it’s rare to see a financial turnaround this clean and dramatic in a single year. ESDS Software’s FY2025 report isn’t just an update; it’s a “before and after” story. The company has fundamentally reset its financial health, transforming from a leveraged, growing firm into a debt-free, high-growth, cash-generating machine.

While the 309% explosion in net profit is the headline, the real story is the 98.6% wipeout of its net debt. ESDS has aggressively de-risked its balance sheet, all while stepping on the gas with an “AI-first” global expansion. But is it all as perfect as it looks? Let’s dive in.

Profit Explosion: Net Profit (PAT) skyrocketed 309% to ₹55.61 Cr.

Massive Margin Expansion: EBITDA margins jumped from 26.5% to an impressive 40.1%, showing strong operational efficiency.

The “Great Deleveraging”: Net Debt has been virtually eliminated, plunging 98.6% from ₹146.8 Cr to just ₹2.03 Cr.

Global Growth Engine: The growth was fueled by a nearly 600% surge in international revenue.

The Big Red Flag: This growth came with a new, significant risk: a single customer, Gazprom Bank, now accounts for 20.36% of all revenue.

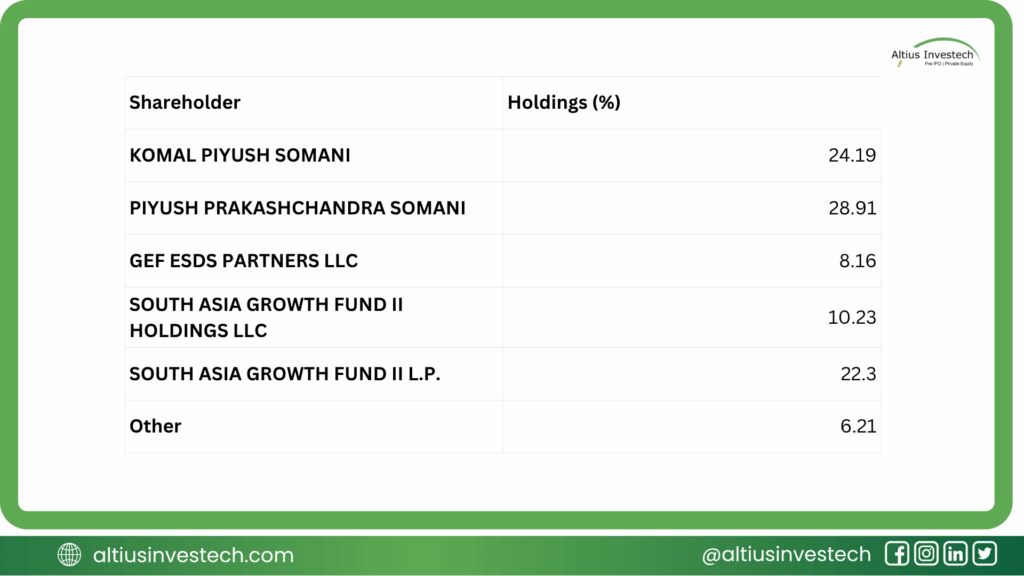

👑 Who Owns ESDS? A Mix of Founders and Finance

The ownership structure is a classic PE-backed promoter setup. The founding Somani family holds a controlling majority, ensuring their vision leads the company. This is backed by a significant stake from institutional investors, including private equity, which has helped fund its aggressive growth and recent de-leveraging.

Financial Analysis

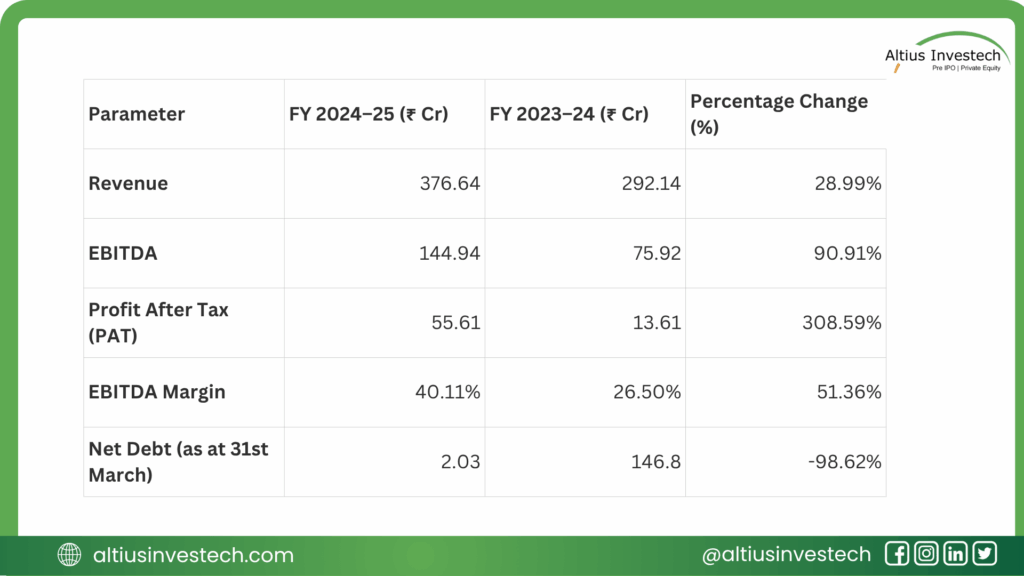

📈 The Financials: A “Before and After” Story

The FY25 numbers tell a story of a complete financial transformation.

