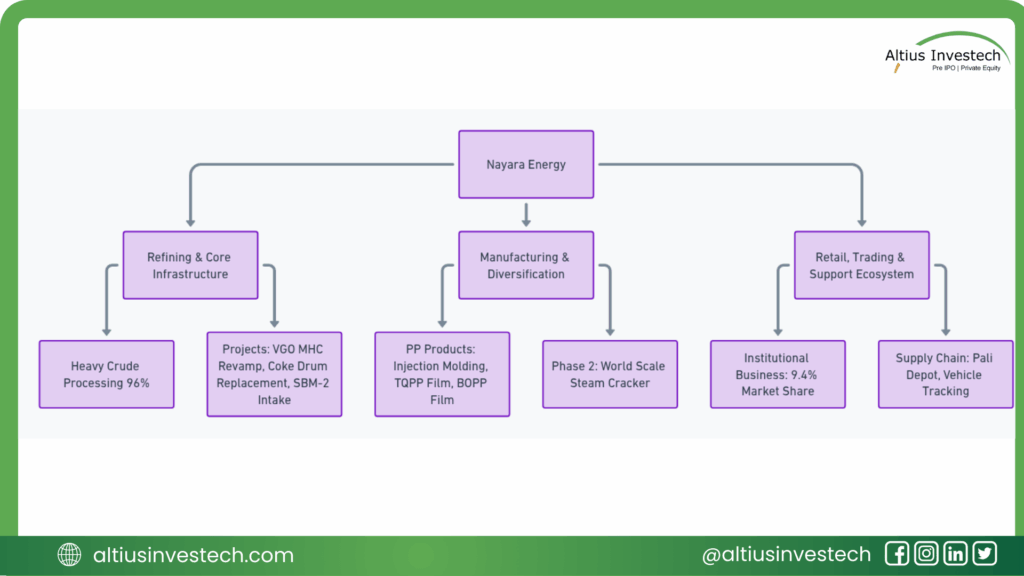

Nayara Energy: Core Assets & Strategic evolution

Nayara Energy Limited is a leading private-sector company in India’s downstream energy sector.

It is primarily involved in refining crude oil and marketing petroleum products in both domestic and international markets.

The company contributes approximately 8% of India’s total refining capacity, playing a key role in the nation’s energy security.

It operates India’s second-largest single-site refinery in Vadinar, Gujarat, with an annual capacity of 20 million metric tonnes (MMTPA).

Nayara Energy works with the guiding principle “In India, For India,” reflecting its strong commitment to the country.

Ownership Structure:

- Rosneft Singapore Pte Limited holds 49.13%.

- Kesani Enterprises Company Limited holds 49.13%.

Nayara’s Business Dynamics

Operational Foundation: The Engine of Efficiency ⚙️

A. The Vadinar Refinery Advantage

The Vadinar refinery’s high Nelson Complexity Index (NCI) is a cornerstone of Nayara’s competitive advantage, enabling it to process a wider range of discounted heavy and sour crude oils into higher-value products. In FY25, the refinery showcased its prowess by processing 96.1% ultra-heavy and heavy crude grades. This flexibility is crucial for maximizing Gross Refining Margins (GRM) across various market conditions and is a key differentiator in a competitive landscape.

B. Strategic Logistics & Integration

Nayara’s fully integrated logistics, including its captive deepwater port and extensive storage, provide unparalleled operational agility. This infrastructure facilitates efficient crude sourcing and optimized product distribution, both domestically and for exports, reducing reliance on third-party services and enhancing cost efficiencies. The ability to manage its own supply chain from port to pump is a significant structural advantage.

C. Capacity Utilization Trend

Consistently high capacity utilization rates at Vadinar underscore the refinery’s operational reliability and management’s expertise in optimizing throughput. In FY25, the refinery achieved a record crude throughput of 20.49 MMT, operating at an exceptional 102.3% capacity utilization. This is a critical factor for sustained profitability, proving the asset’s capability to run at peak performance.

The Strategic Value Proposition: Global Backing, Local Reach 🌐

A. The Ownership Structure as a Moat

The strategic partnership underpinning Nayara Energy—led by Rosneft, Trafigura, and UCP—forms a formidable competitive moat. This ownership structure provides assured access to diversified crude supplies, leveraging Rosneft’s global portfolio, while Trafigura’s expertise facilitates robust product offtake and integration into global commodity trading networks. UCP contributes financial and strategic oversight, solidifying Nayara’s position on the global energy stage.

B. The Retail Network Growth Thesis

Nayara’s aggressive expansion of its retail fuel station network is a strategic play to capture India’s rapidly growing domestic consumption. This provides a crucial hedge against volatile refining margins by securing captive demand. In FY25, the network expanded by 338 outlets to a total of 6,683, achieving a record sales volume of 8.3 million kilolitres (a 10% YoY increase). The focus on Tier 2/3 cities allows for a ‘first-mover’ advantage, complemented by initiatives to boost non-fuel revenues, enhancing overall network profitability and resilience.

