The Indian IPO market is buzzing, and the latest name to join the fray is Fractal Analytics, a pure-play enterprise AI company. With “AI” being the hottest buzzword on the planet, investors are understandably excited. But a deep dive into its financial reports reveals a complex picture: a high-growth, high-potential business with a rock-solid balance sheet, but also one with messy reported profits, serious governance red flags, and extreme client concentration.

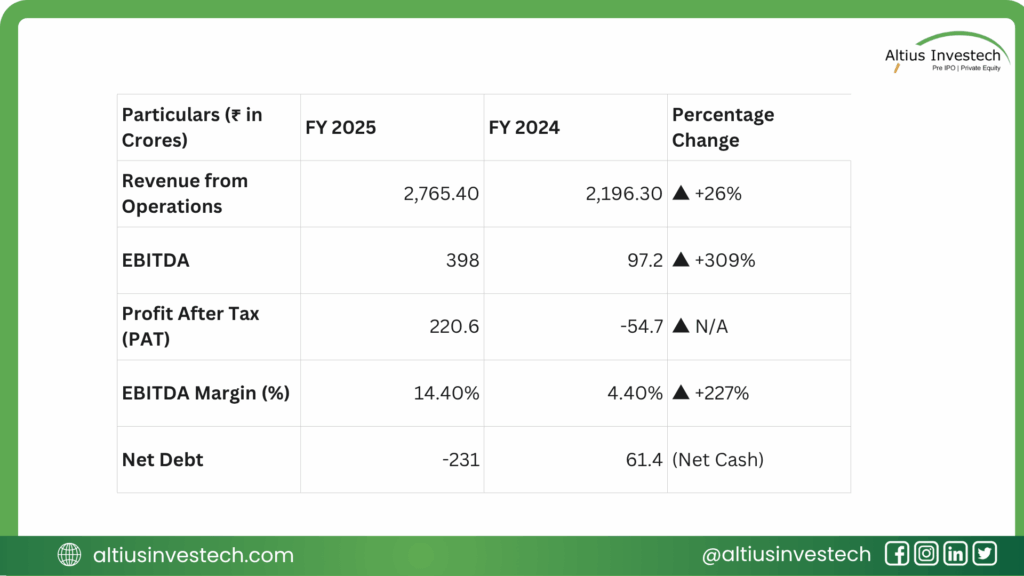

Massive Profit Rebound: After a shock net loss of ₹55 Crores in FY24, the company posted a strong profit of ₹221 Crores in FY25.

Explosive Growth: Revenue grew by a rapid 26% in FY25, outpacing the global market.

Fortress Balance Sheet: The company has negative net debt, meaning its cash and liquid investments are greater than its total borrowings.

The Big Risk (Concentration): Over 54% of its revenue comes from its top 10 clients. Losing just one could be a disaster.

Serious Governance Red Flags: Auditors flagged critical issues, including the failure to maintain a proper audit trail (edit log) and not storing data backups on servers in India as required by law.

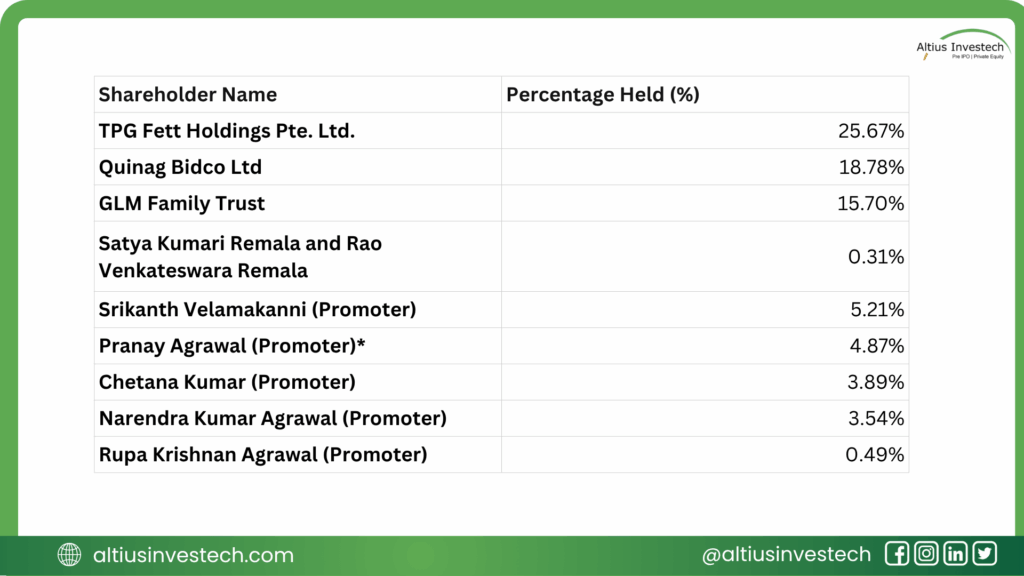

Ownership Structure:

🚀 What’s the Fractal Engine?

