In the crowded world of housing finance, finding a company that balances aggressive growth with conservative safety is rare. But the FY25 annual report for Shubham Housing Development Finance reveals exactly that. This affordable housing lender is growing its revenue at 33% and its profits at nearly 29%.

What makes this story unique isn’t just the growth; it’s the “fortress balance sheet” behind it. Thanks to a massive Series F funding round, the company is sitting on a Capital Adequacy Ratio (CRAR) of 46% more than double the regulatory requirement. This is a lender with a war chest, ready to capture India’s booming affordable housing market.

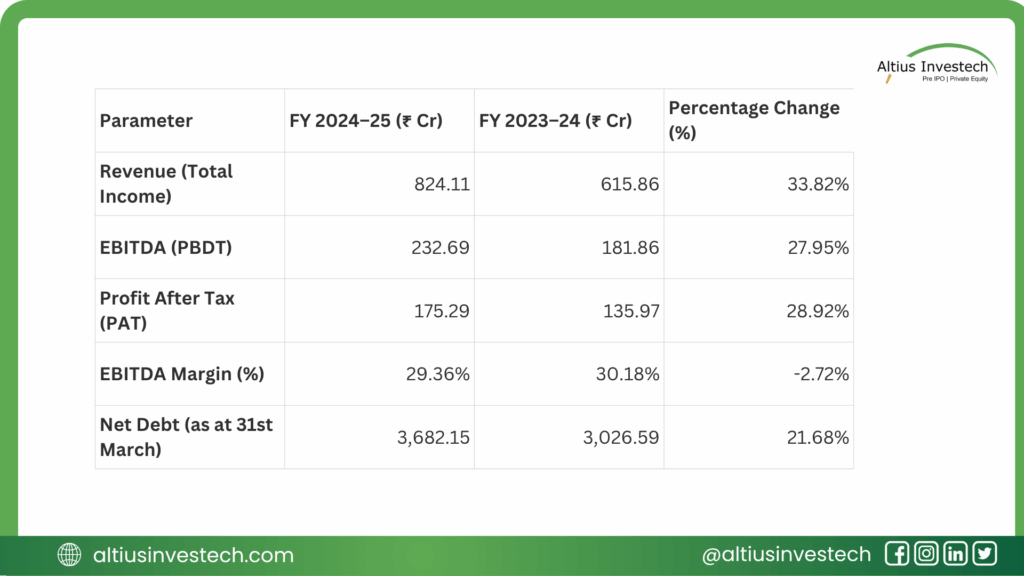

Let’s break down the numbers.

Strong Growth: Total Income surged 33.8% to ₹824 Cr, driven by robust demand for affordable housing loans.

Profit Power: Net Profit (PAT) grew 29% to ₹175 Cr, showing the company can translate lending into earnings.

The “Fortress”: A CRAR of 46.24% makes this one of the best-capitalized lenders in its class, providing a huge buffer for future growth.

Margin Pressure: The cost of growth is rising. EBITDA margins dipped slightly (-2.7%) as borrowing costs and expansion expenses increased.

The Tech Edge: By using a “cash-flow based” underwriting model powered by apps and analytics, Shubham serves the informal income segment that big banks ignore.

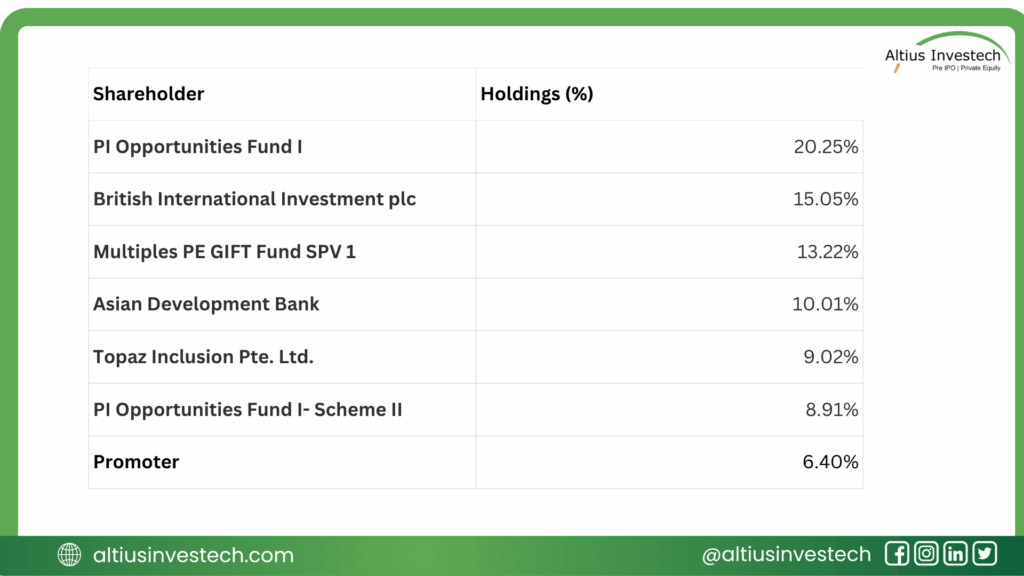

👑 Who Owns Shubham? A PE-Backed Powerhouse

Shubham is not a typical promoter-led firm. It is backed by a consortium of top-tier global investors, including private equity giants and development banks. This institutional backing brings rigorous governance and deep pockets for growth.

