Mohan Meakin Limited announced its unaudited financial results for the quarter and nine months ended December 31, 2025.The performance reflects steady operational momentum across both alcoholic and non-alcoholic segments, supported by revenue growth and improved profitability on a year-on-year basis.

Company Overview – Mohan Meakin Limited

Mohan Meakin Limited was established in 1855 and is one of the oldest alcoholic beverage companies in India. It is a public limited company, listed on the Calcutta Stock Exchange, with its registered office at Solan Brewery, Himachal Pradesh. The company operates with a single-entity structure and has 0 subsidiaries or joint ventures, resulting in a simple and asset-focused corporate setup.

Key aspects of the business include:

- Operations across 2 major segments: alcoholic beverages and non-alcoholic/food products

- Alcoholic portfolio spanning 1 beer segment + 5 IMFS categories

- Presence in multiple manufacturing locations across India

- Non-alcoholic portfolio covering 4 product lines: juices, cereals, porridge, and vinegar

The company’s long operating history and diversified product base support stable brand recall and continuity across generations of consumers.

Business Model – Core Elements

Mohan Meakin follows a manufacturing-led and brand-centric model, with production anchored in owned breweries and distilleries. Sales are primarily domestic and structured around state-wise excise and distribution systems, requiring localized pricing and channel strategies across India.

The business model is characterized by:

- In-house manufacturing to maintain quality control and cost efficiency

- State-level distribution aligned with individual excise frameworks

- Contract bottling arrangements in select states to enable local supply

- Brand licensing and royalty income from third-party bottlers

- Focus on asset utilization and operating efficiency over aggressive expansion

Overall, the company prioritizes steady volumes, geographic reach through partnerships, and disciplined capital use, rather than rapid capacity build-outs.

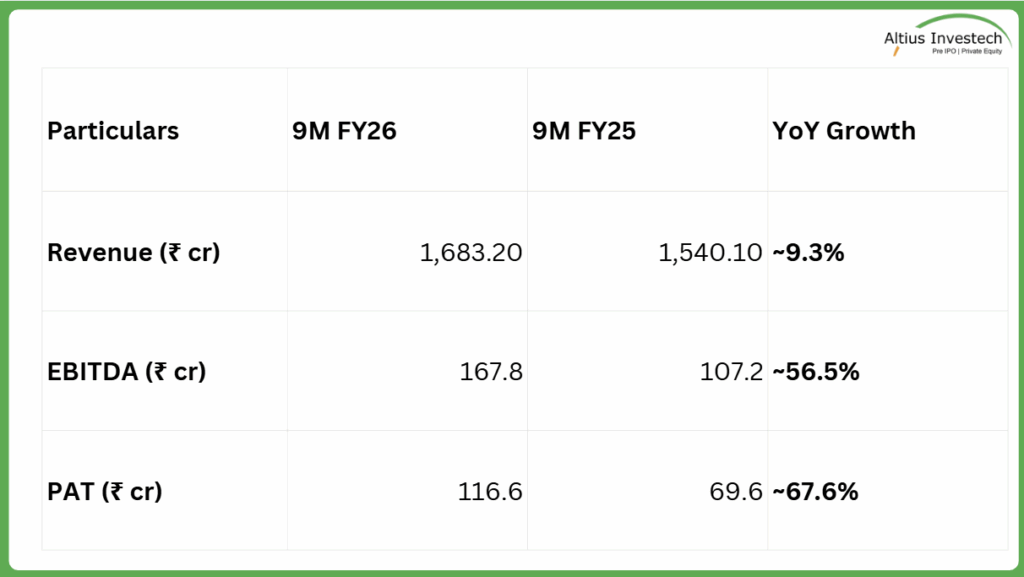

Financial Snapshot

Insights

1. Superior Segmental Profitability (Alcoholic)

The primary engine for the profit jump was the Alcoholic segment. While its revenue grew by 9.4% (from 1,528.07 Cr to 1,671.63 Cr), its segment result (profit) skyrocketed by 56.4%, rising from 107.27 Cr to 167.76 Cr. This indicates that the core business became significantly more profitable, likely due to a better product mix or lower input costs relative to sales.

2. Drastic Shift in Expense Structure

There was a massive structural shift in how the company recorded costs, which ultimately benefited the margins:

• Excise Duty: Dropped by 300.53 Cr (from 401.95 Cr to 101.42 Cr).

• Purchases of Stock-in-Trade: Rose by 332.41 Cr (from 759.74 Cr to 1,092.15 Cr).

