Vivriti Capital, a major player in India’s mid-market lending space, just dropped its annual report, and it’s one of the most complex and fascinating stories of the year. On one hand, the company is a growth machine, posting a 36% jump in revenue and a mind-boggling 11,112% surge in net profit.

On the other, it’s a business facing very real headwinds: rising NPAs in key segments, a constant need for cash to fund growth, and a massive, complex corporate restructuring on the horizon. As an analyst, this is a puzzle. Is this a high-growth rocket ship or a house of cards? Let’s dive in.

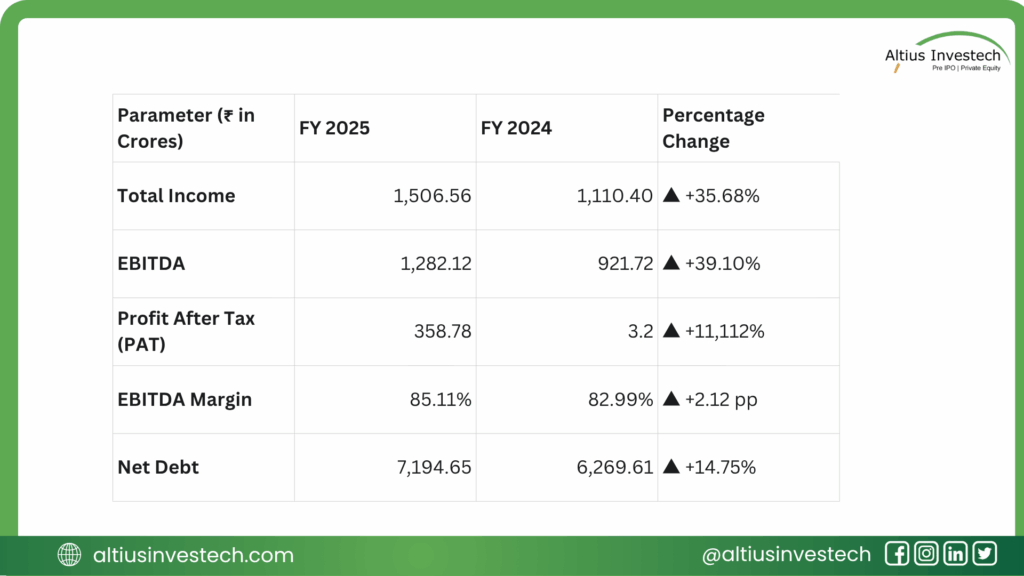

Spectacular Profit Growth: Consolidated Net Profit (PAT) skyrocketed from ₹3.2 Cr to ₹359 Cr, an 11,112% increase.

Strong Core Engine: The growth is real. Total Income grew 36% to ₹1,507 Cr, and operating profit (EBITDA) grew even faster at 39%, showing improving margins.

The Big Restructuring: The company is undergoing a massive corporate split to separate its Lending (NBFC), Asset Management (AIF), and Marketplace (Tech Platform) businesses. This is the single biggest event for investors.

Real-World Risks: Asset quality is slipping. The unsecured personal loan book has an alarming 7.45% NPA (Non-Performing Asset) rate.

The Cash-Hungry Model: Like all fast-growing lenders, Vivriti is burning cash to grow. It consumed over ₹1,125 Cr in Free Cash Flow last year, making it heavily reliant on raising new debt.

What Does Vivriti Actually Do?

Think of Vivriti as a specialized bank for India’s “missing middle” mid-sized companies that are too large for small finance and too small for giant corporate banks. It provides them with customized debt, helping them fund everything from new factories to managing their day-to-day cash flow. It operates two main segments: the NBFC (lending) and Fund Management.