Navigating Commodity Cycles and Financial Performance 📈

A. Refining Margin Volatility and Hedging

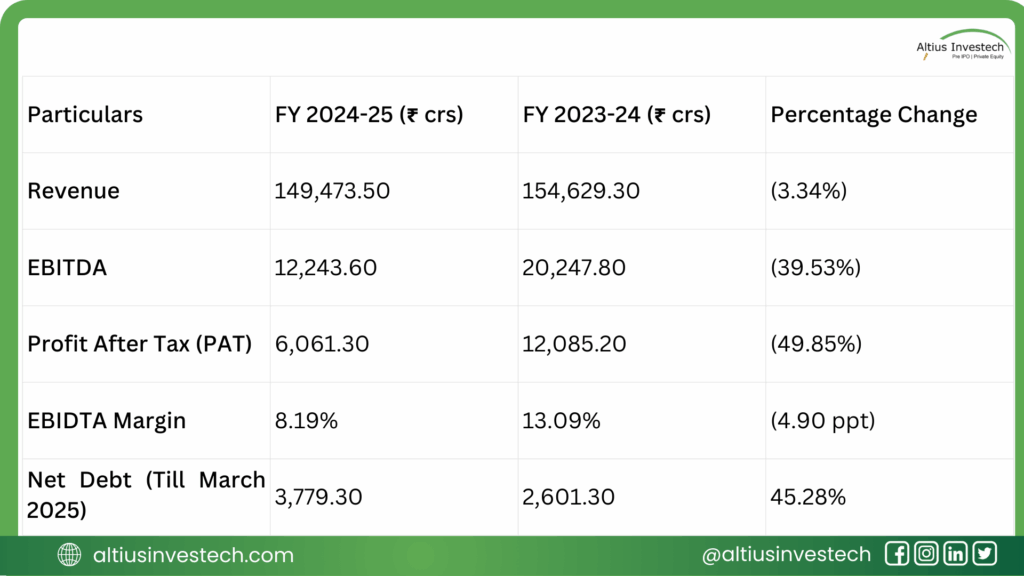

The refining sector is inherently cyclical, with profitability heavily influenced by global crude prices and product crack spreads. FY25 was a testament to this volatility, as Nayara’s EBITDA plummeted by ~41% to ₹122,946 million and PAT fell over 50% to ₹60,795 million. The operating margin compressed from 13.33% to 8.24%. While the company’s ability to optimize its crude basket provides some defense, these results highlight its exposure to adverse market swings and inventory losses.

B. Capital Allocation and Deleveraging

Nayara’s capital allocation strategy appears balanced. CapEx in FY25 was directed toward strategic growth, including the new petrochemicals unit. Despite the profit decline, the balance sheet remains robust with a low gearing ratio of 5.90% and growing total equity. A notable move was the approval of an ₹18,939 million share buyback, signaling management’s confidence and commitment to shareholder returns.

C. Future Growth Vectors

Looking ahead, Nayara’s planned foray into petrochemical integration represents a significant growth vector. The commissioning of its 450 KTPA Polypropylene (PP) plant in July 2024 is a pivotal first step. This downstream diversification aims to elevate its product value chain, unlock higher-margin revenue streams, and reduce the cyclicality associated with solely fuel-based refining. This move is a “natural hedge” against the volatility of its core business.

Financial Analysis

The ESG & Energy Transition Overhang: Risk Assessment ⚠️

A. Decarbonization Pressures

While Nayara benefits from robust immediate demand, the long-term imperative of India’s energy transition and commitment to Net Zero by 2070 poses a strategic challenge. Investors will keenly watch Nayara’s decarbonization roadmap, which includes refinery upgrades for higher energy efficiency, biofuel integration, and exploring hydrogen and carbon capture initiatives to future-proof its assets.

B. Regulatory Environment

Nayara operates within a dynamic regulatory landscape. The designation under the EU’s amended Regulation (EU) No. 833/2014 in July 2025 introduces significant geopolitical risk, potentially impacting trade flows and financing. Furthermore, a substantial year-on-year increase in contingent liabilities to ₹90,478 million, particularly from tax disputes, represents a major financial risk that cannot be ignored.

C. Sustainability Initiatives

Institutional investors are increasingly scrutinizing ESG performance. Nayara’s demonstrable efforts, such as introducing E15 and E20 blended fuels and achieving a 12.7% ethanol blend in its motor spirit, are positive steps. However, this is contrasted by a significant unspent CSR obligation of ₹1,457.34 million in FY25, which could attract reputational and regulatory scrutiny.