• Analysis: When you combine these two items, the total “cost of goods/tax” rose by only 31.88 Cr, despite the company generating 143.12 Cr more in revenue. This efficiency allowed the PBT margin to expand from 6.07% to 9.28% over the nine-month period.

3. Boost from Other Income and Exceptional Items

• Other Income: Added 23.01 Cr to the top line compared to 9.08 Cr the previous year, a gain of 13.93 Cr that carries no operational cost.

• Exceptional Gain: The 9M FY26 figures were further bolstered by a net exceptional gain of 1.71 Cr,. This consisted of a 2.10 Cr gain from the sale of land at Kalka, partially offset by a 0.39 Cr charge for employee benefit past service costs related to new Labor Codes.

4. Managed Operational Costs

Despite the growth in scale, several operating expenses remained well-controlled:

• Finance Costs: Actually decreased from 0.63 Cr to 0.57 Cr.

• Depreciation: Remained stable, increasing only slightly from 7.38 Cr to 7.80 Cr.

• Employee Benefits: Rose by 7.07 Cr (from 38.42 Cr to 45.49 Cr), reflecting a standard increase given the growth in operations.

Summary: The 67.7% jump in PAT was not just due to sales growth; it was the result of the Alcoholic segment becoming vastly more profitable (+60.49 Cr in segment results), a significant boost in Other Income (+13.93 Cr), and a net exceptional gain from a land sale

Valuation

Current Metrics based on FY25 Data

- P/E: 19.1x

- P/B: 4.16x

- P/S: 0.91x

The company has seen a sharp step-up in profitability, with earnings accelerating beyond FY25 levels and sustaining momentum into FY26. This improvement is reflected in both trailing and run-rate profit numbers.

Earnings reference points

- FY25 PAT: ₹102.63 crore → P/E: 19.1x

- TTM PAT: ₹149.71 crore → P/E: ~13.1x

- 9MFY26 PAT: ₹116.6 crore

- Annualised FY26E PAT: ~₹155–156 crore → P/E: ~12.6x

At current prices, the valuation compresses meaningfully on updated earnings, placing the stock in the low-teens P/E range on run-rate profits

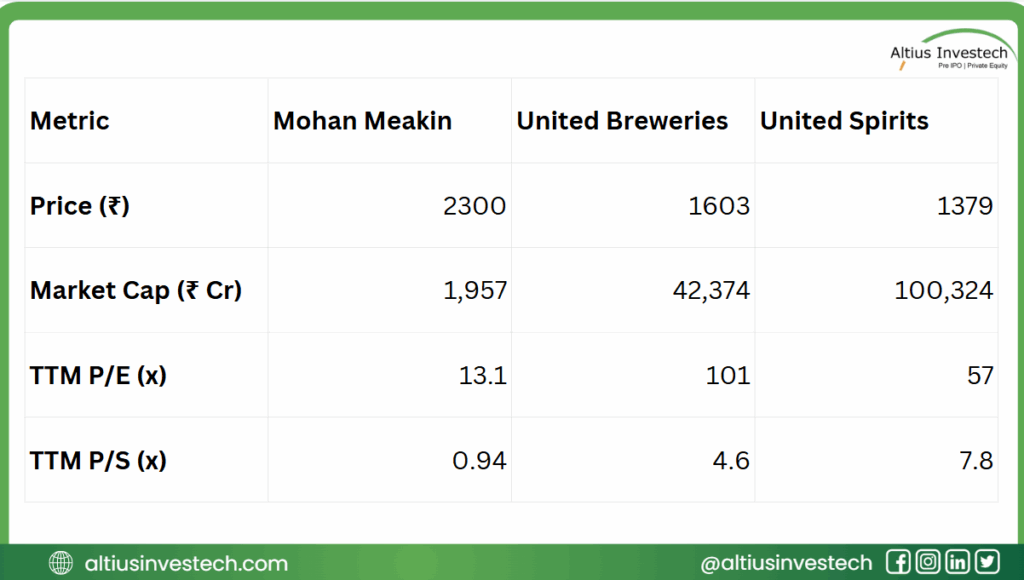

Peer Comparison

Conclusion

Overall, Mohan Meakin Limited is showing a clear improvement in earnings quality and profitability momentum, with valuation metrics compressing meaningfully as profits scale up. When viewed alongside listed peers, the company stands out for its materially lower earnings and sales multiples, suggesting that current pricing reflects a more conservative valuation despite improving fundamentals. This positions Mohan Meakin as a comparatively undemanding valuation play within the Indian alcoholic beverages space, contingent on the sustainability of recent operating performance.

Looking to invest in more high-potential companies like Mohan Meakin?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of February 20th, 2026, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)