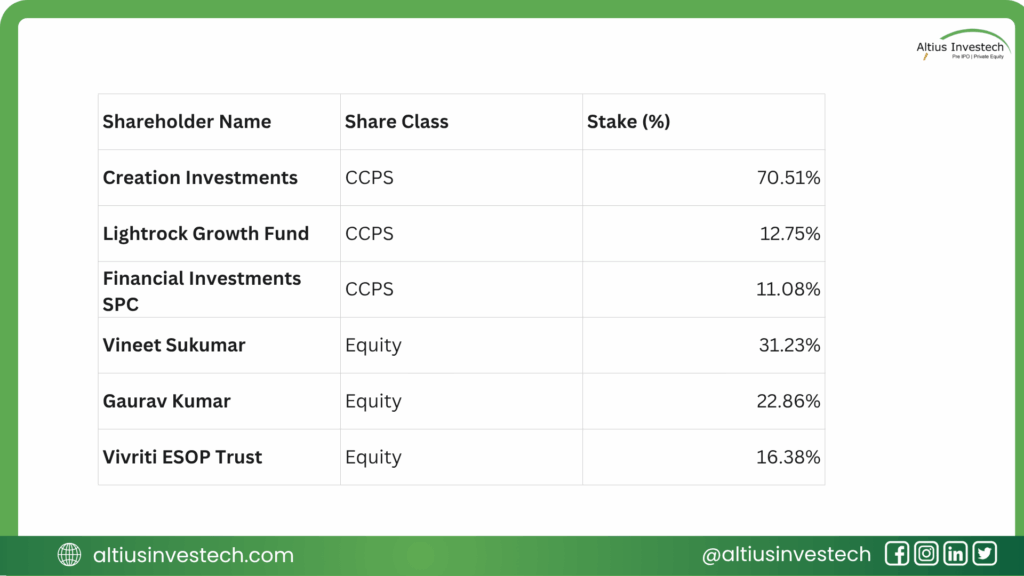

Who Owns Vivriti?

This is not a traditional “promoter-run” company. While the founders hold significant equity, the real power lies with the institutional investors holding preference shares.

This is a private equity-backed company. The institutional CCPS holders (Creation & Lightrock) are the dominant capital providers, and they will be looking for a successful exit, which is a key driver for the restructuring and eventual IPO.

The Big Story: Why Vivriti is Tearing Itself Apart (To Create Value)

The most important news is the complex Composite Scheme of Arrangement. Management is splitting the company into three distinct entities. This isn’t a sign of distress; it’s a strategic move to unlock value.

Why do this?

- Ring-fence Risk: It separates the high-risk, capital-heavy Lending business from the fee-based, high-growth Asset Management and Marketplace (tech) businesses.

- Independent Growth: Each new entity can raise its own capital based on its own business model (e.g., a tech platform gets a tech valuation, a lender gets an NBFC valuation).

- Clear Focus: It creates pure-play companies, making them easier for investors to understand and value.

How the Restructuring Will Work (Simplified)

This is a 3-step process involving two demergers and one amalgamation.

- Step 1: NBFC Demerger: The core Lending Business is moved out of Vivriti Capital (VCL) and into a new company (HCIMPL).

- Step 2: AMC Amalgamation: The Asset Management company (VAM) is first merged into VCL (this is just a temporary housekeeping step).

- Step 3: AMC Demerger: The Asset Management business is then immediately demerged out of VCL and into another new company (VFPL).

The original VCL will be left as a pure-play Marketplace / Credit Tech Platform. A new holding company, Vivriti Next Limited (VNL), will be created to hold the new NBFC and AMC businesses.

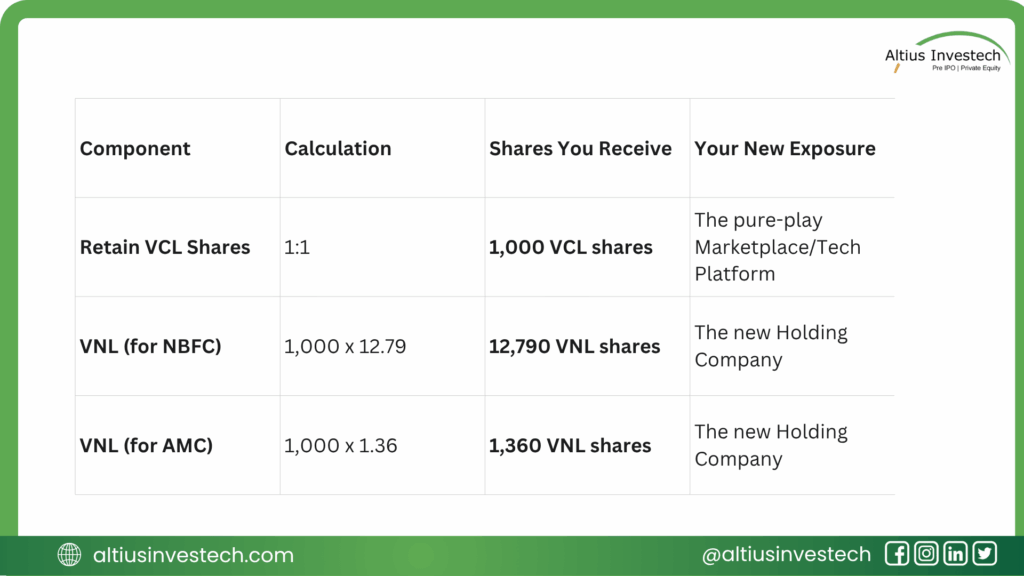

What Will You Get? (Example for 1,000 VCL Shares)

If you hold 1,000 shares of Vivriti Capital (VCL) today, here is what your portfolio will look like after the split:

Your Final Holding:

- 1,000 shares of VCL (the Marketplace)

- 14,150 shares of VNL (the Holding Company for the NBFC and AMC)

This split is complex, but it’s designed to give shareholders direct exposure to the high-growth tech platform while holding the more traditional (but larger) lending and asset management businesses under a separate, clean structure.

Financial Analysis

The headline numbers are staggering, but the story is more nuanced.