Financial Insights:

The 309% PAT Surge: This isn’t a one-off accounting trick. It was driven by two powerful factors:

High-Growth Top Line: Revenue grew by a strong 29%, powered by a nearly 600% explosion in international sales.

Massive Margin Expansion: EBITDA margins leaped from 26.5% to 40.1%. This means the company is keeping far more of every rupee it earns, proving its operational efficiency and “AI-first” model are highly profitable.

The 98.6% Debt Crash: This was a deliberate strategic masterstroke. ESDS raised over ₹1,400 million (₹140 Cr) in two preferential placements and used that cash to redeem its high-interest NCDs. By wiping out its debt, it has slashed its interest payments, which helped its Net Profit grow even faster than its operating profit.

The company’s profits are also backed by strong cash flow, with an excellent EBITDA-to-CFO conversion rate of 78.25%. This confirms the earnings are real.

⚠️ Red Flags: Yellow Cards on the Field?

The new ESDS looks fantastic, but two significant risks have emerged:

- Customer Concentration: The 600% international growth is impressive, but it’s largely driven by one new customer: Gazprom Bank, which now accounts for over 20% of all revenue. Any issue with this single contract would be a massive blow to the top line.

- The ESOP Lawsuit: A ₹184.80 million (₹18.5 Cr) claim from an ex-employee regarding ESOPs is pending in the Bombay High Court. While the company is disputing it, this remains a significant contingent liability that could impact future profits if the ruling is unfavorable.

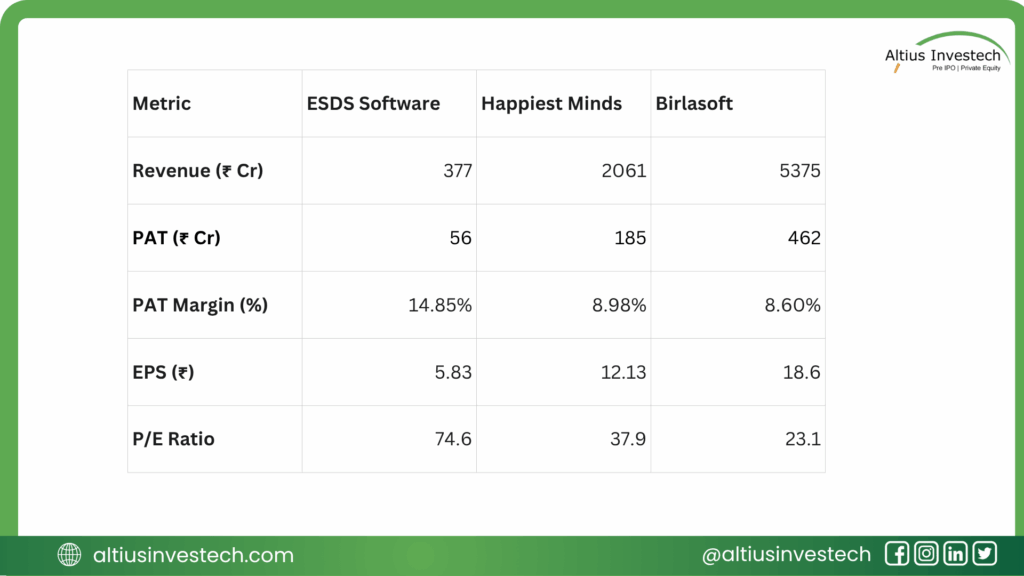

📊 Peer Analysis: How Does ESDS Stack Up?

This comparison reveals a fascinating story of a small, highly efficient player with a “growth stock” valuation.

- The Scale Difference: ESDS is currently a niche player, significantly smaller than its large-cap peers in terms of both revenue and absolute profit.

- The Profitability King: This is the most critical insight. ESDS’s PAT Margin of 14.85% is exceptional. It is significantly more profitable than both Happiest Minds (8.98%) and Birlasoft (8.60%), proving its “AI-first” model is highly efficient at converting every rupee of sales into net profit.

- The Premium Valuation: The market has clearly recognized this superior profitability and growth. ESDS trades at a very high P/E ratio of 74.6. This is nearly double the multiple of Happiest Minds (37.9) and more than triple that of Birlasoft (23.1).

The market is pricing ESDS at a massive premium. This isn’t a “value” stock; it’s a “growth” stock. Investors are paying a high price relative to its current earnings, betting that its superior profitability and explosive 309% PAT growth will continue, allowing it to grow into this rich valuation.

Conclusion: Refining the Investment View

ESDS has successfully executed a brilliant financial reset. It has swapped a high-debt, moderate-growth profile for a debt-free, high-growth, high-margin one. The business is gushing cash, and its “AI-first” focus and global expansion are paying off.

The investment thesis is a bet on this new trajectory. The company has transformed itself. However, investors are paying a premium valuation for this growth, and that bet is not without risk. The two key watch items are clear: diversifying away from the new key customer and resolving the pending high-value lawsuit.

Looking to invest in more high-potential companies like ESDS ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)