When a small-cap stock posts a 57.6% surge in revenue and a 59.3% jump in net profit, investors take notice. On the surface, the latest annual report from Urban Tots (Deepak Houseware & Toys Limited) looks like a breakout success story.

But as an analyst, my job is to look past the shiny P&L, and what’s underneath is deeply concerning. The company is funding this growth with debt, its cash reserves have been depleted, and it’s riddled with some of the most significant governance and related-party red flags I’ve seen this year.

This is a classic tale of two companies: a high-growth P&L and a high-risk balance sheet.

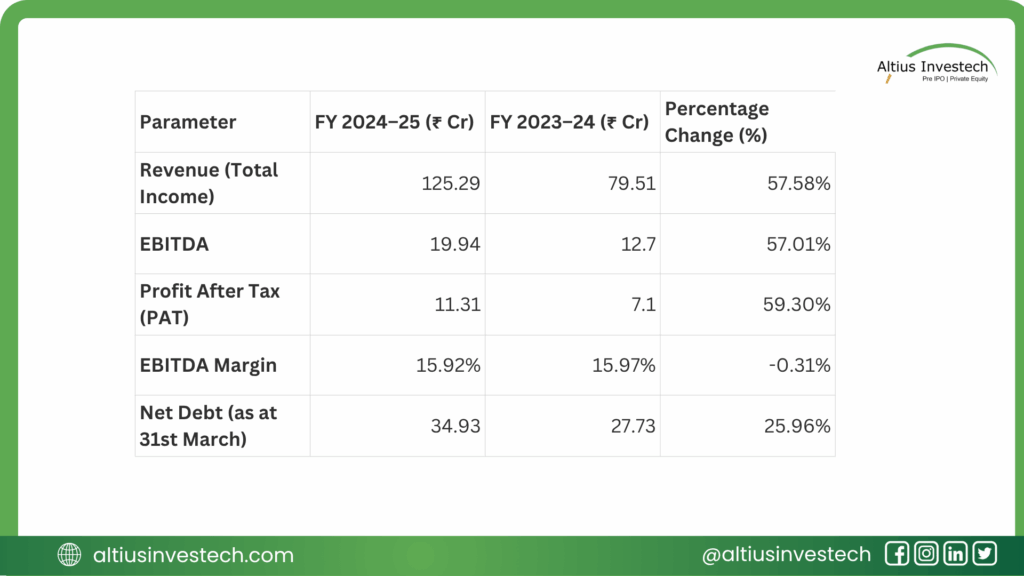

The Good: A spectacular growth story. Revenue surged to ₹125 Cr (from ₹79 Cr), and Net Profit hit ₹11.3 Cr (from ₹7.1 Cr).

The Bad: This growth is cash-hungry. Free Cash Flow is negative (-₹4.5 Cr), cash on hand has “dropped precipitously,” and the company is taking longer to get paid by its customers.

The Ugly (Governance): Auditors flagged a massive internal control failure—the company’s accounting software lacked a mandatory “audit trail” for the entire year.

The Really Ugly (Related Parties): The Managing Director’s remuneration jumped 328% (from ₹42L to ₹180L), and rent paid to a relative more than doubled to ₹3.2 Cr. The auditor could not confirm if these deals were at fair market prices

👑 Who Owns Urban Tots? A Tightly Controlled Ship

This is a classic promoter-owned and operated company. The Chaudhary family controls over 94% of the shares.

With a tiny 5.58% public float, the promoters have absolute control. This can be good for decisive action, but it also means minority shareholders have virtually no say and are along for the ride for better or worse.

Financial Analysis

📈 The Financials: A Story of Growth

The P&L statement from the annual report is, without question, impressive. The company is successfully scaling its toy manufacturing business.

Financial Insights:

The story here is pure top-line growth. The company is selling more, and its profit is growing in lockstep.

But the first clue of a problem is the EBITDA Margin. It’s flat. This means the company’s costs (materials, employee benefits, rent) are rising just as fast as its sales. It’s not achieving any new efficiency or operating leverage as it gets bigger.

💸 Where’s the Cash? The “Bad” News

This is where the positive story starts to unravel. A profitable company should be generating cash. Urban Tots is not.

- Free Cash Flow is Negative: The company reported a negative Free Cash Flow of -₹4.5 Crores.

- Why? Because it spent ₹14 Crores on new CAPEX (factories, equipment). This aggressive expansion is being funded by debt (Net Debt is up 26%) and by draining its own cash reserves, which dropped from ₹1.24 Cr to just ₹0.25 Cr.

- Working Capital Stress: The company is also taking longer to get paid. Its Trade Receivables (money owed by customers) ballooned 78%, and the “turnover ratio” declined. This is a classic sign of liquidity strain—selling fast, but collecting slow.

🚩 The Red Flags: The “Ugly” Truth

This is the most critical part of the analysis. A seasoned investor looks for governance, and what we find here is alarming.

1. The “Missing Audit Trail”

The auditors issued a major warning: the company’s accounting software did not have a mandatory “audit trail (edit log)” feature for the entire year.

- Why this is a deal-breaker: An audit trail is a basic, legally-required control. It records every change and deletion, preventing data tampering. Without it, there is no way to ensure the financial numbers are 100% integral. This is a massive governance failure.