In simple terms, Fractal is a “pure-play enterprise AI” company. It doesn’t just sell software; it sells its brainpower to help the world’s biggest companies make better decisions using AI.

It operates in two segments:

Fractal Alpha: The new, high-growth bet. This segment builds its own pre-built AI products (like Samya.AI) that can be sold to many customers with less customization.

Fractal.ai: The core business. This involves custom-built AI solutions and consulting for large enterprises.

🛡️ What is Fractal’s Competitive Moat?

Fractal’s main advantage is its deep, specialized expertise. In a market where talent is scarce, its ability to attract and retain top data scientists, engineers, and designers is its primary moat.

The proof is in its client relationships. In FY25, its Net Revenue Retention (NRR) was 121.3%. This is a fantastic metric. It means that even if Fractal didn’t sign a single new client, its revenue from existing clients still grew by 21.3%. This shows deep integration and high client satisfaction.

Financial Analysis

At first glance, Fractal’s financials look wildly volatile. But when you separate the “paper” accounting from the “real” business, a much clearer picture emerges.

Insights:

Why the FY24 Loss? The big loss in FY24 wasn’t from a business failure. It was driven by massive one-off and non-cash expenses, primarily related to employee stock options (ESOPs) and acquisition-related bonuses.

The Real Profitability: The management’s “Adjusted EBITDA Margin” (which removes these one-off items) shows a consistent and strong improvement (from 6.8% in FY23 to 17.4% in FY25). This suggests the underlying core business is healthy and getting more efficient.

The Profit is Real (Excellent Cash Flow): The best news is in the cash flow statement. In FY25, Fractal’s EBITDA-to-Cash-Conversion was 99.75%. This means nearly every single rupee of its operating profit was converted into actual cash. This is a sign of very high-quality earnings.

The Fortress Balance Sheet: The company ended FY25 with Net Cash of ₹231 Crores. It has more cash than debt, giving it a powerful buffer and the capital to invest in growth.

⚠️ Red Flags: The Bear Case

Despite the strong underlying metrics, there are serious risks to consider.

- Extreme Client Concentration: With 54% of revenue from its top 10 clients and 65% from the USA, the company is dangerously exposed. A recession in the US or the loss of one or two key accounts would be catastrophic.

- Serious Governance Lapses: This is the most concerning part. The company’s auditors noted that:

- The accounting software lacked a proper audit trail (edit log) for the full year.

- The company and eight of its subsidiaries failed to keep data backups on servers physically located in India, a direct violation of regulatory requirements. These are not minor issues. They point to immature internal controls and a failure to meet basic compliance standards for a public company.