Financial Insights:

The business is growing fast. A 36% revenue growth for an NBFC of this size is very strong.

More importantly, EBITDA grew faster than revenue. This means the company’s core profitability and operational efficiency are improving. The EBITDA margin expanded to a very healthy 85.1%.

The 11,112% PAT jump is real but comes from a tiny base of just ₹3.2 Cr in FY24.

The Big Caveat: The consolidated profit of ₹359 Cr includes a massive ₹200 Crore loss from its associate company, CredAvenue. This means Vivriti’s core business is actually even more profitable than the headline number suggests. The associate loss is a huge drag on the final PAT.

⚠️ Red Flags: The Risks Under the Hood

- The Associate Drag: That ₹200 Crore loss from its associate (CredAvenue) is a recurring problem that is wiping out a huge chunk of the core business’s profits at the consolidated level.

- Asset Quality Cracks: This is the main operational risk. While the overall Gross NPA of 1.89% seems low, the devil is in the details. The unsecured personal loans segment has a 7.45% NPA rate. This is a flashing red light, showing significant stress in a high-risk part of their book, driven by recent RBI rule changes.

- The Cash Burn: The company is Free Cash Flow negative (to the tune of -₹1,125 Cr). This isn’t a sign of failure; it’s the nature of a fast-growing lender. But it means Vivriti is perpetually reliant on capital markets (raising new debt) to fund its growth. If liquidity tightens, its growth engine stalls.

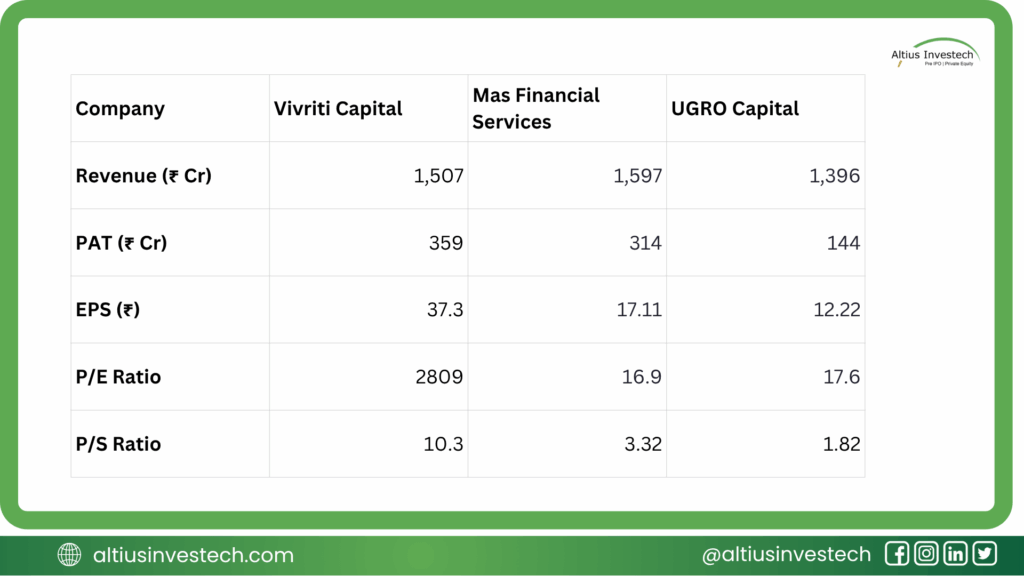

Peers Analysis

Vivriti’s revenue and profitability (PAT) are significantly stronger than its closest listed peers. Its PAT of ₹359 Cr (even with the associate loss) is well ahead of Mas Financial (₹314 Cr) and UGRO (₹144 Cr). This suggests that if and when Vivriti lists, it could command a premium valuation over its peers, if investors are convinced by the restructuring story and can look past the asset quality risks.

Conclusion: Refining the Investment View

Financially Robust Core: Vivriti’s core business is a high-growth, high-efficiency engine. Its profitability is even stronger than the 11,000% PAT jump suggests, as it’s currently absorbing a massive ₹200 Cr loss from an associate.

A “Complexity & Risk Discount” is Warranted: The company is not a simple buy. Investors must discount the valuation for two key factors: 1) The real, measurable asset quality risk in its unsecured book (7.45% NPA), and 2) The significant execution risk and complexity of its 3-way corporate split.

Valuation Hinges on the Restructuring Narrative: The entire investment thesis rests on the success of this split. The goal is to convince investors that they are getting three distinct, high-potential businesses (Lending, AMC, Tech) and that the whole will be worth more than the sum of its parts.

Concluding Perspective: This is a complex but compelling opportunity for sophisticated investors. The company is demonstrably strong on growth and core profitability. The investment is a bet that the complex restructuring will successfully unlock value, clean up the balance sheet, and separate the high-growth tech platform from the high-risk lending arm.

Looking to invest in more high-potential companies like Vivriti Capital ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)