Original Purchase Price × (CII of Year of Sale ÷ CII of Year of First Holding)

What the ITAT Has Clarified

The answer, as consistently held by courts and tribunals, is the year the previous owner first held the asset.

CASE IN FOCUS

The Shethna Case (Surat ITAT, 2026): The assessee sold a property inherited through a will. His share of the sale amounted to ₹22,79,776, while the stamp valuation authority pegged it at ₹68,38,000. The Assessing Officer applied the CII from a more recent year, making an addition of ₹2,16,465 to the capital gains. The ITAT, comprising Dr. B.R.R. Kumar (Vice President) and Suchitra Kamble (Judicial Member), allowed the appeal — holding that indexation must rightfully begin from FY 1985–86, the year the original owner first held the property.

This ruling is grounded in Section 2(42A) of the Income Tax Act, which defines the “period of holding.” It explicitly provides that when an asset is received through a gift or will, the period for which the previous owner held it shall be included in the heir’s holding period. The Gujarat High Court ruled that the indexed cost of acquisition must be computed from the year the previous owner first held the asset. The Mumbai ITAT similarly upheld this in a case involving a US-resident heir who sold property in Colaba, Mumbai, granting indexation from FY 1981–82 (the earliest permissible base year), backed by the Bombay High Court’s ruling in CIT vs. Manjula J. Shah and CBDT Circular No. 636.

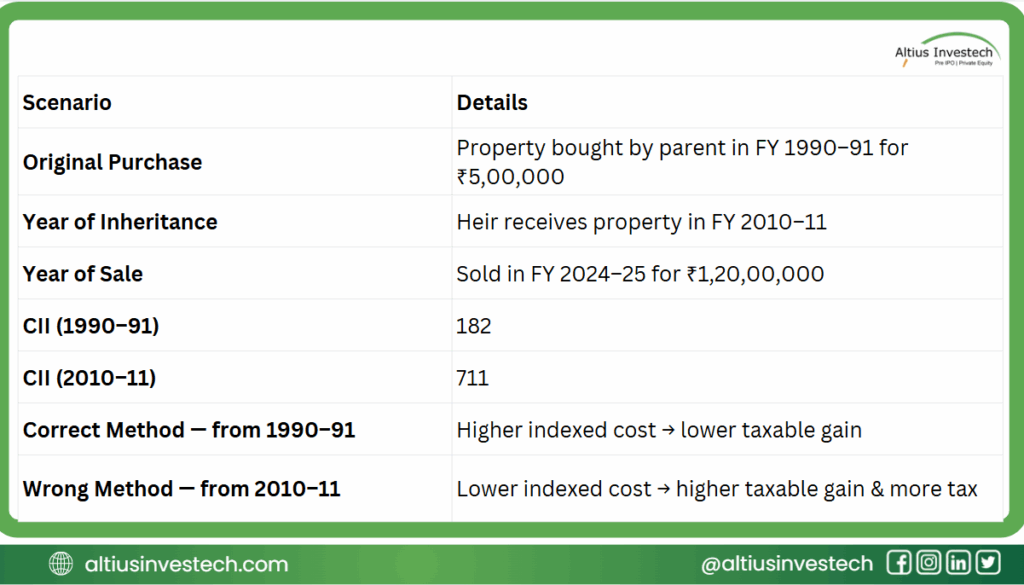

Why This Matters: The Numbers Tell the Story

The difference in tax liability can be enormous. Consider a simple illustration:

The longer the original owner held the property before you inherited it, the greater your indexation benefit — and the more tax you save. Using the wrong year for indexation can easily cost you lakhs in unnecessary taxes.

The Budget 2024 Twist You Must Know

While the ITAT ruling is a relief, it comes with an important context: the Union Budget 2024 made sweeping changes to LTCG taxation on property. Effective July 23, 2024, the LTCG tax rate on real estate was reduced from 20% with indexation to 12.5% without indexation.

However, following significant public pushback, the government introduced a relief provision for properties acquired before July 23, 2024. Sellers of such properties can choose between two options:

| Option | Tax Rate | Indexation Benefit |

| Option A | 20% LTCG | Yes — indexation available |

| Option B | 12.5% LTCG | No — flat rate without indexation |

For inherited properties with a long lineage — where the original owner purchased the asset decades ago — Option A (20% with indexation) will often work out more favourably, because the indexed cost can be traced all the way back, dramatically reducing the taxable gain.

What About Properties Acquired Before April 1, 2001?

If the original owner purchased the property before April 1, 2001 (the current base year for CII), taxpayers may use the Fair Market Value (FMV) as on April 1, 2001 as the cost of acquisition — if it is higher than the actual original purchase price. Indexation then applies from FY 2001–02 (CII = 100) onwards. This ensures that even very old properties — those bought in the 1970s or 1980s — are not taxed on fictitious gains that are merely a product of inflation over half a century.

A Note on Partial Inheritance

Not all inherited shares are equal under the law. If you inherited only a portion of a property while purchasing the rest from co-heirs through a release deed, the indexation rules differ for each portion:

IMPORTANT NUANCE

The Chennai ITAT, in R. Mohan vs. ITO, held that indexation from the original owner’s year applies only to the inherited share. For shares acquired through a release deed (i.e., purchased from co-heirs), indexation runs only from the date of the release deed.

Key Takeaways for Property Heirs

What You Should Remember

✓ When selling inherited property, always trace indexation back to the year the original owner first held the asset — not the year you received it.

✓ This principle is backed by multiple ITAT rulings, Gujarat HC, Bombay HC (Manjula J. Shah), and CBDT circulars.

✓ For properties acquired before April 1, 2001, use the FMV as on that date as your cost base, with CII applied from 2001–02.

✓ Under Budget 2024 rules, compare both options — 20% with indexation vs. 12.5% without — to determine what saves you more tax.

✓ If you inherited only part of a property, apply different indexation start dates for each portion.

✓ Always consult a qualified CA or tax advisor to accurately compute capital gains on inherited property.

The Bottom Line

Selling an inherited property is already an emotionally complex decision. The tax computation should not add unnecessary burden on top of that. The ITAT’s reaffirmation of the indexation rule is a reminder that the law, when correctly applied, is on the side of the taxpayer.

If you — or a family member — are in the process of selling inherited real estate, make sure your tax consultant is computing the indexed cost from the correct year. The difference between the right and wrong starting point can translate into a substantially lower tax outgo, sometimes by several lakhs of rupees.

When in doubt, cite the precedents: CIT vs. Manjula J. Shah (Bombay HC), the Gujarat High Court ruling on inherited property indexation, and the most recent ITAT order in Adil Noshirvan Shethna vs. ITO (2026). These form a clear, consistent line of legal authority you can rely on.