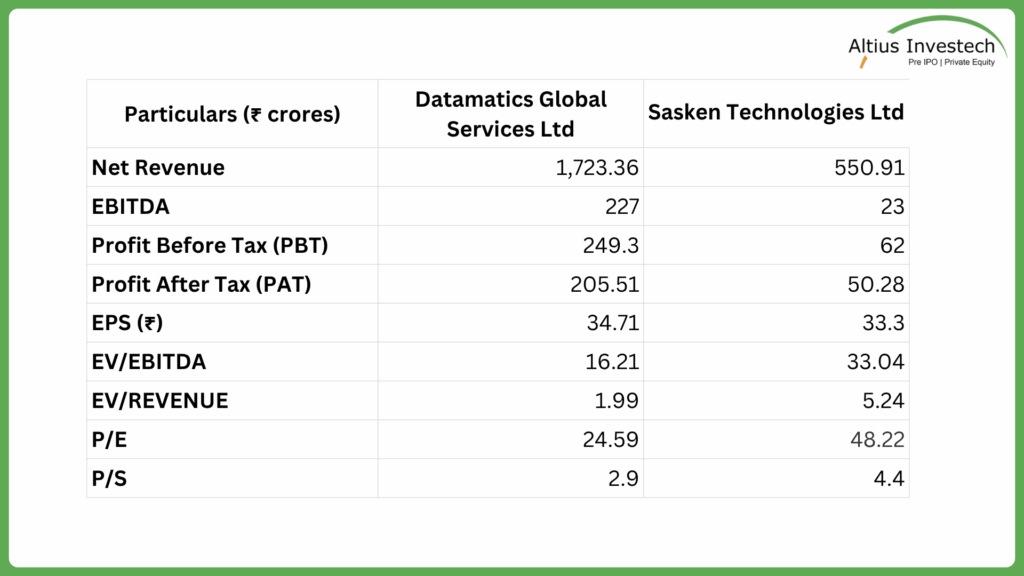

Peer Analysis

To get a relative idea, we can look at other tech consulting and engineering firms, though these are imperfect comparisons.

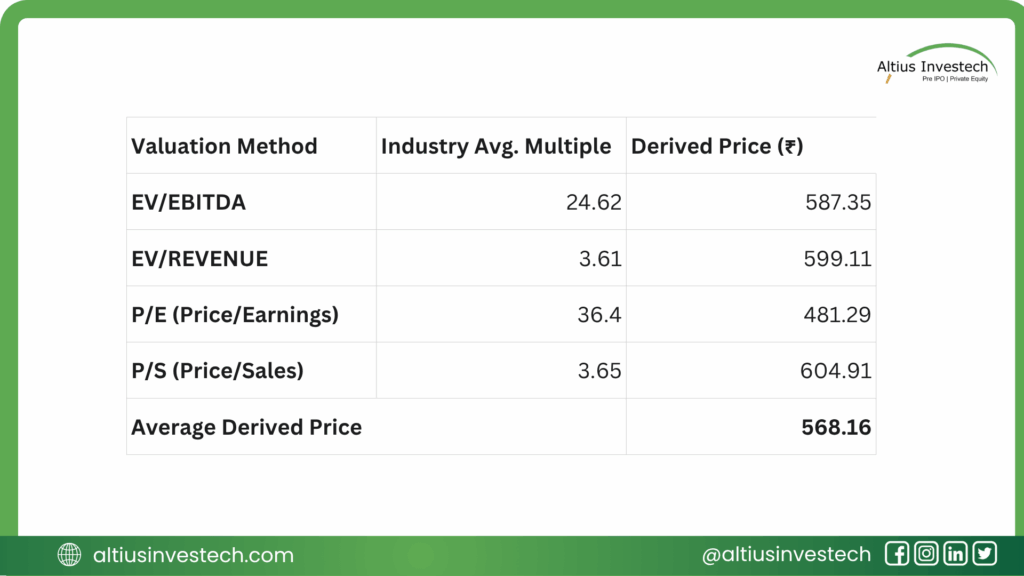

Price Analysis

This is purely illustrative and not a price target. By taking the average valuation multiples from a basket of “similar” (though imperfect) IT and tech services companies, we can derive a potential price

This analysis suggests a potential valuation of around ₹568 per share. However, the market could argue for a higher price (a “premium”) due to Fractal’s pure-play AI focus, or a lower price (a “discount”) due to its governance red flags and high concentration risk.

Conclusion: Refining the Investment View

Financially Robust Core: Fractal is not a cash-burning startup. Its underlying business is highly profitable (17.4% Adjusted EBITDA Margin) and has an excellent 99.75% cash conversion rate. Its balance sheet is a fortress.

A “Governance Discount” is Warranted: The audit trail and data backup failures are serious. These are not mistakes a public-market-ready company should be making. Combined with the extreme client concentration risk, investors must apply a significant risk discount to their valuation.

Valuation Hinges on the AI Narrative: The IPO’s success will depend on convincing investors to look past the messy GAAP numbers and serious governance/concentration risks, and instead pay a premium for a “pure-play AI” leader in a structurally booming market.

Concluding Perspective: The Fractal IPO is a classic high-risk, high-reward proposition. It offers a rare chance to invest directly in the enterprise AI revolution. This opportunity is suitable for investors with a high-risk appetite who believe in the long-term AI story and are willing to bet that management will fix its governance gaps and diversify its client base after going public.

Looking to invest in more high-potential companies like Fractal Analytics ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)