With OYO news buzzing about a potential IPO in the next 12-18 months, investors are poring over its financials to answer one question: Is this a revolutionary tech disruptor poised for glory, or a debt-laden giant flying too close to the sun? A deep dive into OYO’s latest annual report for FY2025 reveals a company firing on all cylinders for growth, but with some serious red flags under the hood.

Explosive Growth: OYO’s story is one of scale. Revenue surged 16% and operating profit (EBITDA) jumped 22% in FY25. Its Gross Booking Value soared by an incredible 126%.

The Debt Dilemma: This growth has been fueled by borrowing. The company’s Net Debt skyrocketed by over 158% in a single year, raising critical questions about financial sustainability.

Profitability Paradox: While OYO reported a Profit After Tax (PAT), its core operations remain loss-making. The profit was driven by one-off “exceptional items,” not sustainable business activity.

Auditor Warnings: The company’s financial reports include a “material uncertainty” from auditors regarding the financial health of some subsidiaries, a significant concern for any potential investor.

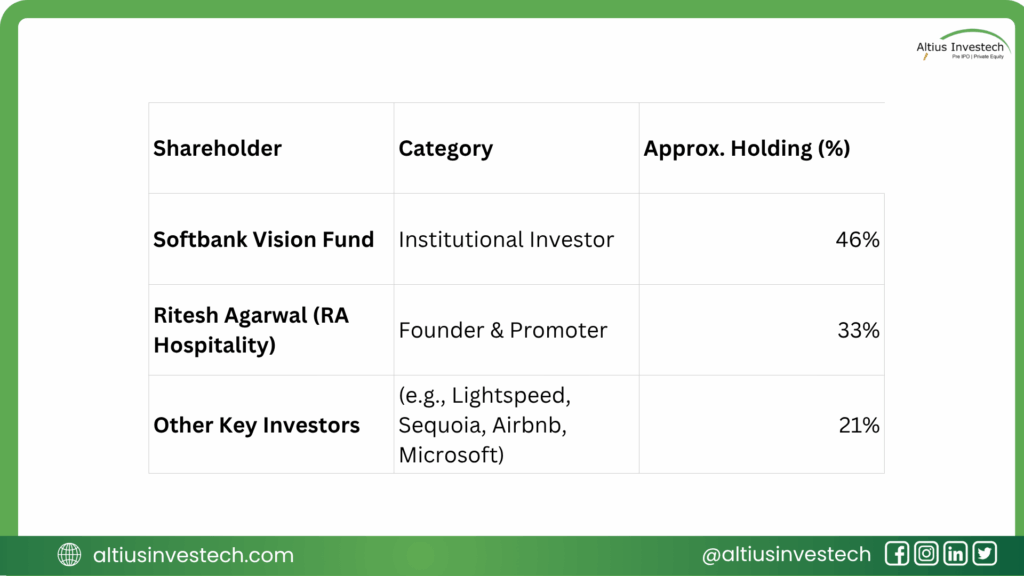

Ownership Structure:

OYO’s ownership is concentrated among its founder, key early-stage backers, and strategic investors. While the exact percentages shift with funding rounds, the major stakeholders based on recent filings are:

As an unlisted company, OYO’s valuation is based on private funding rounds. The January 2025 Series G funding valued the company at ₹36,015 Crores. Here is how its valuation metrics compare to other listed hospitality players:

🚀 What’s Driving the OYO Engine?

At its core, OYO is a two-sided technology platform. It takes fragmented, unbranded hotels and homes, standardizes them with the OYO brand, and plugs them into a massive digital ecosystem. This gives property owners higher revenue potential and offers travelers a wide range of reliable, budget-to-premium accommodations across 80+ countries.

The company is now expanding beyond its budget roots with a premium strategy under the “PRISM LIFE” umbrella, including brands like Sunday, Townhouse, and Palette. This entire operation is powered by a sophisticated tech stack using AI and data science to optimize pricing and enhance customer experience.

🛡️ What is OYO’s Competitive Moat?