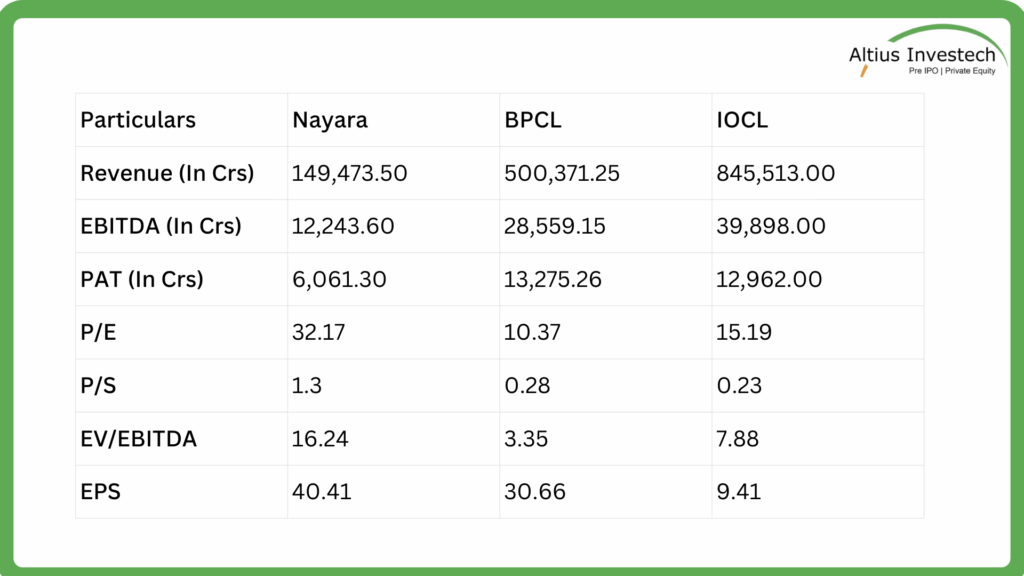

Peer Analysis (FY 2024-25)

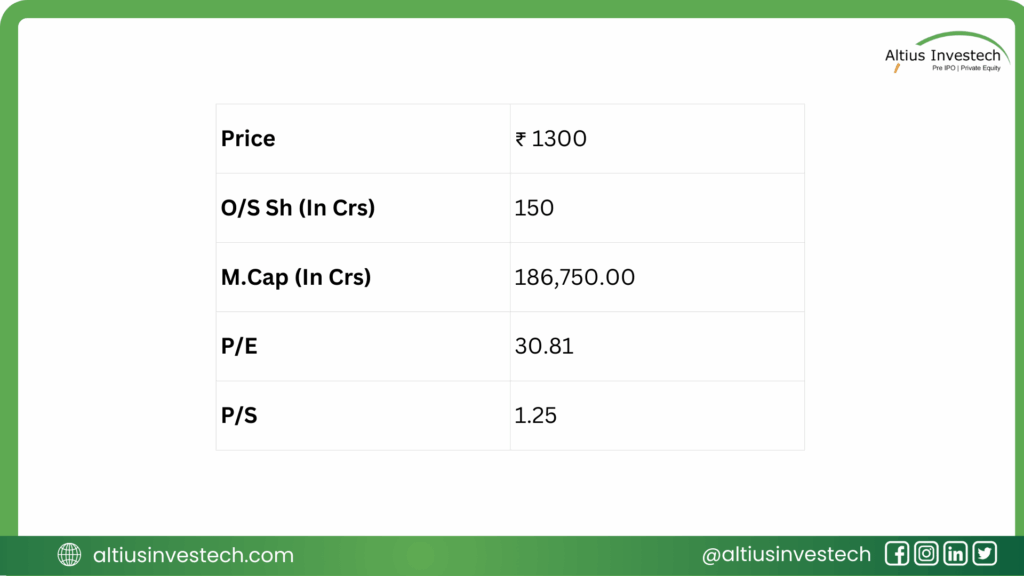

Price Analysis (FY 2025):

Conclusion: Refining the Investment View

- Synthesis: Nayara Energy’s core strengths are clear: a best-in-class, high-complexity refinery, strategic global backing, and a rapidly growing domestic retail footprint. These factors position it perfectly to capture India’s immediate energy demand growth. However, the severe profitability decline in FY25 demonstrates its vulnerability to global commodity cycles.

- Investment Caveat: The long-term risk posed by the energy transition, coupled with immediate geopolitical and regulatory risks like EU sanctions and massive contingent liabilities, must be carefully weighed. These headwinds must be offset by disciplined capital allocation towards diversification.

- Closing Statement: Nayara Energy remains a high-quality cyclical play, but its long-term equity story hinges critically on successfully executing its petrochemical and low-carbon transition strategies to build resilience against market volatility.

Looking to invest in more high-potential companies like Nayara Energy Limited ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius