If you have ever tried to add a nominee to your demat account or mutual fund folio and found yourself stuck in a maze of OTP verifications and video confirmations, you are not alone. The Securities and Exchange Board of India (SEBI) has heard those frustrations — and is now proposing a significant overhaul of how nomination works for investors across the country.

On Tuesday, SEBI put forward a set of changes to the nomination framework that was originally introduced in January 2025. The proposals, which apply to both demat accounts and mutual fund folios, are designed to reduce friction, improve compliance, and make the process more accessible to the average investor.

Why SEBI Is Revisiting the January 2025 Framework

When SEBI rolled out its updated nomination guidelines in January 2025, the intent was clear: encourage more investors to formally designate nominees so that their assets could be transferred smoothly to their families in the event of their death, without lengthy legal battles or unclaimed asset situations.

However, implementation did not go as planned. Industry participants — including brokers, depository participants, and asset management companies — flagged significant operational challenges in putting certain provisions into practice. The process that investors were required to follow to opt out of nomination involved OTP-based verification followed by a video-based confirmation. Market participants widely called this cumbersome, and adoption rates reflected that dissatisfaction.

SEBI has now responded by proposing a revised framework that retains the spirit of the original guidelines while substantially simplifying the mechanics.

The Central Proposal: Nomination as the Default

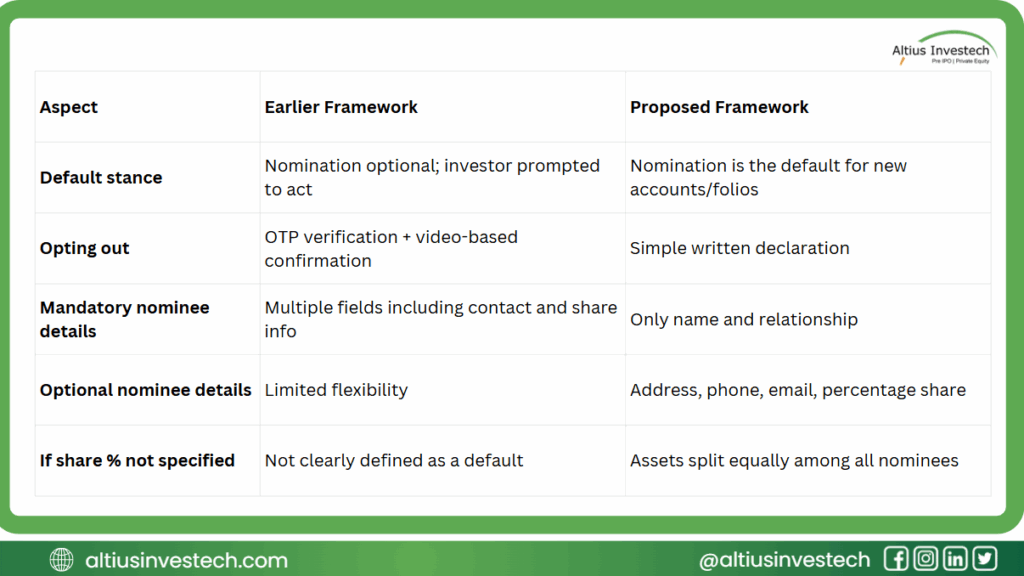

The most consequential change being proposed is structural: nomination would become the default option for investors opening new demat accounts or mutual fund folios.

Under the current system, investors are prompted to nominate but can opt out through a multi-step verification process. Under the proposed framework, the burden shifts. Investors who do not wish to nominate anyone would need to explicitly opt out — and they would do so by providing a simple declaration to that effect.

This is a meaningful philosophical shift. By making nomination the starting assumption rather than a step investors must actively take, SEBI is betting that inertia — which has long worked against nomination — will now work in its favour. Most investors who do not feel strongly either way will end up with a nominee on record, which protects their families and reduces the volume of unclaimed assets in the financial system.

Out with OTPs and Videos, In with Declarations

The previous opt-out mechanism required investors to verify their identity through OTP and then complete a video-based confirmation. While the intent was to ensure informed consent, the execution created unnecessary barriers — particularly for older investors or those in areas with unreliable internet connectivity.

SEBI’s proposed replacement is far simpler: a written declaration. Investors who genuinely do not wish to nominate anyone would sign off on a declaration, providing explicit consent to opt out. This is easier to execute, easier to process for intermediaries, and easier to audit — a practical win on multiple fronts.

Simplified Information Requirements for Nominees

Beyond the opt-out process, SEBI is also proposing to streamline the information investors must provide when they do nominate someone. Currently, the nomination form asks for a fairly detailed set of data points, which can slow down the process and sometimes lead investors to abandon it midway.

Under the proposed framework, only two pieces of information would be mandatory:

- The nominee’s name

- The nominee’s relationship with the investor

All other details — including address, mobile number, email ID, and the percentage share of the estate to be allocated to that nominee — would be optional.

This is a pragmatic calibration. The mandatory fields ensure that the nominee can be identified and contacted when the time comes. The optional fields provide richer information but are not gatekeepers that block the process entirely.

What Happens If You Have Multiple Nominees?

Many investors choose to split their assets among more than one nominee — a spouse and children, for instance, or siblings. A common point of confusion in such cases is what percentage of the assets goes to whom.

SEBI’s proposal addresses this directly. If an investor does not specify the percentage share assigned to each nominee, the assets would simply be divided equally among all nominees listed. This default equal-split rule removes an unnecessary point of complexity and ensures that the absence of a specific instruction does not create ambiguity or disputes later.

Old vs. New: A Quick Comparison

Why This Matters for Ordinary Investors

India has a persistent problem with unclaimed financial assets. Billions of rupees sit in dormant accounts, lapsed insurance policies, and untraced mutual fund investments because there is no nominee on record — or the nominee does not know they were named. Families are forced into lengthy legal processes involving succession certificates, court orders, and protracted paperwork simply to access money that their loved ones legitimately saved for them.

Nomination does not eliminate all of these hurdles, but it dramatically reduces them. A named nominee can approach the financial institution directly and, in most cases, receive the assets far more quickly than through a legal inheritance process. The smoother and more intuitive SEBI makes the nomination process, the higher the chances that investors will actually complete it — and the fewer families will be left scrambling in the aftermath of a loss.

For young investors opening their first demat account or starting a SIP in a mutual fund, these changes lower the bar significantly. There is no longer a complicated process to navigate. The default does the heavy lifting, and personalisation — who gets what percentage, how to reach them — can be layered in optionally at the investor’s convenience.

What Should You Do Right Now?

These are proposals at this stage — SEBI has not yet finalised or implemented the new rules. However, the direction of travel is clear, and it is a good moment for every investor to take stock of their own nomination status.

Log into your demat account or check with your broker whether you have an active nominee on record. Do the same for each of your mutual fund folios — nomination is folio-specific, not account-level, so you may need to update several records. If you have multiple nominees, consider whether the equal-split default suits your intentions or whether you want to specify shares explicitly.

SEBI’s proposals, if implemented, will make it easier for future investors to get this right from day one. For those of us already in the system, the responsibility remains ours to ensure our nominations are current, accurate, and reflective of our wishes.

The regulator is removing the excuses. The rest is up to us.

Source: Securities and Exchange Board of India (SEBI) proposal on nomination framework simplification, reported March 2026.