OYO defends its market position through a combination of scale, technology, and strategic acquisitions.

Strategic Acquisitions: The bold $525 million acquisition of Motel 6 in the U.S. demonstrates OYO’s ambition to dominate the stable, value-conscious economy lodging segment in North America, adding hundreds of hotels to its portfolio.

Unmatched Global Scale: With a footprint that grew from 12,938 hotels to 18,103 in the last year, OYO’s sheer size creates a powerful network effect that is difficult for competitors to replicate.

Technology-Led Operations: OYO’s platform leverages hyper-personalization to drive high-margin direct bookings, giving it an edge over traditional hotels that rely on third-party aggregators.

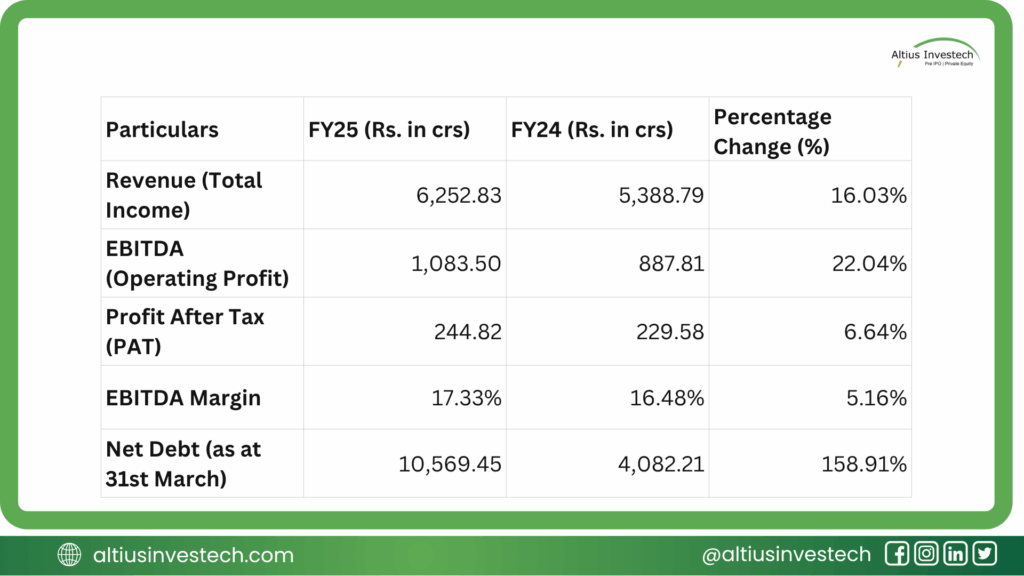

Financial Analysis

A look at OYO’s consolidated financial reports for FY2025 reveals a story of aggressive, debt-fueled expansion. While the top-line numbers are impressive, the balance sheet shows signs of increasing stress.

Financial Insights:

The headline numbers show a company that is growing and improving its operating efficiency. However, the core issue lies in profitability and leverage. The positive PAT of ₹245 Crores masks an underlying loss of ₹322 Crores before exceptional items and tax. This means the company is not yet profitable from its main business operations.

Furthermore, the 159% explosion in Net Debt to over ₹10,500 Crores is a major concern, indicating that recent acquisitions and operations are being heavily financed by borrowings.

⚠️ The Red Flags: What Could Go Wrong?

Beyond the debt, the annual report highlights several critical risks that investors must consider:

- Lack of Core Profitability: The reliance on one-off gains to show a net profit is unsustainable. The company must prove it can make money from its core hotel and home aggregation business.

- Weakening Liquidity: The company’s current ratio was halved in FY25. While still at a healthy level, such a sharp drop in a single year signals potential pressure on its ability to meet short-term obligations.

- Auditor’s “Material Uncertainty”: This is a serious warning. Auditors have cast “significant doubt” on the ability of some of OYO’s subsidiaries and joint ventures to continue operating, pointing to financial fragility within the group.

- Internal Control Gaps: The report noted weaknesses in the company’s financial software audit trails, a governance gap that could impact data integrity.