Financial Analysis

📈 The Financials: Growth with Discipline

The FY25 numbers tell a story of scaling up. The company has successfully expanded its loan book while maintaining profitability.

Financial Insights:

The slight dip in EBITDA margin is the only blemish, but it’s understandable. Finance costs (interest expenses) rose as the company borrowed more to lend more. Additionally, the company aggressively expanded its branch network (adding 33 new branches), which increased operational costs. However, the 29% PAT growth confirms that the core lending engine is highly profitable.

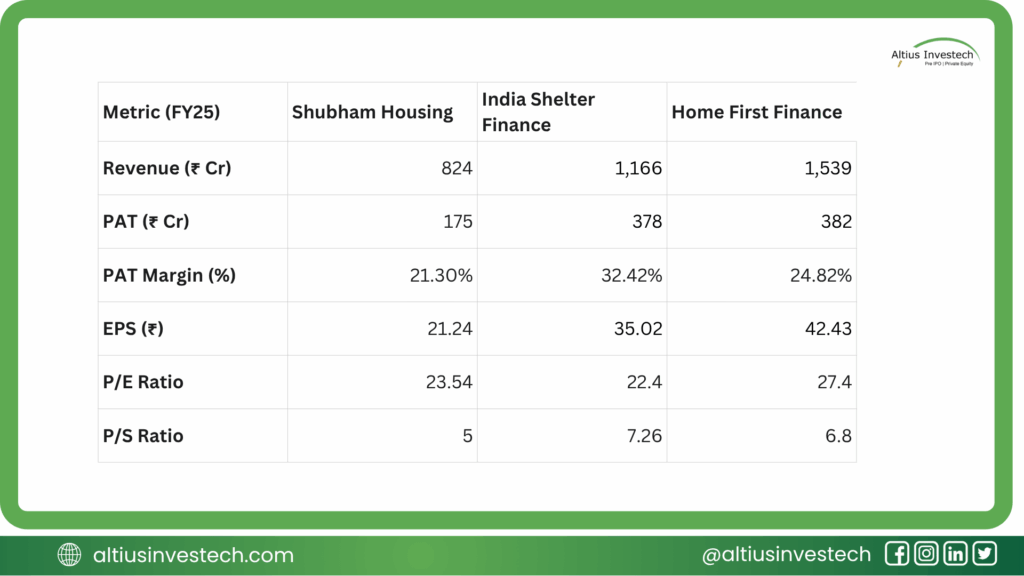

📊 Peer Analysis: Is Shubham Undervalued?

To understand Shubham’s value, we compare it to listed peers in the affordable housing space with similar revenue scale, such as India Shelter Finance and Home First Finance.

(Valuation Note: We have assumed a share price of ₹500 for this analysis to derive P/E and P/S ratios.)

This table shows a clear disconnect between profitability and valuation, which is key to understanding the investment thesis.

Its P/S ratio of 6.17x is double that of MAS and four times that of Repco.

Repco Home Finance (The “Value” Play): Repco is the most profitable and efficient company in the group by a huge margin. It boasts a 28.20% PAT margin and generates the highest absolute profit (₹461 Cr). However, the market assigns it a rock-bottom P/E ratio of 5.72x and a P/S of 1.54x. This signals that investors see Repco as a mature, slow-growth “value” stock, likely a secure cash cow with limited upside.

MAS Financial (The “Growth at a Reasonable Price” Play): MAS Financial is the “middle-of-the-road” stock. Its profitability is solid (17.7% margin), and its valuation is reasonable (16.5x P/E). The market views it as a stable, reliable grower, balancing growth and value.

Veritas Finance (The “Hyper-Growth” Play): This is the most critical insight. Veritas has a PAT margin (18.95%) similar to MAS Financial but is far less profitable than Repco. Despite this, it commands the highest valuation of the entire group.

Its P/E ratio of 27.0x is significantly higher than its peers.

Conclusion: Refining the Investment View

The market is pricing Veritas as a premium, high-growth company. It is not valuing the company based on its current profits, which are lower than Repco’s. It is paying a premium based on its 39% revenue growth story.

Investors are betting that Veritas’s rapid expansion will allow its earnings to grow much faster than its peers, justifying the high price. An investment in Veritas is a clear bet on future growth, whereas an investment in Repco is a bet on current value. The upcoming IPO will be a test of whether public market investors agree with this premium “hyper-growth” valuation, especially given the rising credit costs.

Looking to invest in more high-potential companies like Shubham Housing Development Finance?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)