2. The Exploding Related-Party Deals

This is where the flat margins and high costs come into focus. While the company grew 57%, look at how fast payments to related parties grew:

- MD’s Remuneration (Mr. Deepak Chaudhary): Jumped +328% (from ₹42 Lakhs to ₹1.80 Crores).

- Rent Paid to Relative (Mr. Tarsem Lal): Jumped +110% (from ₹1.52 Crores to ₹3.20 Crores).

- Purchases from Related Firm (Deepak Polymers): Jumped +806% (from ₹50 Lakhs to ₹4.53 Crores).

The kicker? The auditor explicitly stated they could not confirm if these transactions were at a fair “Arm’s Length” price because the items were “of an exclusive nature.”

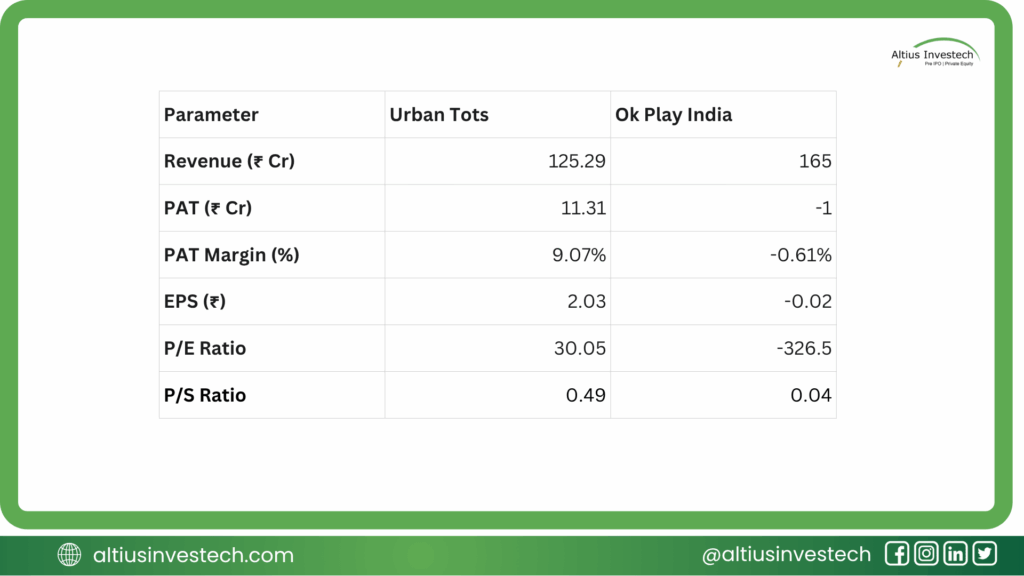

📊 Peer Analysis: Is Urban Tots Overvalued or a Growth Gem?

To understand the investment thesis for Urban Tots, we need to compare it to its peers. The “Made in India” toy industry is highly fragmented, with most major players like Funskool and Mattel being unlisted or foreign-owned.

This leaves us with one primary, direct competitor on the stock exchange: Ok Play India.

A side-by-side comparison of their financials from the most recent full year (FY25 for Urban Tots, TTM for Ok Play) reveals a stunning difference and is the key to the whole investment story.

This comparison tells a simple but powerful story.

- A Tale of Two Toy Companies: While both companies are in the “Made in India” toy space, their financial health is completely opposite. Urban Tots is a high-growth, solidly profitable company with a 9.07% net profit margin. Ok Play, despite having higher revenue, is loss-making.

- The Profitability King: Urban Tots is demonstrably the superior operator. It has proven it can translate its sales into actual profit, a test its main listed competitor is currently failing.

This “scarcity” is a critical part of its valuation. The market is assigning a ~30.05x P/E ratio to Urban Tots because it’s the only investable company to capture the booming domestic toy manufacturing theme. This high valuation is a clear bet on its 59% profit growth and its unique position as the “only game in town” for this story.

Conclusion: Refining the Investment View

Urban Tots (Deepak Houseware & Toys Limited) presents investors with a high-stakes “growth vs. governance” dilemma. The company’s 57% revenue and 59% profit growth are genuinely impressive, establishing it as the only profitable, high-growth “Made in India” toy manufacturer in its listed peer group. This strong narrative has earned it a premium P/E valuation of approximately 32x. However, this compelling growth story is critically undermined by severe governance red flags found in its annual report. The auditor’s discovery of a missing mandatory “audit trail” in the accounting software raises serious questions about data integrity. These concerns are amplified by a pattern of exploding related-party payments including a 328% hike in the MD’s salary and soaring rent to relatives that the auditor could not even verify as being at a fair market price.

Looking to invest in more high-potential companies like Urban Tots (Deepak Houseware & Toys Limited) ?

Explore exclusive opportunities by logging in to Altius Investech today!

GET IN TOUCH WITH US:

For any query/ personal assistance feel free to reach out at support@Altiusinvestech.com or call us at +91-8240614850.

Learn, more about Unlisted Company.

Join our Whatsapp Channel: The Market Buzz by Altius

📜 Disclaimer

(Data as of July 29th, 2025, from public sources & altiusinvestech.com. For educational purposes only; not investment advice. Altius Investech is not SEBI-registered; investors should do their own due diligence.)