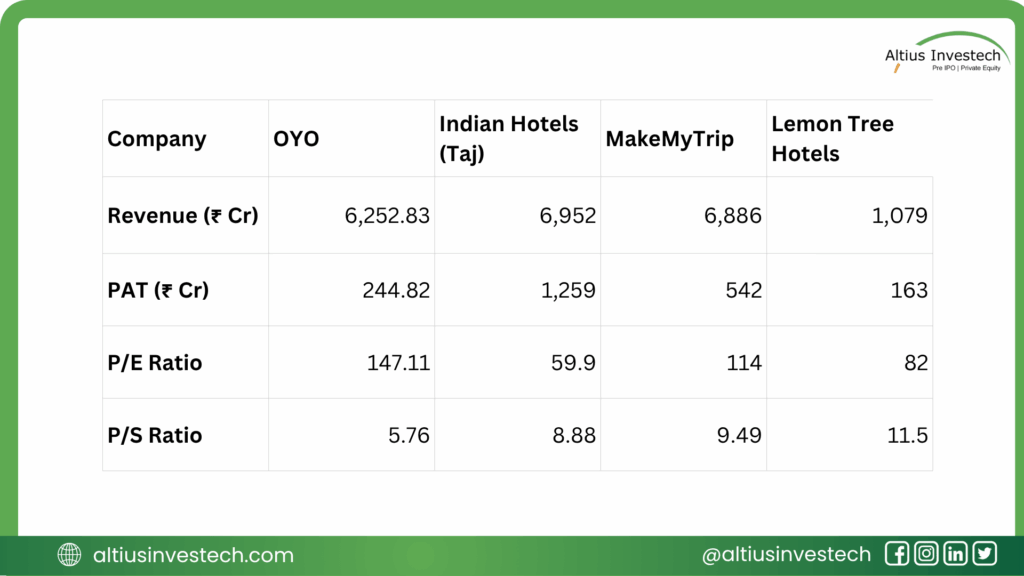

Peer Analysis (FY 2024-25)

When comparing OYO’s private valuation to publicly listed competitors like Indian Hotels (Taj), MakeMyTrip, and Lemon Tree, a clear picture emerges.

Based on its last funding round valuation of ₹36,015 Crores and its FY25 earnings, OYO has an extremely high Price-to-Earnings (P/E) ratio of approximately 147. This is significantly higher than established hotel chains like Indian Hotels (P/E ~60), indicating that investors are pricing in massive future profit growth.

However, its Price-to-Sales (P/S) ratio of around 5.8 is more conservative and comparable to its peers. This suggests OYO is being valued more like a high-growth tech platform for its revenue scale and market share, rather than its current, modest profitability. In essence, the investment thesis hinges on OYO dramatically improving its earnings to justify its premium valuation.

⚖️ A High-Risk, High-Reward Bet

Investing in the OYO IPO will be a decision based on your appetite for risk and belief in its long-term vision.

| Bull Case (Why to be Optimistic) 👍 | Bear Case (Reasons for Caution) 👎 |

| Unprecedented Scale and strong brand recall in a growing global travel market. | Massive Debt Load creates significant financial risk and high interest costs. |

| Powerful Tech Platform drives efficiency and high-margin direct bookings. | Lack of Core Profitability means reliance on non-recurring gains to stay in the black. |

| Strategic shift to premium and aggressive expansion into stable markets like the U.S. | Serious Auditor Red Flags regarding the financial health of subsidiaries. |

| Favorable industry tailwinds with rising global demand for travel. | Weakening Liquidity and internal control gaps point to potential operational stress. |

Conclusion: Refining the Investment View

OYO is a high-octane growth machine making a bold, debt-fueled push for global market dominance. For investors, it’s a bet that the company can outgrow its debt, fix its underlying profitability issues, and successfully integrate its acquisitions before the financial risks catch up. The path ahead is risky, but if management executes flawlessly, the reward could be substantial.

Looking to invest in more high-potential companies like OYO ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)